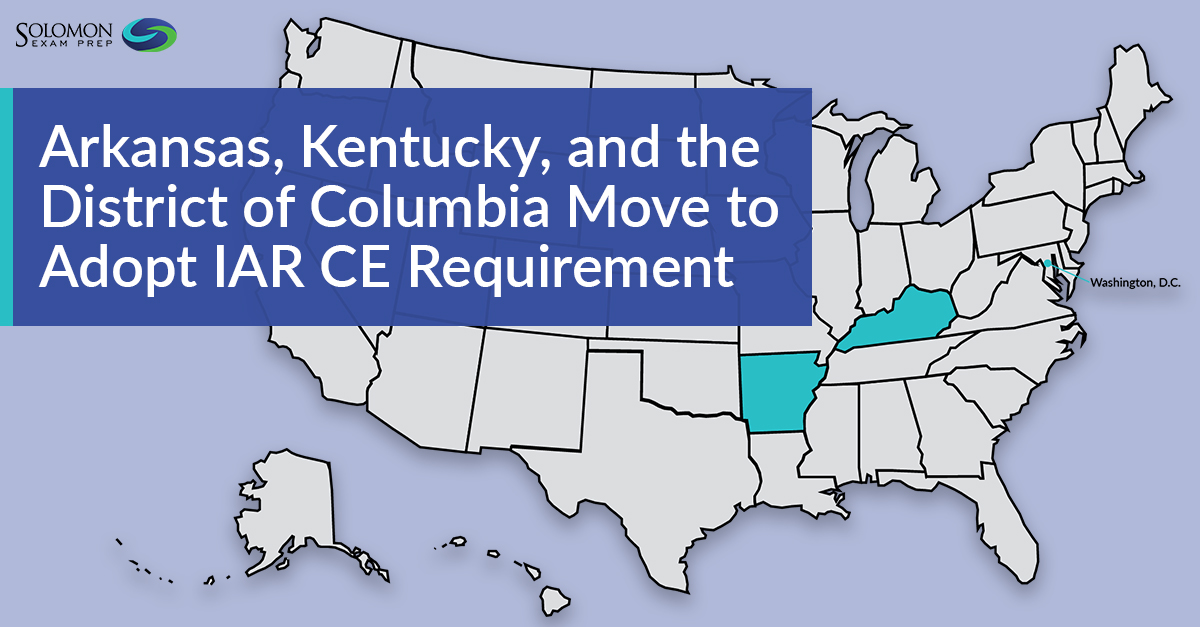

Arkansas Adopts Continuing Education Requirement for Investment Adviser Representatives

Investment Adviser Representatives registered in Arkansas must complete NASAA-approved continuing education courses beginning in 2023. Continue reading

Investment Adviser Representatives registered in Arkansas must complete NASAA-approved continuing education courses beginning in 2023. Continue reading

Solomon has added another Ethics and Professional Responsibility course for Investment Adviser Representatives to complete their annual IAR CE requirement. Continue reading

Investment Adviser Representatives registered in Washington DC must complete NASAA-approved continuing education courses beginning in 2023. Continue reading

