Read the results of Solomon Exam Prep’s latest poll on the topic of cryptocurrency regulation – and learn which license you’d need for either outcome. Continue reading

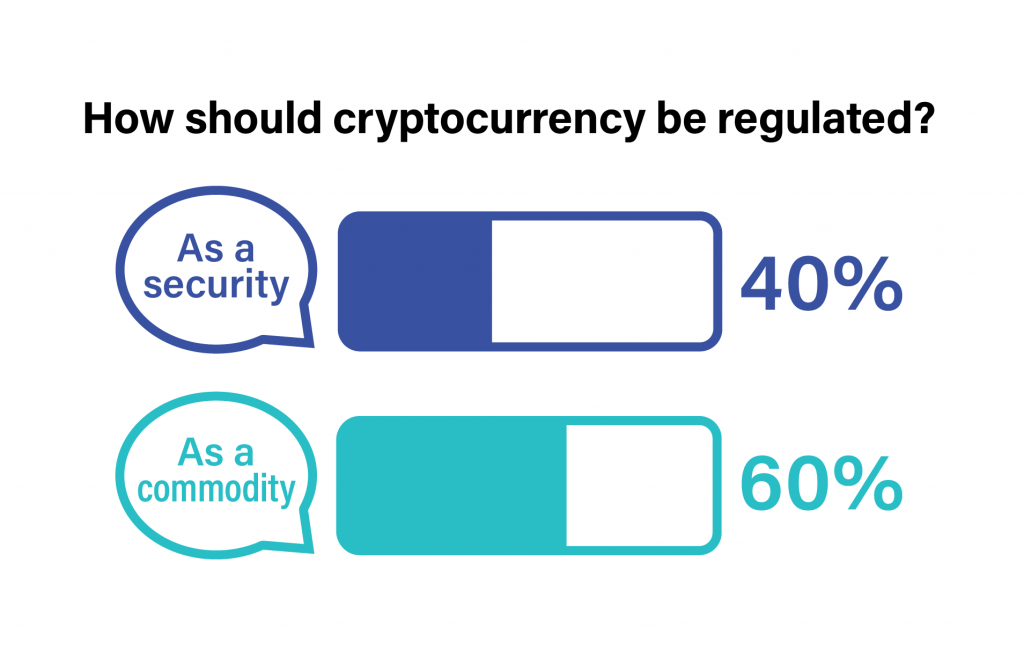

With the regulatory status of Bitcoin and other cryptocurrencies still up in the air, a recent Solomon LinkedIn poll found that 60% of Solomon customers think cryptocurrencies should be treated as commodities, while 40% said they thought cryptocurrencies should be regulated as securities.

Thus far the SEC has avoided clearly stating that cryptocurrencies are securities. To do so, the SEC would likely have to show that cryptocurrencies meet the “Howey Test,” which says that securities must have four characteristics. According to this test, a security involves (1) an investment of money that (2) involves a common enterprise (3) in which the investors expect to make a profit, and (4) the profits will be derived from the efforts of someone other than the investor.

If the SEC, Congress, or the courts declare that cryptocurrencies meet the Howey Test and are therefore securities, Solomon’s got you covered with the Series 7 General Securities Representative Exam Guide. This FINRA license allows you to engage in “the solicitation, purchase and/or sale of all securities products.”

If cryptocurrencies don’t meet the Howey Test, they could be regulated as commodities. These are goods such as wheat, gold, and pork bellies. Why might cryptocurrencies fit in with these others? Because commodities are all highly standardized so that they can be freely bought and sold on exchanges without worrying about differences in quality—every ounce of gold is pretty much like every other ounce of gold. Likewise, every Bitcoin is like every other Bitcoin.

If you’re considering taking the SIE, Series 6, Series 63, Series 7, or another securities licensing exam, read these valuable insights on how to study for and pass your exams. Continue reading

It’s not uncommon for those in the securities and investment industries to need more than one securities license. But the determination involved in passing multiple securities licensing exams (especially in a short time period) is substantial. Case in point: Alexandria Coyne, Financial Advisor at Northwestern Mutual, who passed her fourth exam with Solomon Exam Prep earlier this year. She now has the SIE, Series 6, Series 7, and Series 63 under her belt. Alex was kind enough to answer Solomon’s questions about her study approach and how she achieved success four times.

“I really wanted to learn the material through and through, so I was never preparing for an exam; I was preparing for a career.”

Alex Coyne

Solomon Exam Prep: Why did you take your exams in the order that you did? Was this order helpful, or would you change anything if you had to do it again?

Alex Coyne: I took the SIE, the 6, the 63 and then the 7. If I could do it all over, I’d do the same thing! The SIE was a great entry level exam for the 6. To me, there was only a little bit of differentiating content between the two exams. I will always recommend splitting up the 6 and the 7. I think the 6 was just high-level enough to get an understanding of the content. The 7, on the other hand, got extremely detailed. I truly believe that if I went straight into the 7 from the SIE, I wouldn’t have been successful on my first attempt.

Solomon Exam Prep: Out of the exams you passed, which one required the most study time and why?

Alex Coyne: Most definitely the Series 7. I just think that there were a lot of details to remember and a lot of information to digest.

Solomon Exam Prep: How did you approach studying for your exams?

Alex Coyne: I recommend everyone to Solomon. I think that Solomon did an amazing job with the study material. What I have found to be most successful for me:

The first thing I did was set an exam date. That was just knowing my ability to procrastinate, so I had to put a timeline on this thing before it even started!

Order the book. Read the entire book in full, highlighting important content and underlining even more important content. I found that 20 pages per day was my reading goal.

Once the book was read in full, I WROTE out all the highlighted and underlined information onto a notebook. Yes, I outlined the entire book. I found that approximately 10 pages of outlining per day was my capacity (approx. 1-2 hours). It took an entire 2-subject notebook for an entire outline. (Still no quizzes at this point.)

While I was reading and outlining, I played the online Video Lectures through my AUX cord in my car wherever I went. From start to finish.

