Question: A Municipal Finance Professional (MFP) hosted a $500 plate fundraiser for a governmental issuer. Does this event trigger a ban on business for two years?

A. Yes, it will trigger a ban because an MFP may not host a fundraiser.

B. Yes, it will trigger a ban because the cost per plate is above the de minimis amount.

C. No, it will not trigger a ban because the MFP did not contribute money, only time and space.

D. No, it will not trigger a ban because the MFP was holding the fundraiser, not the municipal dealer.

Correct Answer: A

Explanation: MFPs are not permitted to solicit funds for municipal issuers or their officials without triggering a two-year ban on business for their firm. Thus, holding fundraisers is not allowed. Municipal dealers are also forbidden from holding fundraisers.

To explore free samples of Solomon Exam Prep’s industry-leading online exam simulators for the SIE, Series 7, Series 14, Series 50, Series 52, Series 54, and other FINRA, MSRB, NASAA, and NFA exams, visit the Solomon website here.

Read Solomon Exam Prep’s expert guide for answering state registration questions on the Series 63, Series 65, and Series 66 exams. Continue reading

If you’re planning to take the NASAASeries 63, Series 65, or Series 66 exam, you can expect to see questions about when broker-dealers and their securities agents need to register in a particular state. You can also expect to see questions about when investment advisers and investment adviser representatives need to register in a state. Instead of feeling intimidated when confronted with such questions, you should relax, smile, and feel confident. That’s because if you follow the simple rules that we’re about to describe, you should get each of these questions right.

Broker-Dealers and Their Agents

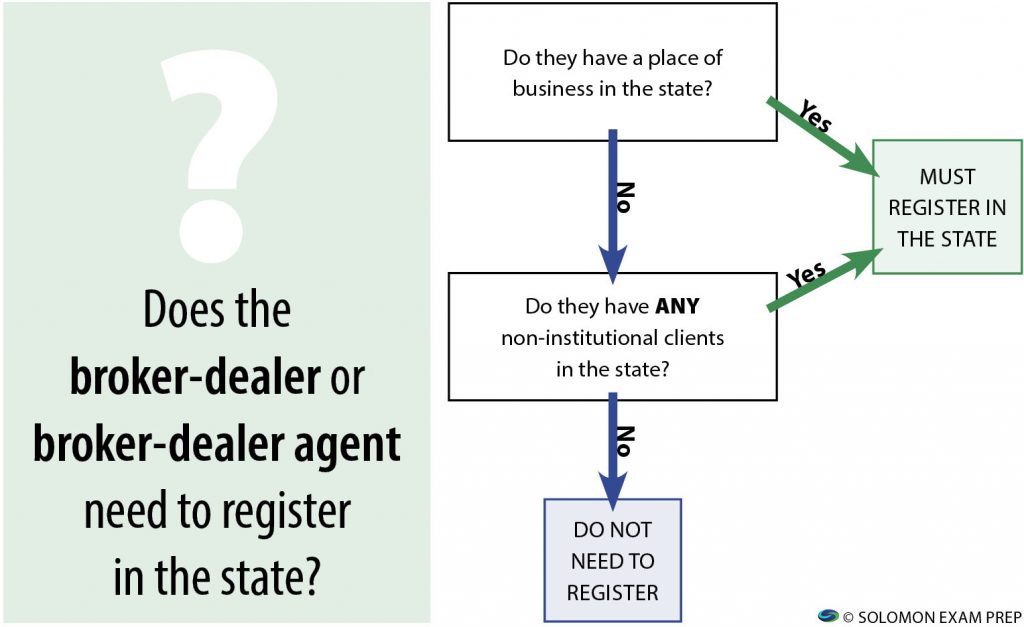

First let’s deal with questions about state registration for broker-dealers (BDs) and their agents. Rule number one here is that when a U.S.-based BD or one of its agents has an office located in a state, that BD or agent must register in the state. It does not matter which types of clients a BD or BD agent with an office in a state has or what types of securities those clients buy from the BD or agent. A BD or agent with an office in a state must register in that state. Period.

What about a BD or BD agent that doesn’t have an office in a state? If a BD or BD agent without an office in a state has any non-institutional clients in that state, the BD or agent must register there. However, if the BD or agent without an office in a state has only institutional clients in the state, no registration in that state is required. Institutional clients include the issuers of securities involved in a specific transaction; other broker-dealers; and institutional buyers, which are big-money entities such as banks, insurance companies, mutual funds, and pension and profit-sharing plans.