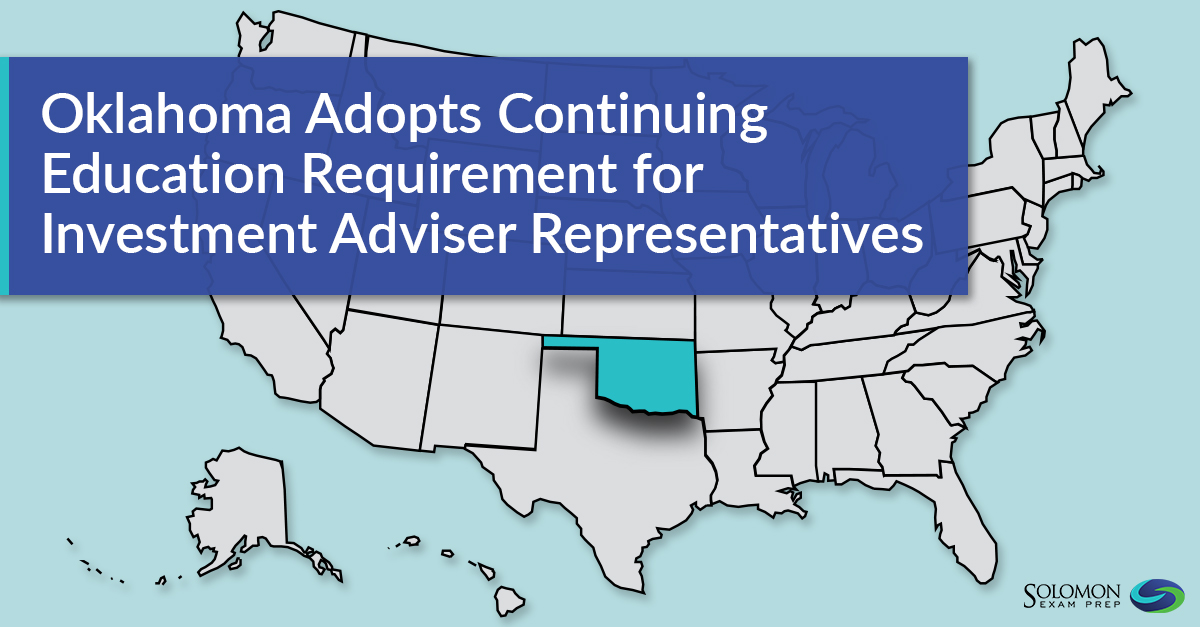

Investment Adviser Representatives registered in Oklahoma must complete NASAA-approved continuing education courses beginning in 2023. Continue reading

Investment Adviser Representatives have two more Solomon continuing education courses to choose from to complete their annual NASAA IAR CE requirement. Continue reading

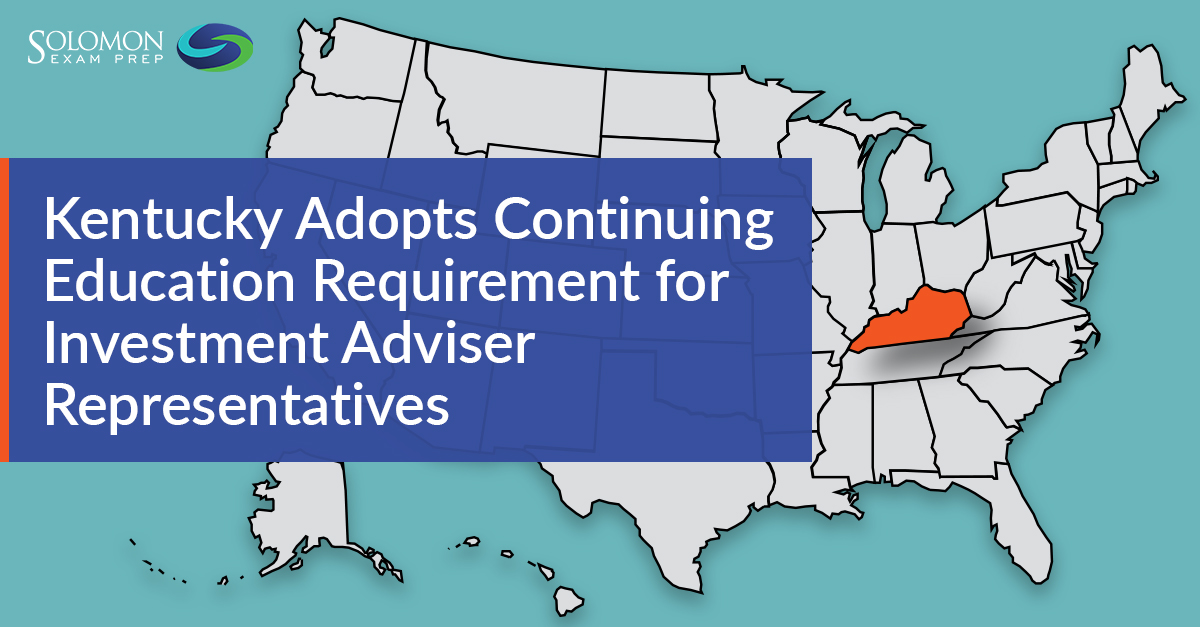

Investment Adviser Representatives registered in Kentucky must complete NASAA-approved continuing education courses beginning in 2023. Continue reading

If you plan to take the NASAA Series 63, Series 65, or Series 66 exams, the new editions of these Solomon Study Guides are now available. Continue reading

If you’re planning to take the Series 63, Series 65, or Series 66 exam after March 31, 2022, testing online will not be available for most candidates. Continue reading