After outlining the entire book, I went to my NOTEBOOK (outlined) and I went through the content in detail. After I studied Chapter 1, I took Ch. 1 practice quizzes until passing consistently. Then Chapter 2, 3, 4 and so on….

After all of the Chapter quizzes were complete, I did the practice tests. I probably did 15-20 total practice exams. Some timed, some with immediate feedback. I made sure to read the feedback and understand what questions I was getting wrong and use my book and notebook to go back to content and work through the wrong answers.

On the 7, the Options Video Lecture was a total game changer for me. I watched it twice and memorized every table on there. That single-handedly won me 15-20 questions on the Series 7 exam.

“…there are still things from the study material that I use in client meetings today, 8 months since the Series 7 exam.”

Solomon Exam Prep: How did you take the exams – at a testing center or remotely? How was your experience, and do you have any tips to share?

Alex Coyne: I took all of my tests in a testing center. My advice: Practice your “dump sheet.” AKA: Once you START the exam, dump out all you can remember on scratch paper. I actually practiced my dump sheet, especially for the Series 7. The week leading up the 7, randomly throughout the day, I would stop what I was doing, find paper, and practice my dump sheet. By the time I took my Series 7, I pretty well had my dump sheet memorized. That was very helpful for me.

Solomon Exam Prep: Any words of wisdom to help motivate others who are preparing for exams?

Alex Coyne: Passing on the first try is very possible, but you will only get out of the material the level of commitment you decide to put into it. I really wanted to learn the material through and through, so I was never preparing for an exam; I was preparing for a career. I saw this knowledge as transformational for my financial practice. I took it seriously and there are still things from the study material that I use in client meetings today, 8 months since the Series 7 exam. My advice is to have that mentality when it comes to learning; don’t just cram to pass an exam. Our clients deserve better.

Visit the Solomon Exam Prep website to explore study materials for 21 different securities licensing exams, including the SIE, Series 6, Series 7, and Series 63.

Learn what the FINRA Series 6 qualifies you to do, what the exam covers, and how you should prepare for it. Continue reading

What does the FINRA Series 6 exam allow me to do?

The Series 6, also known as the Investment Company Products/Variable Contracts Representative Exam, qualifies individuals to solicit, purchase, and/or sell certain investment products. These include mutual funds, initial offerings of closed-end funds, variable life insurance, variable annuities, municipal fund securities, and unit investment trusts (UITs).

The Series 6 does not entitle you to sell all securities products – for that, you’ll need the Series 7. But if you intend to only sell the products listed above, then the Series 6 exam may be an attractive option since it is shorter than the Series 7.

Common jobs in the securities and financial services industries that use the Series 6 are investment advisers, financial advisers, insurance agents, retirement plan specialists, and private bankers. Be aware, though, that some jobs might require other exams or qualifications in addition to the Series 6, depending on the duties required for a particular job. Salary ranges vary among these types of jobs, but the average base salary of people with a Series 6 certification is $56,000 per year (payscale.com).

To take the Series 6 exam, you must be sponsored by a FINRA member firm. The firm files a Form U4 application on your behalf through FINRA’s Central Registration Depository (CRD). Candidates must pass the co-requisite Securities Industry Essentials (SIE) exam in addition to the Series 6 to obtain the Series 6 license. Although you can take the exams in any order, Solomon Exam Prep recommends taking the SIE exam first because it is a foundational exam. Anyone 18 or older can take the SIE exam, and it doesn’t require firm sponsorship.

About the Exam

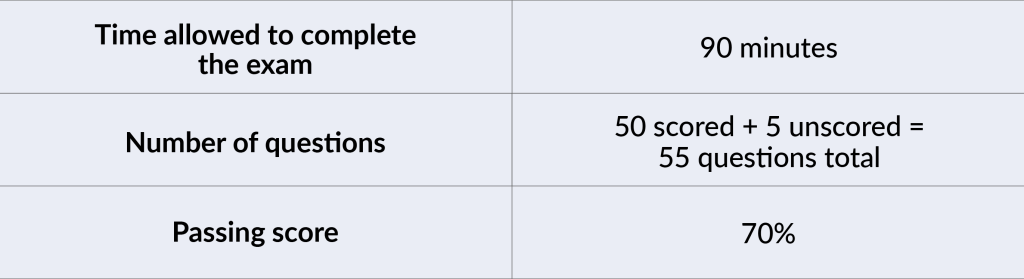

The Series 6 exam consists of 50 scored and 5 unscored multiple-choice questions covering the four sections of the FINRA Series 6 exam outline. The 5 additional unscored questions are ones that the exam committee is trying out. These are unidentified and are distributed randomly throughout the exam. FINRA updates its exam questions regularly to reflect the most current rules and regulations.

Note: Scores are rounded down to the next lowest whole number (e.g. 69.9% would be a final score of 69% – not a passing score for the Series 6 exam).

Topics Covered on the Exam

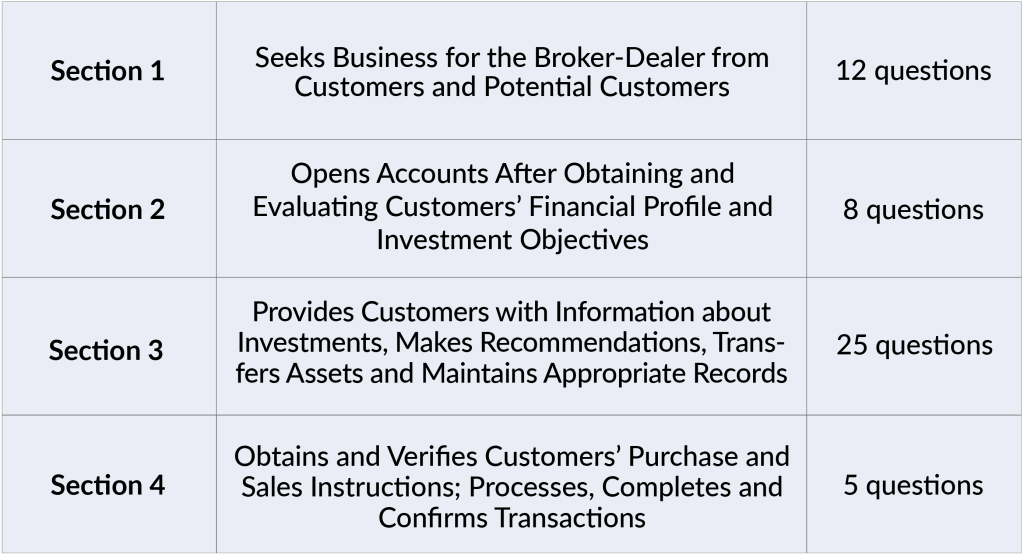

FINRA divides the Series 6 exam into four sections which represent the four job functions of a Series 6 registered representative:

The Series 6 exam covers many topics including the following:

Securities Registration

Communications

Client Accounts

Retirement Plans

Equity Securities

Debt Securities

Taxation

Options

Investment Companies

Annuities

Portfolio Management and CAPM

Investment Goals

Securities Analysis

Completing and Confirming Transactions

Question Types on the Series 6

The Series 6 exam consists of multiple-choice questions, each with four options. You will see these question structures:

Closed Stem Format:

This item type asks a question and gives four possible answers from which to choose.

In the cooling-off period, which of the following would not be allowed?

Making an offer to sell a security with a preliminary prospectus

Taking orders for the security

Publishing a tombstone ad

Distributing a preliminary prospectus

Incomplete Sentence Format:

This kind of question has an incomplete sentence followed by four options that present possible conclusions.

Regulation S-P helps protect customers from:

Recommendations to purchase high-risk securities such as S&P 500 index derivatives

Abusive commissions and sales charges

Having their private information misused

Money laundering

“EXCEPT” Format:

This type requires you to recognize the one choice that is an exception among the four answer choices presented.

All of the following would be considered a security except:

Publicly traded stock

Publicly traded bond

A variable annuity

A commodities future

Complex Multiple-Choice (“Roman Numeral”) Format:

For this question type, you see a question followed by two or more statements identified by Roman numerals. The four answer choices represent combinations of these statements. You must select the combination that best answers the question.

Regarding its telemarketing efforts, a firm or its representative must do which of the following?

Identify themselves and the purpose of their call

Compare potential prospects against the FTC’s National Do Not Call Registry

Be licensed by FINRA as a telemarketer

Establish a 900 number for potential complaints

I and IV

I and II

II and III

III and IV

This format is also used in items that ask you to rank or order a set of items from highest to lowest (or vice versa), or to place a series of events in the proper sequence.

Rank the following yields for a premium bond held to maturity from highest to lowest.

Yield to call

Coupon rate

Yield to maturity

Current yield

II, IV, III, I

IV, I, III, II

II, IV, I, III

III, I, IV, II

For an even better idea of the possible question types you might encounter on the Series 6 exam, try Solomon Exam Prep’s free Series 6 Sample Quiz.

How to Study for the Series 6

Follow Solomon Exam Prep’s proven study system:

Read and understand. Read the Solomon Study Guide, carefully. The Series 6 is a knowledge test, not an IQ test. Many students read the Study Guide two or three times before taking the exam. To increase your ability to focus while reading, or as an alternative to reading, listen to the Solomon Series 6 Audiobook, which is a word-for-word reading of the Solomon Series 6 Study Guide.

Answer practice questions in the Solomon Exam Simulator. When you’re done with a chapter in the Study Guide, take 4–6 chapter quizzes in the Solomon Online Exam Simulator. Use these quizzes to give yourself practice and to find out what you need to study more. Make sure you read and understand the question rationales. When you’re finished reading the entire Study Guide, review your handwritten notes once more. Then, and only then, start taking full practice exams in the Series 6 Exam Simulator. Aim to pass at least six full practice exams and try to get your Solomon Pass Probability™ score to at least an 80%; when you reach that point, you are probably ready to sit for the Series 6 exam.

Use these effective study strategies:

Take handwritten notes. As you read the Study Guide, take handwritten notes and review your notes every day for 10 to 15 minutes. Studies show that the act of taking handwritten notes in your own words and then reviewing them strengthens learning and memory.

Make flashcards. Making your own flashcards is another powerful and proven method to reinforce memory and strengthen learning. Solomon also offers digital flashcards for the Series 6 exam.

Research. Research anything you do not understand. Curiosity = learning. Students who take responsibility for their own learning by researching anything they do not understand get a deeper understanding of the subject matter and are much more likely to pass.

Become the teacher. Studies show that explaining what you are learning greatly increases your understanding of the material. Ask someone in your life to listen and ask questions. If you don’t have anyone, explain it to yourself. Studies show that helps almost as much as explaining to an actual person (see Solomon’s recent post to learn more about this strategy!).

Take advantage of Solomon’s supplemental tools and resources:

Use all the resources. The Resources folder in your Solomon student account has helpful information, including a detailed study schedule that you can print out – or use the online study schedule and check off tasks as you complete them.

Watch the Video Lecture. This provides a helpful review of the key concepts in each chapter after reading the Solomon Study Guide. Take notes to help yourself stay focused.

Good practices while studying:

Take regular breaks. Studies show that if you are studying for an exam, taking regular walks in a park or natural setting significantly improves scores. Walks in urban areas or among people did not improve test scores.

Get enough sleep during the period when you are studying. Sleep consolidates learning into memory, studies show. Be good to yourself while you are studying for the Series 6: exercise, eat well, and avoid activities that will hurt your ability to get a good night’s sleep.

You can pass the FINRA Series 6! It just takes focus and determination. Solomon Exam Prep is here to support you on your journey to becoming a registered Investment Company Products/Variable Life Contracts Representative.

To explore all Solomon Exam Prep Series 6 study materials, including product samples, visit the Solomon website here.

For more helpful securities exam-related content, study tips, and industry updates, join the Solomon email list. Just click the button below:

Solomon Exam Prep’s latest partnership will bring its Securities Industry Essentials (SIE) exam curriculum to a new UNC Pembroke course. Continue reading

Solomon Exam Prep is thrilled to announce its newest university partnership, with the University of North Carolina at Pembroke. Mohammad Rahman, Ph.D., Associate Professor in the School of Business, will be using Solomon Exam Prep’s Securities Industry Essentials (SIE) curriculum for a new finance course called Financial Trading. The online elective is running this Fall 2021 semester and will give students the opportunity to dive into the world of investing, plus help prepare them to take the SIE exam.

