How to Pass the FINRA Series 24 Exam

Should you take the Series 24 exam? Keep reading to learn what the Series 24 qualifies you to do, what the exam covers, and how you should prepare for it. Continue reading

Should you take the Series 24 exam? Keep reading to learn what the Series 24 qualifies you to do, what the exam covers, and how you should prepare for it. Continue reading

Passing a securities exam like the SIE exam is an important step in your career. But what if you don’t pass the first time? Here are tips for restudying. Continue reading

Considering taking the Series 51 exam? Keep reading to learn what the Series 51 qualifies you to do, what the exam covers, and how you should prepare for it. Continue reading

Thinking about taking the Series 22 exam? Keep reading to learn what the Series 22 qualifies you to do, what the exam covers, and how you should prepare for it. Continue reading

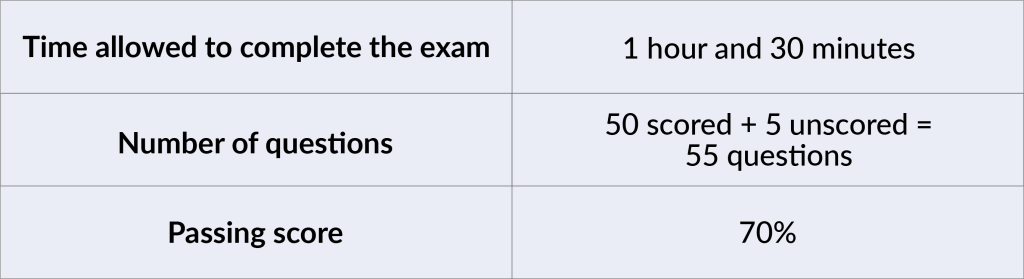

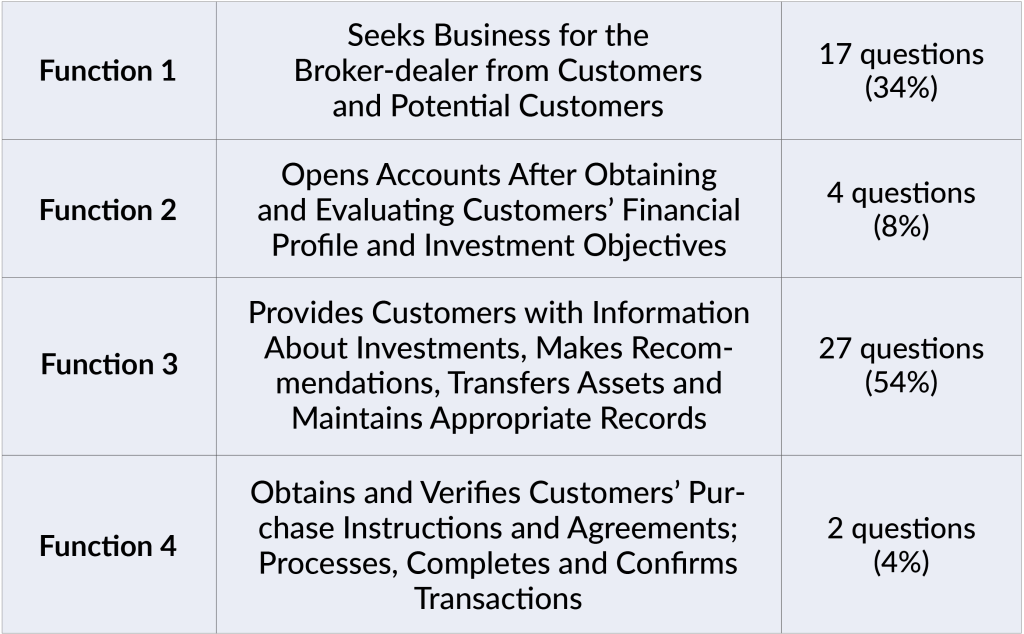

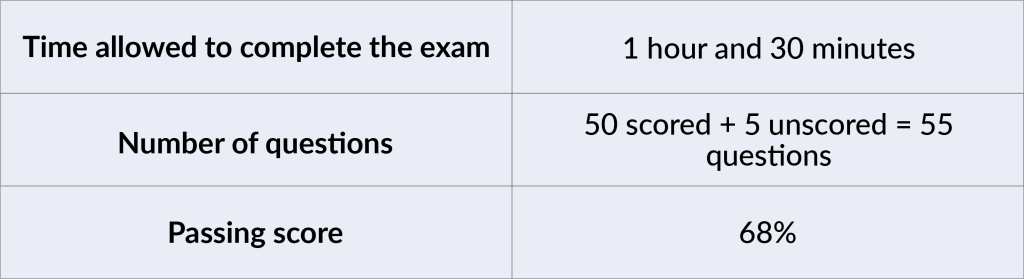

Thinking about taking the Series 99 exam? Keep reading to learn what the Series 99 qualifies you to do, what the exam covers, and how you should prepare for it. Continue reading

Thinking about taking the Series 54 exam? Keep reading to learn what the Series 54 qualifies you to do, what the exam covers, and how you should prepare for it. Continue reading

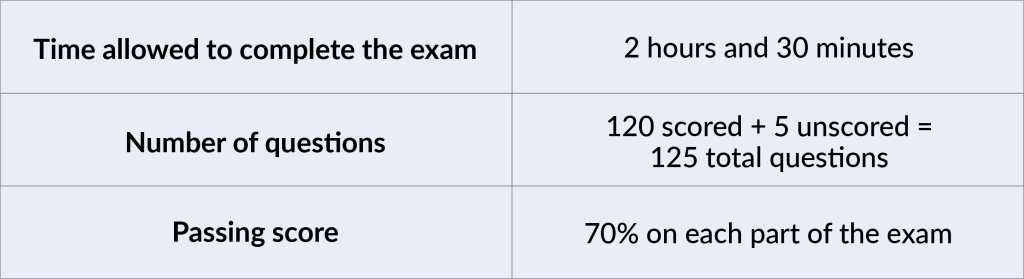

What is the Series 3 exam? Learn what passing the Series 3 exam allows you to do, what the exam covers, and how you should prepare for it. Continue reading

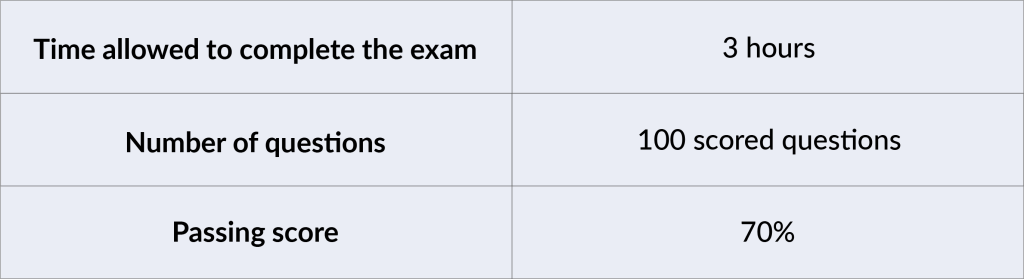

What is the Series 53 exam? Learn what a Series 53 license qualifies you to do, what the exam covers, and how you should prepare for it. Continue reading

What is the Series 52 exam? Learn what a Series 52 license qualifies you to do, what the exam covers, and how you should prepare for it. Continue reading

Thinking about taking the Series 63 exam? Keep reading to learn what the Series 63 qualifies you to do, what the exam covers, and how you should prepare for it. Continue reading