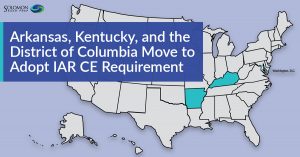

Arkansas, Kentucky, and Washington, D.C. have begun the process to adopt NASAA Investment Adviser Representative continuing education. Continue reading

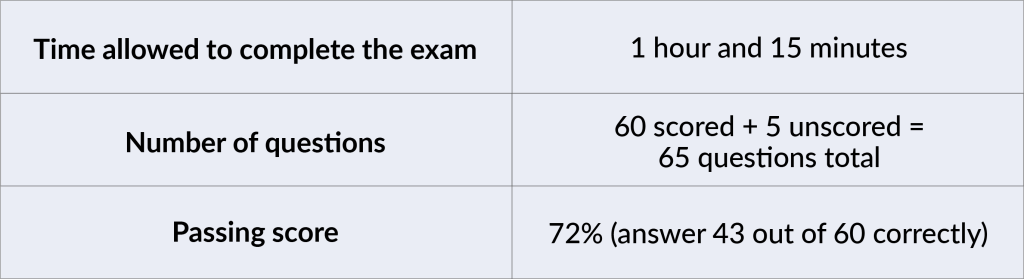

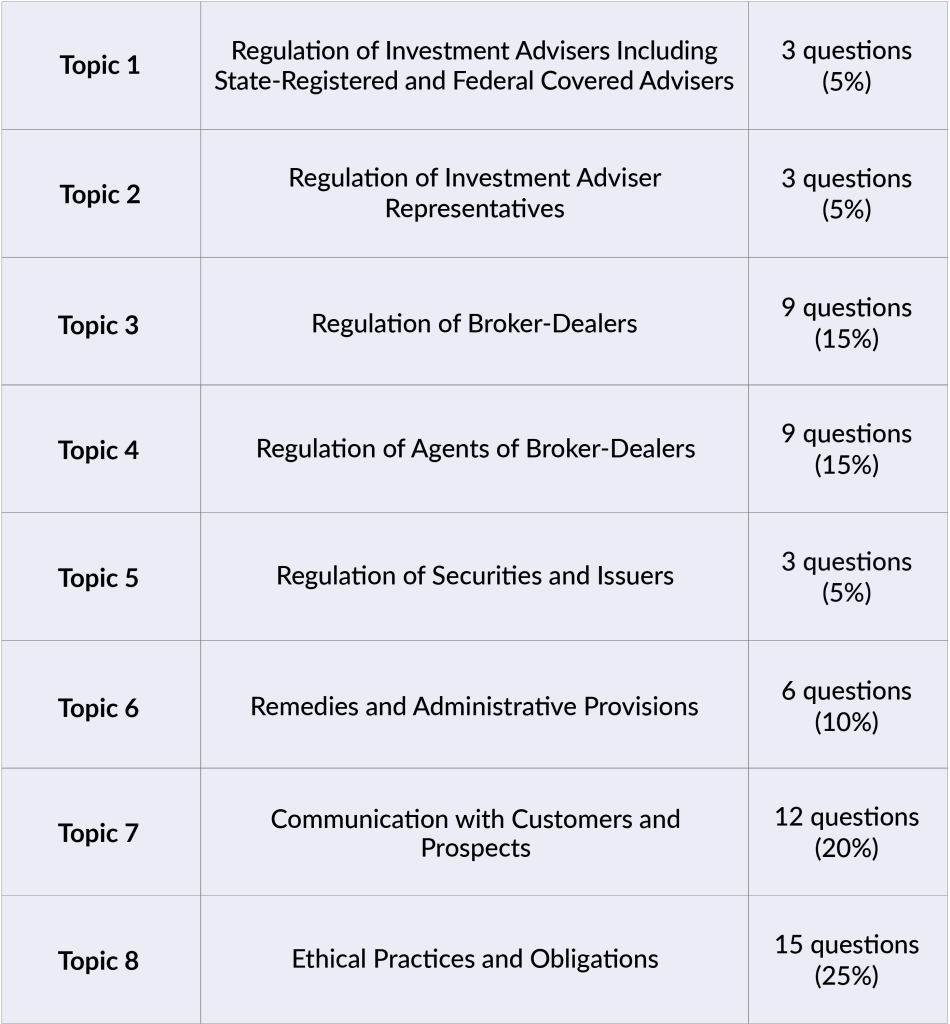

Thinking about taking the Series 63 exam? Keep reading to learn what the Series 63 qualifies you to do, what the exam covers, and how you should prepare for it. Continue reading