In the course, students will learn about trading environments, processes, and strategies. Topics covered include order types, trading terminology, hedging strategies, trading costs, market structure, and regulatory environments. Market simulations will be used to aid students’ understanding of executing trades, the application of trading strategies, and tracking performance metrics.

Bring the SIE to Your Campus

Interested in how you could incorporate Solomon Exam Prep’s study materials into a course at your college or university? Solomon’s flexible SIE curriculum can be tailored to meet the needs of a variety of classes. Students receive Solomon’s industry-leading online study materials at a discounted educational rate, and instructors benefit from high-touch support and access to the Instructor Portal with its innovative classroom tools and reporting features. And Solomon’s SIE curriculum is perfect for both in-person and online courses.

I just want to thank Solomon Exam Prep for a great semester! We taught this curriculum at Widener University for the first time. The Solomon team was great to work with! Always available, very responsive and eager to help. The online offering is very comprehensive and we didn’t miss a beat when we switched to remote learning. The QwizBang game was a big hit with the students (although more fun when we were all in the same room.) I can’t thank them enough for all that they have done.

Maggie Creed, Widener University, Chester, PA

Join institutions such as the University of Delaware, Adelphi University, University of Nebraska-Omaha, Seton Hall University, Ohio Dominican University, Georgetown University, Widener University, and University of Dallas in partnering with Solomon.

To learn more about the ways colleges and universities can partner with Solomon, visit the website or contact Beth Hamilton, Higher Education Development Manager, at beth@solomonexamprep.com or 503-601-0212.

Principals at municipal advisor firms must pass the Series 54 exam by November 12, 2021, to continue acting as principals. Continue reading

When the Municipal Securities Rulemaking Board (MSRB) created an exam specifically for principals at municipal advisor (MA) firms, the plan was for all MA principals to take it within a year.

The exam, known as the Series 54, was first made available on November 12, 2019. The MSRB required that all MA principals who wanted to continue acting as principals would have to pass the Series 54 by November 12, 2020.

But like many plans in 2020, the MSRB’s plan for the Series 54 was disrupted by Covid-19. With FINRA testing centers shut down for months, and uncertainty regarding when testing would resume, the MSRB added a one-year grace period to its original deadline. MA principals would now have until November 12, 2021, to pass the Series 54 exam.

The regulator recently reminded MA firms that “those who engage in the management, direction or supervision of…municipal advisory activities” will need to pass the Series 54 on or before November 12.

UPDATE: On August 11, the MSRB announcedthat it would seek SEC approval for an additional extension. The MSRB did not say how long the planned extension would be, but the regulator plans to announce this by September 10. The MSRB also announced an “interim accommodation” allowing those who need to take the Series 54 exam online to do so. Details about how to apply for this accommodation will be posted on MSRB.org no later than August 20.

UPDATE: On September 2, the MSRB announced that it has filed a request with the SEC to extend the Series 54 deadline from November 12 to November 30, 2021. View the blog post about this announcement here.

What is a Municipal Advisor?

A municipal advisor, or MA, differs from a municipal securities dealer in that an MA does not underwrite and sell municipal securities. Instead, an MA gives advice about structuring an issue of municipal securities, selecting an underwriter, investing the proceeds, and related matters. Unlike a municipal securities dealer, an MA is the municipality’s fiduciary, which means that the MA must put the municipality’s interests before its own. MAs became regulated in a manner like municipal securities dealers as one of the reforms resulting from the 2008 financial crisis.

When MAs first came under the MSRB’s jurisdiction, the MSRB only had one qualification exam for MA personnel: the Series 50, which is taken by representatives and principals alike. During the grace period, principals who have only passed the 50 have been allowed to continue as principals. After the deadline, MA principals will need to have passed both the Series 50 and the Series 54.

Solomon Exam Prep has helped hundreds pass the Series 50 and Series 54 exams.

Solomon offers an innovative suite of exam prep products for the Series 54 to help you pass this difficult test, plus a step-by-step study schedule to tell you how to do it. Choose from an easy-to-understand Study Guide, an Exam Simulator with hundreds of relevant practice questions and detailed rationales, and a Video Lecture to help you learn and highlight the most critical information for the exam.

Solomon recommends at least 40 hours of studying to give yourself the best chance at passing this challenging principal exam.

Do yourself a favor and start studying well before the deadline, and let Solomon help you on your road to success! Explore Solomon’s Series 54 study materials by clicking the link below.

Preparing for the SIE, Series 63, Series 79, Series 82, or another securities licensing exam? Read about one Solomon Exam Prep student’s path to success. Continue reading

Passing a securities licensing exam is no small feat, but four? Solomon Exam Prep recently reached out to Fernando Russo, Vice President of Investment Banking at Young America Capital, to learn more about his success in passing the SIE, Series 82, Series 63, and Series 79 exams (in that order). Whether you need to pass one or multiple exams to reach your career goals, you’ll want to hear about Fernando’s process and helpful tips.

“The content is not rocket science and the math is very simple. It just takes time, dedication and good study materials.”

Fernando Russo

Solomon Exam Prep: Why did you take your exams in the order that you did? Was this order helpful, or would you change anything if you had to do it again?

Fernando Russo: After the SIE I decided to take the 82 first because I wanted to be licensed as soon as possible. The materials for the 82 seemed simple and I felt confident that I could pass. The 63 came right after because it allowed me to offer securities in my state and be fully registered as an investment banker. The 63 is actually very tricky because it is prepared by NASAA and not by FINRA. Some of the materials are similar but the exam is very different from FINRA exams.

I took the 79 last.

I could’ve gone straight for the 79 but I think that taking the 82 was a good way to get started. It helps build up confidence and knowledge.

The 82, for some, might feel like a practice exam for the 79.

Solomon Exam Prep: Out of the exams you passed, which one required the most study time and why?