Key takeaway:

So when presented with a question about whether a specific broker-dealer or one of its agents must register in a given state or states, there are two potential questions to ask yourself. The first question is: “Does the broker-dealer or BD agent have an office in the state?” If the answer is yes, it’s simple: the BD or agent must register in that state. End of questions. However, if the answer is no, move on to the second question: “Does the BD or BD agent have any non-institutional clients in the state?” If the answer is yes, the BD or agent must register in the state; if the answer is no, they do not need to register in the state.

Here’s a flowchart to help you remember the question-answering process:

Investment Advisers and Their Representatives

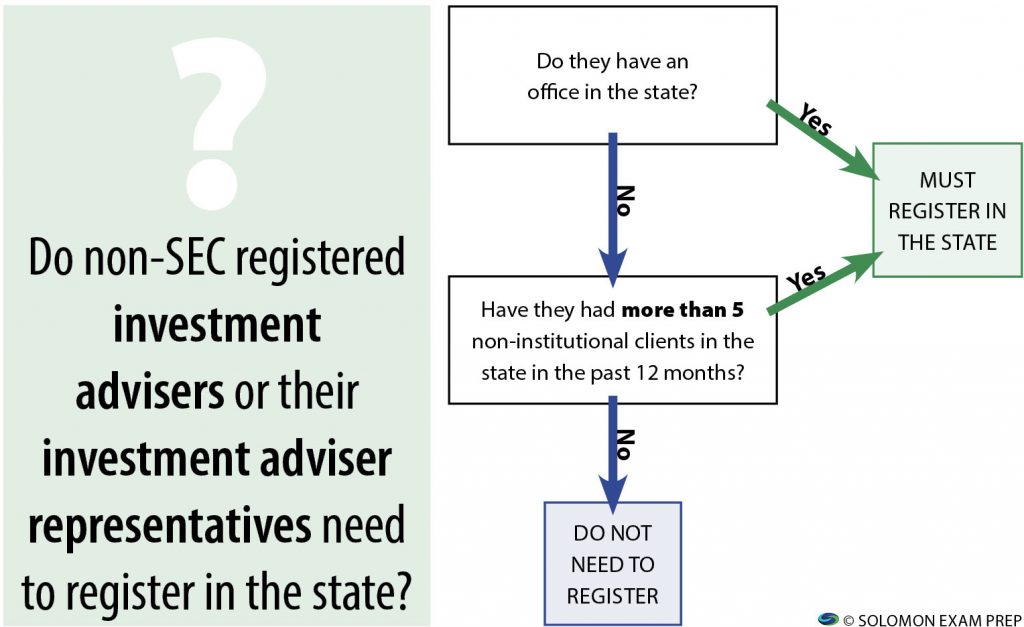

Now let’s look at the state registration requirements for investment advisers that do not register with the SEC. If the investment adviser has an office in the state, it must register there. If the investment adviser doesn’t have an office in the state but has had more than five non-institutional clients in the state during the past twelve months, it also must register there. The rules are the same for investment adviser representatives who work for an investment adviser that does not register with the SEC.

Investment adviser representatives who work for investment advisers that register with the SEC — also known as federal covered advisors — may need to register with the state if they have an office in the state.

Key takeaway:

So if you see a question about state registration requirements for non-SEC registered investment advisers or their investment adviser representatives, the first question to ask yourself is: “Does the IA or IAR have an office in the state?” If the answer is yes, you know the IA or IAR must register there. If the answer is no, move on to the second question: “Has the IA or IAR had more than five non-institutional clients in the state during the preceding twelve months?” If the answer is yes, they must register in the state; if the answer is no, they don’t need to register in the state.

Here’s another flowchart to help you with this type of question:

Remember that if an investment adviser registers with the SEC, it is a federal covered adviser and does not need to register in any state. Instead, a federal covered adviser must notice file to provide investment advice to residents of that state. When it comes to notice filing requirements for federal covered advisers, follow the same thought process as that described above. If the federal covered adviser has an office in a state, it must notice file there. If it has no office in the state but it has had more than five non-institutional clients in the state in the past twelve months, the firm must also notice file there.

Practice question

Simple, right? So let’s put the suggested thought process into practice by looking at a question like one you may see on your exam.

XYZ Broker Dealer has its main office in State A. It also has offices in States B and C. XYZ has non-institutional clients in states A and B, but it only has institutional clients in State C. It does not have an office in State D, but it has three non-institutional clients there. In which states does XYZ need to register?

A. State A only

B. States A and B only

C. States A, B, and C only

D. States A, B, C, and D

Remember the process to follow when you see questions about where a BD must register. There are two possible questions to address as part of that process.

First question: Does the broker-dealer have an office in a state? Answer: XYZ has offices in each of States A, B, and C. Recall that if the answer the first question is “yes, the BD has an office in the state”, then the BD must register in that state. So XYZ needs to register in States A, B, and C.

If the answer to the first question is no, as it is for State D, you move on to the second question: Does the BD have any non-institutional clients in the state? XYZ has non-institutional clients in State D, so the answer is yes to that question. If the answer to the second question is yes, this means the BD must register in the state. Thus, XYZ has to register in State D as well as States A, B, and C. So Choice D is the correct answer.

So now you’re an expert, and you’re one step closer to passing your Series 63, Series 65, or Series 66 exam!

Want more exam tips?

Watch a video version of “How to Answer State Registration Questions on the Series 63, Series 65, and Series 66” on the Solomon YouTube channel, where you’ll find even more exam and study tips!

Solomon Exam Prep has helped thousands pass their securities licensing exams, including the SIE and the Series 3, 6, 7, 14, 22, 24, 26, 27, 28, 50, 51, 52, 53, 54, 63, 65, 66, 79, 82 and 99.

This month’s study question from the Solomon Online Exam Simulator question database is now available. Continue reading

This month’s study question from the Solomon Online Exam Simulator question database is now available.

***Comment below or submit your answer to info@solomonexamprep.com to be entered to win a $20 Starbucks gift card.***

This question is relevant to the Series14, 79, 82, and SIE exams.

Question:

A research analyst who works for an underwriter that participated in an IPO may not publicly discuss or write a research report about the company until __________________.

Answer Choices:

A. 30 days after the registration is filed

B. 20 days after the securities are issued

C. 10 days after the date of the IPO

D. 30 days after the date of the IPO

Correct Answer: C – 10 days after the date of the IPO

Explanation: A research analyst who works for an underwriter of an IPO must not discuss or write a research report about the company for 10 days after the IPO. This 10-day period of silence is called a ‘quiet period.’ There is no quiet period for EGCs (emerging growth companies).

To explore free samples of Solomon Exam Prep’s industry-leading online exam simulators for the SIE, Series 14, Series 79, Series 82, and many more exams, visit the Solomon website here.

This month’s study question from the Solomon Online Exam Simulator question database is now available. Continue reading

This month’s study question from the Solomon Online Exam Simulator question database is now available.

***Comment below or submit your answer to info@solomonexamprep.com to be entered to win a $20 Starbucks gift card.***

This question is relevant to the Series7, 14, 51, 52, and 53 exams.

Question:

MSRB Rule G-38 states that a broker-dealer may not pay any person to solicit municipal securities business on its behalf who is not an affiliated person of the firm. For the purposes of the rule, an affiliated person is:

Answer Choices:

A. Any person who works for the firm

B. Only a partner, director, or officer of the firm

C. Only a registered employee of the firm

D. Only an unregistered clerical or ministerial employee of the firm

Correct Answer: A – any person who works for the firm

Explanation: An affiliated person is anyone who is a partner, director, officer, employee, or registered person of the broker-dealer.

This month’s study question from the Solomon Online Exam Simulator question database is now available. Continue reading

This month’s study question from the Solomon Online Exam Simulator question database is now available.

***Comment below or submit your answer to info@solomonexamprep.com to be entered to win a $20 Starbucks gift card.***

This question is relevant to the SIE, Series 6, 7, 22, 24, and 82 exams.

Question:

Which of the following people would be considered a specified adult?

Answer Choices:

A. A 16 year old with autism

B. A 30 year old

C. A 60 year old with a heart condition

D. An 18 year old in a coma

Correct Answer: D

Explanation: A specified adult is a natural person age 65 and older or a natural person age 18 and older who the member firm reasonably believes has a mental or physical impairment that renders the individual unable to protect his or her own interests.

This month’s study question from the Solomon Online Exam Simulator question database is now available. Continue reading

This month’s study question from the Solomon Online Exam Simulator question database is now available.

***Comment below or submit your answer to info@solomonexamprep.com to be entered to win a $20 Starbucks gift card.***

This question is relevant to the Series 6, 7, 14 and 79 exams.

Question:

Which of the following is not typically part of an underwriting agreement?

Answer Choices:

A. Description of the per-share underwriting spread

B. Description of a Greenshoe option

C. Terms between syndicate members and selling group dealers

D. Terms under which the underwriter can terminate the contract

Correct Answer: C

Explanation: The underwriting agreement, which is typically signed the evening before or the morning of the effective date of a securities issue typically includes the per-share underwriting spread, an over-allotment (Greenshoe) option if granted, and the underwriter’s termination rights. It also is the document that contains the public offering price or a formula to derive it.

This month’s study question from the Solomon Online Exam Simulator question database is now available. Continue reading

This month’s study question from the Solomon Online Exam Simulator question database is now available.

***Comment below or submit your answer to info@solomonexamprep.com to be entered to win a $20 Starbucks gift card.***

This question is relevant for the SIE and Series 7, 14, 24, 26, 27, 28, 51, 53, 65, 66, and 99 exams.

Question:

Which situation would a CTR need to be filed?

Answer Choices:

A. When a customer regularly, but on different days, deposits $9,900 into their account in cash.

B. When a person deposits checks for $11,000 every week.

C. A customer withdraws $10,500 from their account in cash.

D. A customer makes a $20,000 Venmo transaction.

Correct Answer: C

Explanation: A currency transaction report (CTR) is filed with FinCEN on cash transactions that exceed $10,000 in a single day, whether conducted in one transaction or several smaller ones. The transactions can be either deposits or withdrawals and they must be in cold, hard cash.

This month’s study question from the Solomon Online Exam Simulator question database is now available. Continue reading

This month’s study question from the Solomon Online Exam Simulator question database is now available.

***Submit your answer to info@solomonexamprep.com or comment below to be entered to win a Solomon temporary tattoo.***

Question:

Frank and Wilma Fertig are snowbirds. They spend periods of time in Arizona each winter and then return to their home in Wisconsin. They have been doing business with their broker-dealer and their agent, Michael, for almost 10 years. The broker-dealer is registered in Wisconsin but not in Arizona. This year Frank and Wilma left early for Arizona, in early October rather than their usual late October. On October 12, the broker-dealer contacted the Fertigs to ask them about using some of their current cash position to purchase shares of QRS Company. The Fertigs agreed. What happened next?

Answer choices:

The Fertigs went back to their golf game.

The Wisconsin state securities Administrator issued a cease and desist order against the Fertigs’ broker-dealer for conducting a securities transaction outside Wisconsin, where the broker-dealer is registered.

The Arizona state securities Administrator issued a cease and desist order against the Fertigs’ broker-dealer for conducting a securities transaction for Arizona residents without the broker-dealer being registered in Arizona.

Michael realized he misled the Fertigs about being able to complete the transaction in a state where neither he nor the broker-dealer is registered and had to call them to apologize and tell them the deal could not be completed.

Correct Answer: A. The Fertigs went back to their golf game.

Explanation: After agreeing to the transaction Michael proposed, the Fertigs went back to their golf game and the transaction was completed without negative consequences. The Uniform Securities Act allows broker-dealers to complete transactions for existing customers who are out of their state of residence temporarily, as the Fertigs are. That is, the broker-dealer is excluded from the requirement to register in a state if he/she has no place of business in the state, they are registered in another state, and they have an existing client who is in that state temporarily. In this case, they can continue to make trades for their vacationing client for up to 30 days. Hence, Michael can make this trade. Once a month has passed, however, he will not be able to make similar transactions for the Fertigs until they return to Wisconsin.

Answer this month’s study question for a chance to win! Continue reading

This question comes from the Solomon Exam Prep Online Exam Simulator question database for Series 65 & 66:

Under modern portfolio theory, which of the following is the most efficient set?

A. Expected return 9%, Standard deviation 8

B. Expected return 9%, Standard deviation 9

C. Expected return 11%, Standard deviation 8

D. Expected return 11%, Standard deviation 9

Correct Answer: C. Expected return 11%, Standard deviation 8

Rationale: According to modern portfolio theory (MPT), the investment opportunity set consists of all available risk-return combinations. Standard deviation is the measure of volatility used in MPT. Assuming a normal distribution of returns, 68% of all returns will fall within one standard deviation of the mean return and 95% of all returns will fall within two standard deviations of the mean return. An efficient portfolio is a portfolio that has the highest possible expected return for a given standard deviation. In this question, the highest expected return with the lowest standard deviation is 11% and 8.