Want to become an Investment Banker? Solomon Series 79 Study Guide, 6th Edition, Now Available

The updated 6th edition of the Solomon Series 79 Study Guide covers everything you need to know to pass the FINRA Series 79 exam. Continue reading

The updated 6th edition of the Solomon Series 79 Study Guide covers everything you need to know to pass the FINRA Series 79 exam. Continue reading

What can you do with a Series 79 license? What is the exam like and how should you prepare for it? Solomon answers your top Series 79 questions. Continue reading

For a number of securities exams, you should understand the term “tender.” Solomon explains what the term means and how it’s used in the securities industry. Continue reading

What does it take to pass securities licensing exams like the SIE, Series 24, Series 63, and Series 79? Read about one student’s approach to success. Continue reading

Preparing for the SIE, Series 63, Series 79, Series 82, or another securities licensing exam? Read about one Solomon Exam Prep student’s path to success. Continue reading

Solomon Exam Prep explains what a Series 7 General Securities Representative can and cannot do and how this compares to other rep-level registrations. Continue reading

If you’re studying for securities licensing exams, such as the SIE or the Series 7, then you should understand the terms “accredited investor” and “QIB.” Continue reading

If you’ve been studying for the Series 7, 6, 14, 22, 24, 65, 79, or 82, or the Securities Industry Essentials (SIE), then you’ve had to learn about Regulation D private placements and Rule 144A sales. Regulation D private placements are securities offerings that are exempt from the normal SEC registration process and in many cases are sold only to “accredited investors” or limit the involvement of investors who are not accredited. Rule 144A sales are sales of unregistered securities to large institutional investors known as “qualified institutional buyers” or QIBs for short.

You may have wondered about the difference between accredited investors and QIBs. On the surface, these may seem similar. Each refers to a category of investor with resources and/or knowledge above and beyond the average retail investor. So why not just have one standard for buyers under both Rule 144A and Regulation D? After all, the purpose of both Regulation D and Rule 144A is the same: to allow wealthier and more sophisticated investors easier access to investments that may be too risky for the average investor.

To begin to answer this question, we have to start with the fact that wealth and sophistication fall on a spectrum. Investors aren’t neatly divided between small retail investors and huge financial institutions that move millions around without blinking an eye.

You could think of accredited investors as a middle ground between these two extremes. Accredited investors are investors whose financial status or investment knowledge may give them a greater ability to handle the risks inherent in a private placement. There are many ways to qualify as an accredited investor but they all have one thing in common, which is that the SEC believes they indicate an ability to take on risks that regulators believe are unsuitable for most retail investors.

Accredited investors are investors whose financial status or investment knowledge may give them a greater ability to handle the risks inherent in a private placement.

An accredited investor that is not an individual—such as a business, governmental, or nonprofit entity—is sometimes called an institutional accredited investor (IAI).

QIBs are a narrower group of large institutional investors. A QIB is a large institutional investor that owns at least $100 million worth of securities, not counting securities issued by its affiliates. For registered broker-dealers, the threshold is lower, just $10 million. A bank must also have a net worth of at least $25 million in order to be considered a QIB.

If a firm has discretionary authority to invest securities owned by a QIB, those securities count toward whether the firm itself is considered a QIB. So if a broker-dealer has $9 million worth of securities in its own accounts, and holds $1 million worth of securities in a discretionary account belonging to a QIB, then the broker-dealer is itself a QIB.

Common examples of QIBs include broker-dealers, insurance companies, investment companies, pension plans, and banks. However, any corporation, partnership, or LLC could qualify as a QIB. So can an IAI that owns at least $100 million in securities. Individuals can never be QIBs, regardless of their assets or financial sophistication.

Individuals can never be QIBs, regardless of their assets or financial sophistication.

Rule 144A allows QIBs to buy unregistered securities at any time, and freely trade these shares to other QIBs. In effect, QIBs can trade unregistered shares among themselves with almost the same ease as trading registered shares. Selling unregistered securities to anyone other than a QIB commonly requires a the seller to hold the securities for a period of up to 12 months.