Fernando Russo: The 63 is trickier than most people think it is. The study materials are not as extensive as the 79 but the content is very specific and one needs to remember very detailed pieces of information (dates, percentages, etc.). I was studying a lot (2-3 hours a day during the week and 4-6 hours during weekends) but not getting the scores that I wanted on my practice exams, so I had to go back to the books and memorize 85% of the materials.

I spent 25% more time studying for the 63 than for the 79.

“The audiobooks are great. I would listen to the chapters while driving, while working out and while doing many other activities.”

Solomon Exam Prep: How did you approach studying for your exams?

Fernando Russo: I studied each chapter and then took a practice exam for that specific content or section. If I didn’t do well, I would go back to the materials and do it all over again until I passed. I did that over and over and over until I passed. I also found a lot of help in the notes that are found in the Resources Folder. These are great to find definitions, tables and simple explanations for seemingly complicated terms. The audiobooks are great. I would listen to the chapters while driving, while working out and while doing many other activities.

Solomon Exam Prep: How did you take the exams – at a testing center or remotely? How was your experience, and do you have any tips to share?

Fernando Russo: I took all my exams at the same Prometric test center in Chicago, and I did so on Monday mornings. I took Friday off from work and studied all day on Friday and on Saturday. On Sunday, the day before each exam, I did not study at all. Instead of studying I spent the whole day doing a fun activity with my family.

I think that is very necessary to allow the mind to rest before the exam. For each test I studied 30-45 days nonstop and one day of peace before the exam felt necessary. It worked. Each time I woke up the day of the test I felt relaxed and ready.

Solomon Exam Prep: Any words of wisdom to help motivate others who are preparing for exams?

Fernando Russo: Take the practice exams. Take them 1,000 times and then some more. I also recommend studying every day, even 10-15 minutes if the student is swamped with other activities. It keeps the mind engaged and the program moving forward. The content is not rocket science and the math is very simple. It just takes time, dedication and good study materials.

Visit the Solomon Exam Prep website to explore study materials for 21 different securities licensing exams, including the SIE, Series 63, Series 79, and Series 82.

What is the Series 65 exam and how should you prepare for it? Read Solomon Exam Prep’s guide to the NASAA Series 65 exam. Continue reading

What does the NASAA Series 65 allow me to do?

The Series 65, also known as the Uniform Investment Adviser Law Examination, qualifies individuals to give investment advice for a fee. Investment adviser representatives (IARs) use their knowledge to give financial advice and help clients build investment portfolios. IARs might provide general investment advice or recommend a client to invest in a specific security. IARs can also manage client accounts and supervise other IARs.

The organization that creates the test—the North American Securities Administrators Association, or NASAA—works to protect investors in every state, territory, the District of Columbia, Canada, and Mexico. Requiring investment adviser representative candidates to pass the Series 65 is a key tool in the NASAA’s investor protection arsenal. Regulators want to make sure people who are giving investment advice in their state or jurisdiction are competent and will behave legally and ethically.

About the Exam

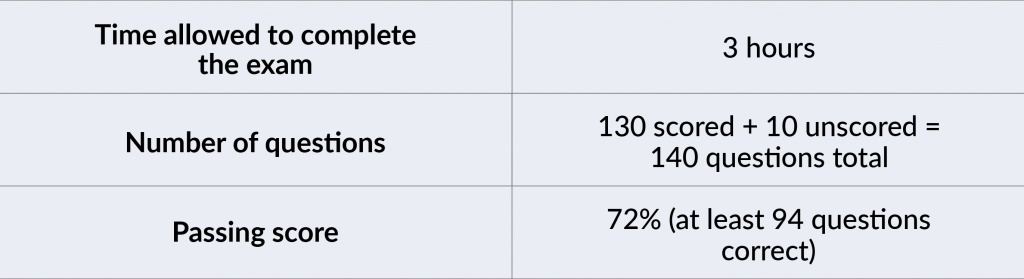

The Series 65 exam consists of 130 scored and 10 unscored multiple-choice questions covering the four sections of the NASAA Series 65 exam outline. The 10 additional unscored questions are ones that the exam committee is trying out. These are unidentified and are distributed randomly throughout the exam. NASAA updates its exam questions regularly to reflect the most current rules and regulations.

Note: Scores are rounded down to the lowest whole number (e.g. 71.9% would be a final score of 71%–not a passing score for the Series 65 exam).

Topics Covered on the Exam

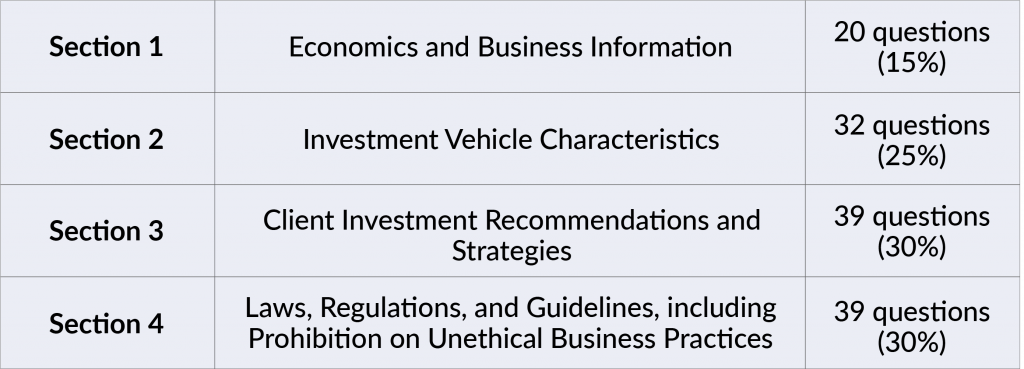

The NASAA divides the Series 65 exam into four sections:

The Series 65 exam covers many topics including the following:

Economics

Financial reporting

Quantitative methods

Risks

Cash investments

Fixed income

Equities

Pooled investments, such as mutual funds, ETFs, and REITs

Derivatives

Alternatives

Annuities and other insurance-based investments

Client types

Client profiles

Capital market theory

Portfolio management

Taxes

Retirement plans

ERISA

Special accounts, such as college savings plans

Trading securities

Performance measures

State and federal securities acts and regulations

Ethical practices and fiduciary obligations

Question Types on the Series 65

The Series 65 exam consists of multiple-choice questions, each with four options. You will see these question structures:

Closed Stem Format:

This item type asks a question and gives four possible answers from which to choose.

