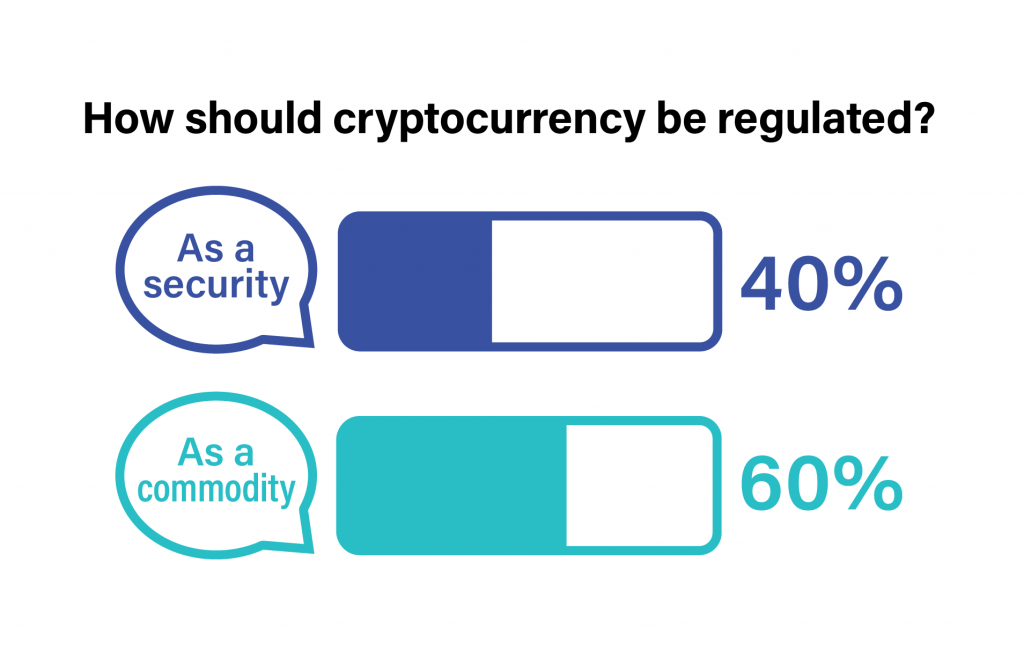

Read the results of Solomon Exam Prep’s latest poll on the topic of cryptocurrency regulation – and learn which license you’d need for either outcome. Continue reading

With the regulatory status of Bitcoin and other cryptocurrencies still up in the air, a recent Solomon LinkedIn poll found that 60% of Solomon customers think cryptocurrencies should be treated as commodities, while 40% said they thought cryptocurrencies should be regulated as securities.

Thus far the SEC has avoided clearly stating that cryptocurrencies are securities. To do so, the SEC would likely have to show that cryptocurrencies meet the “Howey Test,” which says that securities must have four characteristics. According to this test, a security involves (1) an investment of money that (2) involves a common enterprise (3) in which the investors expect to make a profit, and (4) the profits will be derived from the efforts of someone other than the investor.

If the SEC, Congress, or the courts declare that cryptocurrencies meet the Howey Test and are therefore securities, Solomon’s got you covered with the Series 7 General Securities Representative Exam Guide. This FINRA license allows you to engage in “the solicitation, purchase and/or sale of all securities products.”

If cryptocurrencies don’t meet the Howey Test, they could be regulated as commodities. These are goods such as wheat, gold, and pork bellies. Why might cryptocurrencies fit in with these others? Because commodities are all highly standardized so that they can be freely bought and sold on exchanges without worrying about differences in quality—every ounce of gold is pretty much like every other ounce of gold. Likewise, every Bitcoin is like every other Bitcoin.

For many when choosing bonds the most important factor is the tax implications. Knowing the after-tax yield and tax-equivalent yield calculations is critical. Continue reading

Bonds can be nice, reliable investments. Pay some money to an issuing company or municipality, receive interest payments twice a year, and then get all of your original investment back sometime down the road. Sounds like a plan.

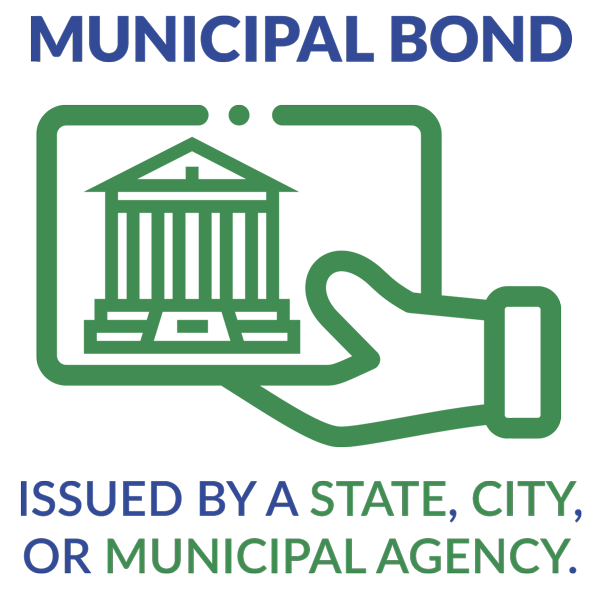

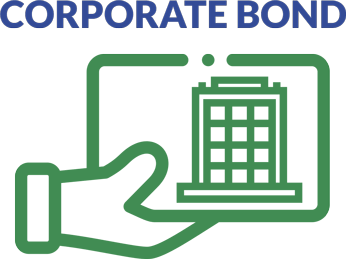

But which bonds are best for a specific investor? There are many factors for bond investors to consider when choosing which bond to buy, but for many the most important is the tax implications of investing in one bond instead of another. This concern is most prominent when an investor compares a corporate bond to a municipal bond. For reference, a corporate bond is one issued by a corporation or business, while a municipal bond is one issued by a state, city, or municipal agency.

Comparing the tax implications of these bonds is important because the interest payments that investors receive from municipal bonds are typically not taxed at the federal level. Conversely, interest payments on all corporate bonds are subject to federal taxation. This means that someone in the 32% tax bracket will have to give Uncle Sam 32% of his interest received from a corporate bond, while he will not give up any of his interest received from a municipal bond. Additionally, an investor does not pay state taxes on municipal bond interest if the bond is issued in the state in which the investor lives. Corporate bond interest, on the other hand, is always subject to state tax.

interest payments taxed federally

interest payments subject to state tax

interest payments not federally taxed

interest payments not taxed by state if issued in state local to investor

For these reasons, when comparing a corporate bond to a municipal bond, understanding the after-tax yield and the tax-equivalent or corporate-equivalent yield is essential. This is true both for investors and for those who will be taking many of the FINRA, NASAA, and MSRB exams. So let’s look at how to calculate those yields.

After-Tax Yield

First the after-tax yield. The after-tax yield tells you the amount of a corporate bond’s annual interest payment that an investor will take home after accounting for taxes he will be assessed on that interest. Once that amount is known, the investor can compare it to the yield he would receive from a specific municipal bond and see which potential investment would put more money in his pocket. When calculating the after-tax yield, start with the annual interest percentage (a.k.a. coupon percentage) of the corporate bond, which represents the percent of the bond’s par value that an investor receives each year in interest. For instance, a corporate bond that has a $1,000 par value and an interest rate of 8% will pay an investor $80 dollars in annual interest ($1,000 x 0.08 = $80). You then multiply the coupon percentage by 1 minus the taxes an investor will pay on the corporate bond that he will not pay on the municipal bond that he is considering.

This is where it sometimes gets tricky. What taxes will an investor not pay when investing in a municipal bond that he will pay when investing in a corporate bond? Remember that for just about all municipal bonds, investors do not pay federal tax on interest received.

The formula for after tax yield is:

After-tax yield = Corporate Bond Annual Interest Rate x ( 1 – Taxes Investor Does Not Pay By Investing in Municipal Bond)

On the other hand, an investor always pays federal taxes on interest received from a corporate bond. Additionally, an investor does not pay state taxes on interest payments from a municipal bond issued in the state in which the investor lives.

On the other hand, an investor always pays state taxes on interest received from corporate bonds. So if you see an exam question in which you need to calculate the after-tax yield of a corporate bond to compare it the yield on a municipal bond, you will always subtract the investor’s federal income tax rate from 1 in the equation. You will also subtract the investor’s state tax rate from 1 if the municipal bond is issued in the investor’s state of residence.

Seems simple, right? Here’s a question to provide context:

Marilyn is a resident of Kentucky. She is considering a bond issued by XYZ Corporation. The bond comes with a 7% annual interest rate. Marilyn is also interested in purchasing municipal bonds issued in Ohio. If Marilyn has a federal tax rate of 28% and Kentucky’s state tax rate is 4%, what is the after-tax yield on XYZ’s bond?

To answer this question, begin with the interest rate on the XYZ bond, which is 7%. Then subtract from 1 the taxes Marilyn will not pay if she invests in the municipal bond in question. She will not pay federal taxes on the municipal bond interest, so you would subtract 28%, or .28. However, because Marilyn is a resident of Kentucky and the municipal bonds she is considering are issued in Ohio, she will pay state taxes on the bond. That means you would not subtract her state tax rate (0.04) from 1. After subtracting .28 from 1 to get 0.72, you multiply that amount by the 7% coupon payment. Doing so gives you a value of 5.04 (7 x 0.72 = 5.04%). This means that the interest amount she would take home from the XYZ bond would be equivalent to what she would receive from a municipal bond issued in Ohio that has a 5.04% interest payment. If she can get a bond issued in Ohio that has a higher interest payment than 5.04%, she would take home more money in annual interest payments than she would from the XYZ bond.

Tax-Equivalent Yield

The second approach an investor can take to compare how a potential bond investment will be affected by taxation is to calculate the tax-equivalent yield (TEY). This calculation is also known as the corporate-equivalent yield (CEY). The TEY/CEY measures the yield that a corporate bond will have to pay to be equivalent to a given municipal bond after accounting for taxes due. To calculate this yield, you take the annual interest of the given municipal bond and divide it by 1 minus the taxes the investor will not pay if she invests in the municipal bond that she would pay if she invested in a corporate bond.

Here’s the formula for tax-equivalent yield:

Tax-equivalent yield = Municipal Bond Annual Interest Rate / (1 – Taxes Investor Does Not Pay By Investing in Municipal Bond)

When determining what tax rates to subtract from 1 in the denominator, the same principal as described above applies. That is, the investor will not have to pay federal tax on the municipal bond, so her federal rate is always subtracted from 1. The investor will also not have to pay state tax on the bond if it is issued in the state in which she lives. If that is the case, the investor’s state tax rate should also be subtracted from 1. However, if the investor lives in a different state than the state in which the bond is issued, she will have to pay state taxes on the interest payments. In that case, her state tax rate would not be subtracted from 1.

Here’s another question to provide context.

Franz, a resident of Michigan, has purchased a Michigan municipal bond that pays 4% annual interest. If his federal tax bracket is 30% and the Michigan state tax rate is 4%, what interest rate would he need to receive on a corporate bond to have a comparable rate after accounting for taxes owed?

To answer this question, begin with the interest rate on the Michigan municipal bond, which is 4%. Then subtract from 1 the taxes that Franz will not pay on that bond that he would pay if he invested in a corporate bond. He wouldn’t pay federal taxes on the municipal bond interest, so you would subtract 0.30 from 1. Additionally, since the bond is issued in Michigan and he is a Michigan resident, Franz will not pay state taxes on the bond. So you subtract Michigan’s state tax rate of 4%, or 0.04, from 1 as well. After subtracting 0.30 and 0.04 from 1 to get 0.66, you divide that number into the 4% municipal bond annual interest. Doing so gives a value of 6.06 (4 / 0.66 = 6.06). This means Franz would need to find a corporate bond that pays 6.06% in annual interest to match the amount of interest he will take home annually from the Michigan municipal bond after accounting for taxes.

Many people are confused by the concepts of the after-tax and tax-equivalent yields. But you don’t have to be one of them. Just follow this simple approach and any questions you see on this topic will not be overly taxing.

SPACs have grown by leaps and bounds in recent years. What will this mean for regulations, and will this topic appear on the FINRA Series 79 exam? Continue reading

Updated August 24, 2022

What is a SPAC?

It sounds like a securities-industry riddle: what do you call a blank check company with no hard assets that holds a multimillion dollar IPO? But the answer is very real: SPACs (special purposes acquisition companies) are an alternative to traditional IPOs that have exploded in popularity.

What’s a “blank check company”? A blank check company is an exchange-listed shell company that, according to the SEC, has “no specific business plan or…its business plan is to engage in a merger or acquisition.”

The purpose of a SPAC is to raise money to acquire a privately held company. Think of it as crowdfunding on a massive scale. First, the SPAC sells shares of itself in an IPO. Then it uses the IPO proceeds to fund a merger between itself and a target company. When the merger is complete, the SPAC’s shareholders become shareholders in the target company. Investors buy SPAC shares based on their confidence that the SPAC’s management will complete the merger and the anticipated value of the shares after the merger.

SPACs have grown by leaps and bounds in recent years. The amount raised by SPAC IPOs in 2020 more than quadrupled the amount they raised in 2019, and the number of SPACs more than doubled from 2020 to 2021. Though SPACs have struggled in 2022, they remain an important new development in the world of securities offerings.

What does this mean for regulations?

As investor excitement around SPACs has heated up, there are indications that the SEC is beginning to take a closer look at this new kind of IPO. On March 10, 2021, the SEC issued a warning against investing based on celebrity involvement with a SPAC. Celebrities with high-profile ties to SPACs include A-Rod, Shaquille O’Neal, Serena Williams, and former Speaker of the House Paul Ryan. Acting SEC Chair Allison Herren Lee recently warned of “more and more evidence on the risk side of the equation for SPACs as we see studies showing that their performance for most investors doesn’t match the hype.”

Will SPACs be tested on the Series 79 exam?

While none of this guarantees that new rules for SPACs are around the corner, it does make it more likely that FINRA’s Series 79 Investment Banking Exam may begin to include mention of SPACs. They are a topic that investment bankers are increasingly likely to encounter in practice, and therefore are increasingly likely to be viewed as fair game for the exam.

Solomon Exam Prep is ahead of the curve with new material in our Series 79 Study Guide. Series 79 customers can find material on SPACs included in both the online and hard copy editions of the Solomon Series 79 Study Guide.

Potentially testable points about SPACs include:

SPACs are formed by “sponsors,” commonly institutional investors or high net worth individuals, who are compensated with both a portion of the IPO proceeds, as well as an equity stake in the SPAC of up to 20%.

SPACs typically avoid committing to merge with a specific company, even if the SPAC was formed with the intention of targeting that company. The SPAC’s management may respond to changing market conditions by choosing a different target, subject to approval from the SPAC’s shareholders.

After a SPAC goes public, its shares trade freely on exchanges even before it completes a merger.

A SPAC must hold at least 85% of proceeds from its IPO in an escrow account.

The SPAC commits to return investor funds if it fails to complete a merger within a specified timeframe.

As a blank check company with no business operations of its own, a SPAC cannot take advantage of certain options available to more established securities issuers. For example, a SPAC is not permitted to make an electronic version of its road show presentation.

For a sample of Series 79 practice questions, try out Solomon’s free Series 79 Sample Quiz.

Solomon Exam Prep will continue to follow industry trends and how they affect your licensing exams. To stay informed, join the Solomon email list! Just click the button below to subscribe:

On Wednesday, the SEC finalized rule changes that will broaden its definition of “accredited investor” to encompass industry professionals who have earned certain FINRA licenses. Continue reading

On Wednesday, the SEC finalized rule changes that will broaden its definition of “accredited investor” to encompass industry professionals who have earned certain FINRA licenses.

An accredited investor is an investor considered sophisticated enough to weigh an investment’s merits independently. Accredited investors have easier access to certain types of investments, such as private equity offerings.

Under the newly expanded definition, General Securities Representatives (Series 7), Private Securities Offerings Representatives (Series 82), and Licensed Investment Adviser Representatives (Series 65) are now accredited investors. The SEC indicated that it may add other FINRA licenses later. Note that passing the exam by itself does not make you an accredited investor – you must have and maintain the license.

The rule change also allows “spousal equivalents” such as domestic partners to qualify as accredited investors based on the total income and assets of both partners, a benefit previously limited to couples who are legally married. Native American tribes and foreign governments now qualify as accredited investors as well.

The Solomon Exam Prep team is always on the lookout for how current developments affect the securities industry. For more updates from our Industry News blog, use the subscribe form on this page.

With post-Brexit vote market turmoil, it’s good to remember that the Securities Exchange Commission requires trading halts across US markets in the event that stocks fall more than specified percentages in one day. Continue reading

With post-Brexit vote market turmoil, it’s good to remember that the Securities Exchange Commission requires trading halts across US markets in the event that stocks fall more than specified percentages in one day. This information is also important to know if you are studying for securities licensing exam such as the Series 7, Series 24, Series 26, Series 62, Series 79, and the Series 65.

A market-wide trading halt can be triggered at three thresholds. These thresholds are triggered by steep declines in the S&P 500 Index. They are calculated based on the prior day’s closing price of the Index.

• Level 1 Halt—a 7% drop in the S&P 500 prior to 3:25 p.m. ET will result in a 15-minute cross-market trading halt. There will be no halt if the drop occurs at or after 3:25 p.m. ET.

• Level 2 Halt—a 13% drop in the S&P 500 prior to 3:25 p.m. ET will result in a 15-minute cross-market trading halt. There will be no halt if the drop occurs at or after 3:25 p.m. ET.

• Level 3 Halt—a 20% drop in the S&P 500 at any time during the day will result in a cross-market trading halt for the remainder of the day.

These halts apply to securities and options trading on all the exchanges as well as the OTC market. Levels 1 and 2 trading halts are permitted just once a day.

Solomon Exam Prep has helped thousands of financial professionals pass the Series 6, 7, 63, 65, 66, 24, 26, 27, 50, 51, 52, 53, 62, 79, 82 and 99 exams.

For more information call 503 601 0212 or visit http://www.solomonexamprep.com/

The Securities and Exchange Commission announced last week that next April it plans to introduce a fiduciary standard for broker-dealers. Since last month when the Department of Labor issued its fiduciary rule for tax-advantaged retirement accounts, the securities industry has been waiting to see if the SEC would join the Department of Labor in a push to raise the legal and ethical standards for broker-dealers and agents. Continue reading

The Securities and Exchange Commission announced last week that next April it plans to introduce a fiduciary standard for broker-dealers. Since last month when the Department of Labor issued its fiduciary rule for tax-advantaged retirement accounts, the securities industry has been waiting to see if the SEC would join the Department of Labor in a push to raise the legal and ethical standards for broker-dealers and agents.

Currently, broker-dealers and agents are held to the less stringent suitability ethical standard while investment advisors and investment advisor representatives are held to the higher fiduciary standard. The higher standard requires disclosure of all conflicts of interest and ensures the client’s interests come first. While SEC Chair Mary Jo White has said she supports a uniform fiduciary rule, Republicans in Congress have strongly opposed the effort by the Labor Department to expand the fiduciary standard to retirement accounts. However, many in the securities industry hope that the SEC’s efforts will harmonize with the Department of Labor’s efforts, making compliance more uniform and less complicated.

Capital markets in the United States are arguably the strongest in the world. Recent developments could strengthen them even more by making equity investing and equity capital-raising much more accessible. Continue reading

Capital markets in the United States are arguably the strongest in the world. Recent developments could strengthen them even more by making equity investing and equity capital-raising much more accessible.

In an effort to lower the cost and increase the availability of equity investing to small businesses, the SEC just adopted Regulation Crowdfunding (Title III of the Jobs Act adding Securities Act Section 4(a)(6)). These are the much-awaited final rules permitting equity crowdfunding, which allows small and startup companies to raise capital via the internet through relatively small contributions from investors.

Under the terms of the new rules, crowdfunding transactions for eligible U.S. companies will be exempted from SEC registration, provided

the aggregate amount the issuer sells to all investors in a 12-month period does not exceed $1 million,

The aggregate amount sold to any investor does not exceed a given percentage of that investor’s annual income or net worth (the greater of 2% or $5,000 for investors with either an annual income or net worth of less than $100,000; 10%, but not to exceed $100,000, for all others),

The transaction is conducted through either a registered broker-dealer or a registered “funding portal”, and

Issuers are in compliance with required SEC disclosure filings.

Certain companies are not eligible for the crowdfunding exception. These include all foreign-based companies, Exchange Act-reporting companies, certain investment companies, and companies that have previously failed to comply with crowdfunding reporting requirements.

Buyers of crowdfunding securities will be required to hold them for at least a year before they can resell them.

This alert applies to the Series 7, Series 24, Series 62, Series 79, and Series 82.

Effective June 19, 2015 the SEC changed the Regulation A registration exemption for small issues. The change moved from the old standard of $5 million or smaller issues to a new standard of $50 million or smaller issues. In addition, there are two “tiers” for Reg A – offerings up to $20 million are Tier 1, and offerings up to $50 million are Tier 2. Continue reading

Effective June 19, 2015 the SEC changed the Regulation A registration exemption for small issues. The change moved from the old standard of $5 million or smaller issues to a new standard of $50 million or smaller issues. In addition, there are two “tiers” for Reg A – offerings up to $20 million are Tier 1, and offerings up to $50 million are Tier 2.

Tier 2 issuers are required to include audited financial statements in their offering documents and to file annual, semiannual, and current reports with the SEC. Also, if a Tier 2 issue is not listed on a national securities exchange, purchasers in Tier 2 offerings must either be accredited investors or be subject to certain limitations on their investment. Specifically, non-accredited investors cannot spend over 10% of the greater their annual income or net worth for a natural person, or over 10% of the greater of their revenue or net assets for a non-natural person.

On June 1, 2015, the SEC issued an investor bulletin about “diminished financial capacity”, which refers to when an individual becomes unable to manage their finances. They recommend a number of steps for individuals to take to prepare for such a condition. Continue reading

On June 1, 2015, the SEC issued an investor bulletin about “diminished financial capacity”, which refers to when an individual becomes unable to manage their finances. They recommend a number of steps for individuals to take to prepare for such a condition. These steps include:

Organize important documents and keep them safe and accessible

Give your financial professionals emergency contacts

On March 25, the Securities and Exchange Commission proposed rule amendments to require that broker-dealers trading in off-exchange venues become members of a national securities association. Continue reading

On March 25, the Securities and Exchange Commission proposed rule amendments to require that broker-dealers trading in off-exchange venues become members of a national securities association. According to SEC Chair Mary Jo White, “today’s proposed rules would close a regulatory gap by extending oversight to a significant portion of off-exchange trading.”

The proposed amendments to Rule 15b9-1 under the Exchange Act would eliminate the proprietary trading exemption and replace it with a narrower one that will permit a floor-based dealer to engage in off-exchange transactions only if such transactions hedge the broker-dealer’s floor-based trading. The proprietary trading exemption originally was designed to accommodate exchange specialists and other floor members that might need to conduct limited hedging or other off-exchange activities ancillary to their floor-based business. Over time, the markets have undergone a substantial transformation, including the emergence of active cross-market proprietary trading firms, many of which engage in so-called high-frequency trading strategies. Although the business of these firms may not be focused on an exchange floor, and they may be responsible for a substantial percentage of the trading volume in the off-exchange market, many are not members of a national securities association because they have been able to rely on the broad proprietary trading exemption in Rule 15b9-1.

The proposed amendments would amend the exemption to target the broker-dealers for which it was originally designed – those with a business focused on an exchange floor and over which that exchange is positioned to oversee the entirety of their trading activity. They also would update the exemption that permits off-exchange transactions necessary to comply with regulatory requirements restricting trade-throughs, under Rule 611 of Regulation NMS.

The SEC will take public comment on the proposed rule amendment for 60 days following publication in the Federal Register.

With post-Brexit vote market turmoil, it’s good to remember that the Securities Exchange Commission requires trading halts across US markets in the event that stocks fall more than specified percentages in one day. This information is also important to know if you are studying for securities licensing exam such as the Series 7, Series 24, Series 26, Series 62, Series 79, and the Series 65.

With post-Brexit vote market turmoil, it’s good to remember that the Securities Exchange Commission requires trading halts across US markets in the event that stocks fall more than specified percentages in one day. This information is also important to know if you are studying for securities licensing exam such as the Series 7, Series 24, Series 26, Series 62, Series 79, and the Series 65. The Securities and Exchange Commission announced last week that next April it plans to introduce a fiduciary standard for broker-dealers. Since last month when the Department of Labor issued its fiduciary rule for tax-advantaged retirement accounts, the securities industry has been waiting to see if the SEC would join the Department of Labor in a push to raise the legal and ethical standards for broker-dealers and agents.

The Securities and Exchange Commission announced last week that next April it plans to introduce a fiduciary standard for broker-dealers. Since last month when the Department of Labor issued its fiduciary rule for tax-advantaged retirement accounts, the securities industry has been waiting to see if the SEC would join the Department of Labor in a push to raise the legal and ethical standards for broker-dealers and agents. Capital markets in the United States are arguably the strongest in the world. Recent developments could strengthen them even more by making equity investing and equity capital-raising much more accessible.

Capital markets in the United States are arguably the strongest in the world. Recent developments could strengthen them even more by making equity investing and equity capital-raising much more accessible.