A QIB will virtually always meet the criteria to be an accredited investor, whereas an accredited investor may fall well short of QIB status.

Over time, other securities laws and regulations have made use of these two well-known categories. For example, in 2019 the SEC gave issuers more flexibility to test the waters with potential investors before deciding whether to go through with a public offering. When deciding which investors were sophisticated enough to receive test-the-waters communications, the SEC limited these communications to QIBs and institutional accredited investors. Additionally, references to institutional accredited investors have become more common, such as when the SEC revamped its rules around integration of offerings in March 2021.

Know your QIBs from your accredited investors and be ready to pass your securities exam with Solomon Exam Prep.

For more helpful securities exam-related content, study tips, and industry updates, join the Solomon email list. Just click the button below:

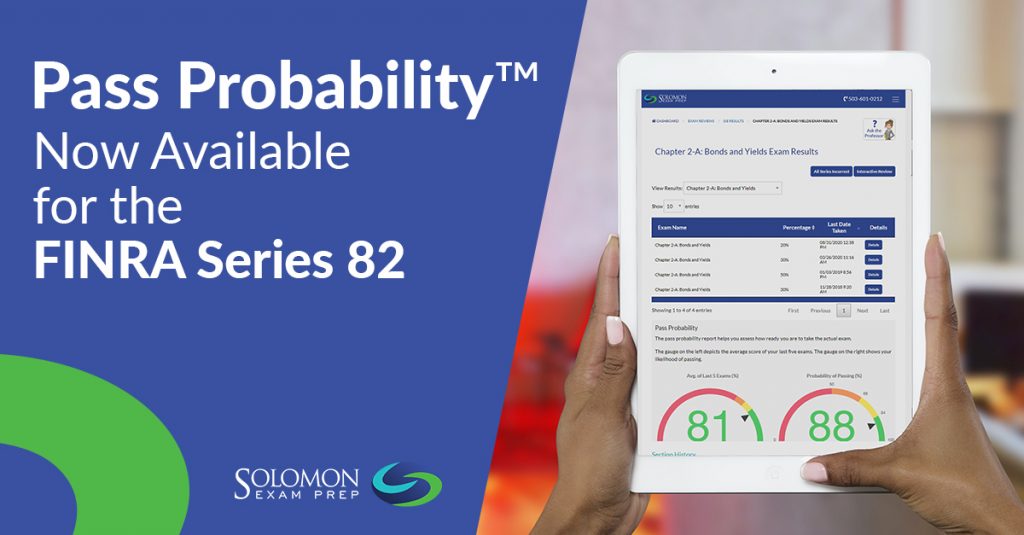

Everyone would like to feel confident when they take their securities exam, but how do you know if you’re ready for test day? Solomon Exam Prep can help – with Pass Probability™. Continue reading

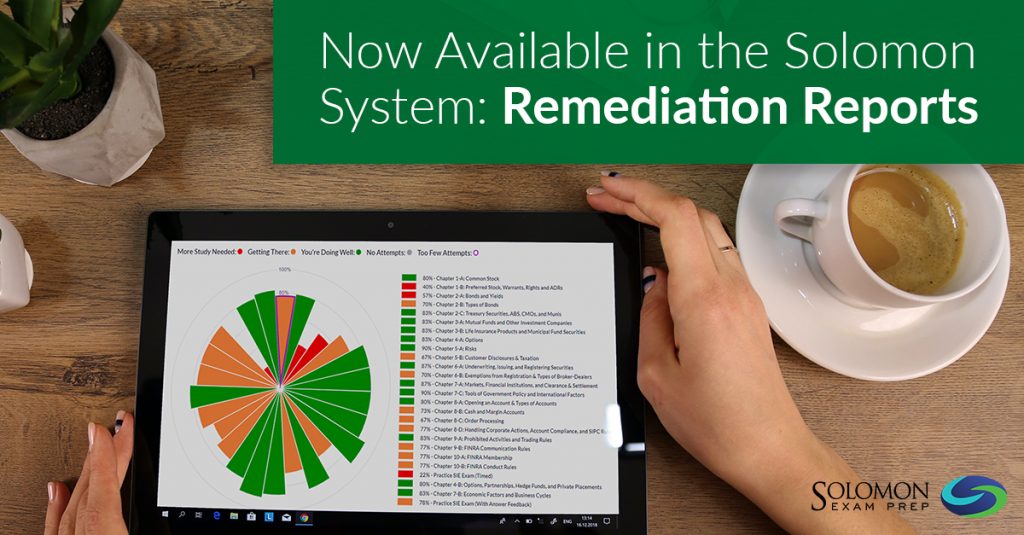

Learn about the Solomon Remediation Report, a new analytical feature designed to help students pass their securities licensing exams the first time. Continue reading