Which of the following actions might the Federal Reserve take if it wishes to stimulate the economy?

Buy Treasuries

Raise the discount rate

Raise the bank reserve requirements

Raise the margin requirements

Incomplete Sentence Format:

This kind of question has an incomplete sentence followed by four options that present possible conclusions.

A recession is a protracted period of decline in the national economy, typically defined as:

More than two quarters of decreasing GDP

More than two quarters of decline in the housing market

More than two quarters of shrinking M1

More than two quarters of a falling PPI

“EXCEPT” Format:

This type requires you to recognize the one choice that is an exception among the four answer choices presented.

All of the following are tools that the Federal Reserve uses to implement monetary policy except:

Open market operations

Discount window lending

Altering bank reserve requirements

Altering the value of the dollar

Fill-in-the-Blank Format:

This question type has a missing word or phrase, which you must select from the four options provided.

A situation in which short-term securities pay higher yields than long-term securities is considered a(n) _____ yield curve.

Normal

Inverted

Flat

Barbell

Complex Multiple-Choice (“Roman Numeral”) Format:

For this question type, you see a question followed by two or more statements identified by Roman numerals. The four answer choices represent combinations of these statements. You must select the combination that best answers the question.

A stronger dollar benefits which group?

U.S. exporters

U.S. importers

U.S. investors who want to invest in foreign assets

Overseas investors who want to invest in U.S. assets

I and II

II and III

III and IV

I and IV

This format is also used in items that ask you to rank or order a set of items from highest to lowest (or vice versa), or to place a series of events in the proper sequence.

Order the following from lowest to highest:

Broker call rate

Federal funds rate

Prime rate

Discount rate

I, IV, III, I

III, II, I, IV

IV, III, I, II

II, IV, I, III

How to Study for the Series 65

Follow Solomon Exam Prep’s proven study system:

Read and understand. It’s simple: read the Solomon Study Guide, carefully. The Series 65 is a knowledge test, not an IQ test. Many students read the Study Guide two or three times before taking the exam. To increase your ability to focus while reading, or as an alternative to reading, listen to the Solomon Audiobook, which is a word-for-word reading of the Solomon Study Guide.

Answer practice questions in the Solomon Exam Simulator. When you’re done with a chapter in the Study Guide, take 4 – 6 chapter quizzes in the Solomon Online Exam Simulator. Use these quizzes to give yourself practice and to find out what you need to study more. Make sure you read and understand the question rationales. When you’re finished reading the entire Study Guide, review your handwritten notes once more. Then, and only then, start taking full practice exams in the Exam Simulator. Aim to pass at least six full practice exams and try to get your average score to at least an 80; when you reach that point, you are probably ready to sit for the Series 65 exam.

Use these effective study strategies:

Take handwritten notes. As you read the Study Guide, take handwritten notes and review your notes every day for 10 to 15 minutes. Studies show that the act of taking handwritten notes in your own words and then reviewing them strengthens learning and memory.

Make flashcards. Making your own flashcards is another powerful and proven method to reinforce memory and strengthen learning. Solomon also offers digital flashcards for the Series 65 exam.

Research. Research anything you do not understand. Curiosity = learning. Students who take responsibility for their own learning by researching anything they do not understand get a deeper understanding of the subject matter and are much more likely to pass.

Become the teacher. Studies show that explaining what you are learning greatly increases your understanding of the material. Ask someone in your life to listen and ask questions. If you don’t have anyone, explain it to yourself. Studies show that helps almost as much as explaining to an actual person (see Solomon’s recent post to learn more about this strategy!).

Take advantage of Solomon’s supplemental tools and resources:

Use all the resources. The Resources folder in your Solomon student account has helpful information, including a detailed study schedule that you can print out – or use the online study schedule and check off tasks as you complete them.

Watch the Video Lecture. This provides a helpful review of the key concepts in each chapter after reading the Solomon Study Guide. Take notes to help yourself stay focused.

Good practices while studying:

Take regular breaks. Studies show that if you are studying for an exam, taking regular walks in a park or natural setting significantly improves scores. Walks in urban areas or among people did not improve test scores.

Get enough sleep during the period when you are studying. Sleep consolidates learning into memory, studies show. Be good to yourself while you are studying for the Series 65: exercise, eat well, and avoid activities that will hurt your ability to get a good night’s sleep.

You can pass the NASAA Series 65! It just takes work and determination. Solomon Exam Prep is here to support you on your journey to becoming a registered Investment Adviser Representative.

For more helpful securities exam-related content, study tips, and industry updates, join the Solomon email list. Just click the button below:

Solomon Exam Prep explains what a Series 7 General Securities Representative can and cannot do and how this compares to other rep-level registrations. Continue reading

Of the representative-level FINRA registrations categories, the General Securities Representative (Series 7) registration is considered by many to be the most valuable, due to the range of products it allows you to sell. But how “general” is it? Are there other representative-level registrations that permit you do things a Series 7 representative cannot?

What is a Series 7 representative permitted to do?

FINRA allows a General Securities Representative to solicit the purchase and sales of all securities products, including:

Stocks, whether from IPOs, private placements, or secondary market trading

Other corporate securities, such as bonds, rights, and warrants

Mutual funds

Closed-end funds

Money market funds

Unit investment trusts (UITs)

Exchange-traded funds (ETFs)

Real estate investment trusts (REITs)

Variable contracts (insurance products whose funds are invested in securities)

Municipal securities

Municipal fund securities, such as 529 plans

Options

Government securities

Direct participation programs (DPPs)

Venture capital

Hedge funds

This long list of products means that a Series 7 registered rep may perform the functions of an Investment Company and Variable Contracts Representative (Series 6), Direct Participation Programs Representative (Series 22), or Private Securities Offerings Representative (Series 82).

Besides sales, General Securities Representatives may also perform certain activities closely related to sales. They may:

recommend investments after performing a suitability analysis for the customer

accept unsolicited orders

open customer accounts, subject to approval by a principal

What is a Series 7 representative NOT permitted to do?

Though a General Securities Representative may solicit purchases of IPO shares, he may not work on underwriting or structuring an IPO, or any other securities offerings. This means that he is not permitted to advise an issuer on an offering. This work requires registration as an Investment Banking Representative (Series 79). Likewise, working on municipal underwriting requires registration as a Municipal Securities Representative (Series 52).

A Series 7 representative is also not qualified to perform the back-office functions of an Operations Professional (Series 99). Among these functions are maintaining possession or control of the firm’s securities, calculating margin for margin accounts, and sending trade confirmations and account statements.

Of course, every registered representative must also pass the FINRA Securities Industry Essentials (SIE) exam. The SIE doesn’t qualify you to do anything, instead it is a foundational exam that focuses on industry terminology, securities products, the structure and function of the markets, regulatory agencies and their functions, and regulated and prohibited practices. Unlike other FINRA securities exams, you do not need to be employed or sponsored by a broker-dealer in order to take the SIE. The only requirement is that you be 18 years old.

If you’re considering taking the Series 7 exam, Solomon Exam Prep is here to help. Solomon provides a wide variety of study materials, together with resources such as study schedules, the Ask The Professor function, and helpful exam information. Explore Solomon’s Series 7 study materials.

Options are a common topic on the Series 6, Series 7, Series 65, Series 66, and SIE exams. Read our guide to calculating gains and losses on exercised options. Continue reading

Options are a topic that many taking the Series 6, Series 7, Series 65, Series 66, and SIE exams have to deal with. One of the biggest problems that students have with options questions occurs when they are asked to calculate gains and losses on exercised options. As long as you understand a few basic points, these types of questions can be a breeze and definitely nothing to lose sleep over.

First of all, let’s remind ourselves of what an option is. An option is a contract between two parties that gives the buyer of the contract the right to buy or sell an underlying asset to the other party in the future for a specific price. The specific price is called the “exercise” or “strike” price. The seller of the option, on the other hand, is obligated to buy or sell, at the strike price. The option to buy is a “call” option, the option to sell is a “put” option.

To calculate gains and losses on exercised options, you first need to understand what is happening as a result of an options transaction. When an option is exercised, that means its holder chooses to either buy or sell the underlying security at the strike price. With an exercised call option, the holder purchases shares of the underlying security from the options seller; with an exercised put option, the holder sells shares of the underlying security to the options seller. The sale in each case occurs at the option’s strike price.

Buying – Exercised Call Option

When a call options holder exercises her option by purchasing the underlying shares, she must add the cost of those shares to the premium she paid to obtain the option in the first place. This sum represents the option holder’s total money spent as a result of her options transaction. If the option holder then elects to sell the underlying securities she’s just purchased at their current market price, the money she receives from the sale will be money she takes in. To calculate her gain or loss, subtract the money she paid out from the money she took in. It’s as simple as that.

So, if, for instance, Marie paid $200 in premiums to purchase a call option with a strike price of $20 and then exercised the option by purchasing 100 shares of the underlying stock, the money she spent as a result of her options transaction will be $2,200 ($200 premium paid + $2,000 purchase price for underlying securities). If she then sells those 100 shares at the market price of $25, she will receive $2,500 in sales proceeds. Subtracting the money she spent from the amount she received will result in a $300 gain ($2,500 sale proceeds – $2,000 purchase price – $200 premium paid = $300 gain.)

Buying – Exercised Put Option

In order for a put options holder to exercise his option, he must have 100 shares of the underlying security to sell to the options seller. That means he needs to go out in the market and purchase shares at their market price. The money he pays for those securities plus the premium he paid to purchase his put option in the first place represents money spent as a result of his options transaction. The options holder will then sell those 100 shares to the options seller at the strike price. When he does this, he receives the sale proceeds. Subtracting the money spent on the put from the sale proceeds will result in the put investor’s gain or loss.

So, if, for instance, Pierre paid $300 in premiums to purchase a put option with a strike price of $30 and then purchases 100 shares of the underlying stock when its market price drops to $25, he will have spent $2,800 as a result of his options transaction ($300 premium + $2,500 purchase price for underlying shares). He will then sell those 100 shares to the options seller at their strike price of $30 and take in $3,000 from his sale. Thus, Pierre will make a total of $200 on his options transaction ($3,000 sale proceeds - $300 premium – $2,500 purchase price = $200 gain).

Selling an Option

Now let’s look at gains or losses from the perspective of an options seller. Remember that when someone sells an option, he receives the premium from the options buyer. If the option expires unexercised, the seller gets to keep his entire premium received, which represents his maximum potential gain. If the option is exercised, he will either be required to sell shares of the underlying security to the option holder in the case of a call option or buy shares from the option holder in the case of a put option. Each of an exercised call or an exercised put option transaction is made at the option’s strike price.

Selling – Exercised Call Option

When a call option is exercised, the option seller must obtain 100 shares of the underlying stock to sell to the options holder. To do so, he will have to purchase the shares at their current market price, which will be higher than the option’s strike price. He will then sell them to the option holder at the strike price. The money he takes in from the sale is added to the premiums he received when shorting the option, and this totals the money he takes in as part of his options transaction. The money he paid to obtain the underlying securities is the money he pays out. Subtracting the money he pays out from the money he takes in results in his overall gain or loss.

For example, let’s say Michael sells a call option with a strike price of $50 and receives premiums totaling $500. If the option is exercised, and Mike purchases the underlying shares at $55, he will have paid out $5,500 as a result of his options transaction. At the same time, he will have received $5,500 ($500 premium + $5,000 strike price). Thus, Mike will break even on this transaction; money taken in will be equal to money paid out.

Buying – Exercised Put Option

When a put option is exercised, the option seller must purchase 100 shares of the underlying security from the options holder at the strike price. This represents money the options seller pays out. The options holder has already received the premium when she sold the option, and after purchasing the 100 shares, she can sell them for their current market price. The combination of the seller’s sale proceeds and the premium received represents money taken in. Subtracting money paid out from money taken in will result in the investor’s gain or loss.