Solomon Exam Prep is delighted to announce an advanced analytical feature called a Remediation Report. The Solomon system analyzes a student’s five most recent practice exams and determines whether a student is ready to take his or her exam. If Solomon AI determines that a student is not ready to sit for their exam, then it creates an individual report with personalized guidance on how to remediate and prepare to pass. This custom Remediation Report is sent to the Solomon student’s email inbox.

The Solomon Remediation Report is connected to the Solomon Pass Probability tool, the industry-leading measure of a security exam prep student’s readiness to pass an exam. Solomon Pass Probability is based on thousands of student data points. Once a Solomon student has taken at least five practice exams, the Solomon Pass Probability feature is activated, and the Pass Probability metric is available in the student’s dashboard. The Solomon Remediation Report provides an additional level of customized study support by helping students focus their efforts and remediate before they sit for their exam.

Solomon Pass Probability and Remediation Reports are currently available for the following exams: SIE, Series 6, Series 7, Series 63, Series 65, Series 66, Series 79, and Series 82.

To learn about all the features of the Solomon Exam Prep learning system, watch the video overview.

SPACs have grown by leaps and bounds in recent years. What will this mean for regulations, and will this topic appear on the FINRA Series 79 exam? Continue reading

Updated August 24, 2022

It sounds like a securities-industry riddle: what do you call a blank check company with no hard assets that holds a multimillion dollar IPO? But the answer is very real: SPACs (special purposes acquisition companies) are an alternative to traditional IPOs that have exploded in popularity.

What’s a “blank check company”? A blank check company is an exchange-listed shell company that, according to the SEC, has “no specific business plan or…its business plan is to engage in a merger or acquisition.”

The purpose of a SPAC is to raise money to acquire a privately held company. Think of it as crowdfunding on a massive scale. First, the SPAC sells shares of itself in an IPO. Then it uses the IPO proceeds to fund a merger between itself and a target company. When the merger is complete, the SPAC’s shareholders become shareholders in the target company. Investors buy SPAC shares based on their confidence that the SPAC’s management will complete the merger and the anticipated value of the shares after the merger.

SPACs have grown by leaps and bounds in recent years. The amount raised by SPAC IPOs in 2020 more than quadrupled the amount they raised in 2019, and the number of SPACs more than doubled from 2020 to 2021. Though SPACs have struggled in 2022, they remain an important new development in the world of securities offerings.

As investor excitement around SPACs has heated up, there are indications that the SEC is beginning to take a closer look at this new kind of IPO. On March 10, 2021, the SEC issued a warning against investing based on celebrity involvement with a SPAC. Celebrities with high-profile ties to SPACs include A-Rod, Shaquille O’Neal, Serena Williams, and former Speaker of the House Paul Ryan. Acting SEC Chair Allison Herren Lee recently warned of “more and more evidence on the risk side of the equation for SPACs as we see studies showing that their performance for most investors doesn’t match the hype.”

While none of this guarantees that new rules for SPACs are around the corner, it does make it more likely that FINRA’s Series 79 Investment Banking Exam may begin to include mention of SPACs. They are a topic that investment bankers are increasingly likely to encounter in practice, and therefore are increasingly likely to be viewed as fair game for the exam.

Solomon Exam Prep is ahead of the curve with new material in our Series 79 Study Guide. Series 79 customers can find material on SPACs included in both the online and hard copy editions of the Solomon Series 79 Study Guide.

For a sample of Series 79 practice questions, try out Solomon’s free Series 79 Sample Quiz.