Let’s say Maribel shorts a put option and receives premiums totaling $400. The option has a strike price of $40, and the option holder exercises it when the underlying stock is trading at $35. This means Maribel is obligated to pay $4,000 total for the 100 underlying shares. This is money she pays out. She has already taken in $400, and if she chooses to sell the underlying stock at its current market price, she will take in an additional $3,500 in sales proceeds. This means she will receive a total of $3,900 from his options transaction ($3,500 sale proceeds + $400 premium) and paid out a total of $4,000. As a result, she has lost $100 on his options transaction ($3,900 money in – $4,000 money out = -$100).

As long as you understand what is occurring when an option is exercised, calculating gains and losses is as simple as comparing the money the investor takes in to the money she pays out. Calculating gains and losses on exercised options requires an understanding of the transaction and some simple math. Follow the guidance above and you will be able to correctly answer this type of question on your securities licensing exam.

For more helpful securities exam-related content, study tips, and industry updates, join the Solomon email list. Just click the button below:

If you’re studying for securities licensing exams, such as the SIE or the Series 7, then you should understand the terms “accredited investor” and “QIB.” Continue reading

If you’ve been studying for the Series 7, 6, 14, 22, 24, 65, 79, or 82, or the Securities Industry Essentials (SIE), then you’ve had to learn about Regulation D private placements and Rule 144A sales. Regulation D private placements are securities offerings that are exempt from the normal SEC registration process and in many cases are sold only to “accredited investors” or limit the involvement of investors who are not accredited. Rule 144A sales are sales of unregistered securities to large institutional investors known as “qualified institutional buyers” or QIBs for short.

You may have wondered about the difference between accredited investors and QIBs. On the surface, these may seem similar. Each refers to a category of investor with resources and/or knowledge above and beyond the average retail investor. So why not just have one standard for buyers under both Rule 144A and Regulation D? After all, the purpose of both Regulation D and Rule 144A is the same: to allow wealthier and more sophisticated investors easier access to investments that may be too risky for the average investor.

To begin to answer this question, we have to start with the fact that wealth and sophistication fall on a spectrum. Investors aren’t neatly divided between small retail investors and huge financial institutions that move millions around without blinking an eye.

Accredited Investors

You could think of accredited investors as a middle ground between these two extremes. Accredited investors are investors whose financial status or investment knowledge may give them a greater ability to handle the risks inherent in a private placement. There are many ways to qualify as an accredited investor but they all have one thing in common, which is that the SEC believes they indicate an ability to take on risks that regulators believe are unsuitable for most retail investors.

Accredited investors are investors whose financial status or investment knowledge may give them a greater ability to handle the risks inherent in a private placement.

All of the following are considered accredited investors:

Banks, broker-dealers, investment advisers, insurance companies, and investment companies

Corporations, trusts, partnerships, and LLCs with more than $5 million in assets

Most employee benefit plans with more than $5 million in assets

The issuer’s directors, executive officers, and general partners

If the issuer is a privately owned fund, (such as a hedge fund), a knowledgeable employee of the fund, which means an employee with at least 12 months’ experience working on the fund’s investment activities

Individuals with income of $200,000 in each of the last two years, or $300,000 in combination with a spouse or spousal equivalent such as a domestic partner

Individuals with a net worth more than $1 million, alone or with a spouse or spousal equivalent, not including primary residence

Individuals who hold any of these three designations in good standing:

Licensed General Securities Representative (Series 7)

Any firm where all owners are accredited investors (e.g., venture capital firms)

Any other entity with more than $5 million in investments that was not formed specifically to qualify as an accredited investor; the purpose of this category is to include entities that don’t neatly fit into any of the above categories, such as:

Native American tribes

Labor unions

Government bodies, including those of foreign governments

Investment funds created by government bodies

New types of business entities that may be introduced by new laws

An accredited investor that is not an individual—such as a business, governmental, or nonprofit entity—is sometimes called an institutional accredited investor (IAI).

Qualified Institutional Buyers

QIBs are a narrower group of large institutional investors. A QIB is a large institutional investor that owns at least $100 million worth of securities, not counting securities issued by its affiliates. For registered broker-dealers, the threshold is lower, just $10 million. A bank must also have a net worth of at least $25 million in order to be considered a QIB.

If a firm has discretionary authority to invest securities owned by a QIB, those securities count toward whether the firm itself is considered a QIB. So if a broker-dealer has $9 million worth of securities in its own accounts, and holds $1 million worth of securities in a discretionary account belonging to a QIB, then the broker-dealer is itself a QIB.

Common examples of QIBs include broker-dealers, insurance companies, investment companies, pension plans, and banks. However, any corporation, partnership, or LLC could qualify as a QIB. So can an IAI that owns at least $100 million in securities. Individuals can never be QIBs, regardless of their assets or financial sophistication.

Individuals can never be QIBs, regardless of their assets or financial sophistication.

Rule 144A allows QIBs to buy unregistered securities at any time, and freely trade these shares to other QIBs. In effect, QIBs can trade unregistered shares among themselves with almost the same ease as trading registered shares. Selling unregistered securities to anyone other than a QIB commonly requires a the seller to hold the securities for a period of up to 12 months.

A QIB will virtually always meet the criteria to be an accredited investor, whereas an accredited investor may fall well short of QIB status.

Over time, other securities laws and regulations have made use of these two well-known categories. For example, in 2019 the SEC gave issuers more flexibility to test the waters with potential investors before deciding whether to go through with a public offering. When deciding which investors were sophisticated enough to receive test-the-waters communications, the SEC limited these communications to QIBs and institutional accredited investors. Additionally, references to institutional accredited investors have become more common, such as when the SEC revamped its rules around integration of offerings in March 2021.

Know your QIBs from your accredited investors and be ready to pass your securities exam with Solomon Exam Prep.

For more helpful securities exam-related content, study tips, and industry updates, join the Solomon email list. Just click the button below: