In addition to offering an SIE exam prep course, State College of Florida has added courses for five more securities exams using Solomon Exam Prep study programs. Continue reading

Solomon Exam Prep and the State College of Florida (SCF) have expanded their partnership to offer exam prep courses for a total of six securities exams. Solomon study programs are being used in courses for the FINRA SIE, Series 6, and Series 7 exams, as well as the NASAA Series 63, 65, and 66 exams.

About the Courses

Offered through SCF Workforce Development, the courses are 100% online and self-paced, so students can easily fit study time into their individual schedules. Anyone 18 years or older can register for the courses. Each course includes 180-day access to the Solomon Total Study Package, which consists of these Solomon digital materials:

Study Guide

Exam Simulator

Audiobook

Video Lecture

Flashcards

In addition to these study materials, all courses provide free Solomon tools and resources to give students the best chance at passing their exams. These include Solomon Study Schedules in digital and pdf formats, individual instructor support via Ask the Professor, and Solomon Pass Probability™, an innovative feature that predicts a student’s readiness to take the exam.

About the Exams

Passing the Securities Industry Essentials (SIE) Exam is the foundational requirement for many careers in the securities industry. The SIE covers basic or “essential” securities industry knowledge. In addition to passing the SIE, individuals must also pass specialized representative-level exams (such as the Series 6 and Series 7) to be permitted to work in specific job roles. These exams “top-off” your knowledge of the industry with more in-depth information. Most people take the SIE first and then take one or more representative-level exams.

Partner with Solomon Exam Prep

Solomon Exam Prep partners with dozens of colleges and universities to bring securities exam prep to students across the country. The Solomon learning system works equally well for in-person, hybrid, and online courses.

Join institutions such as State College of Florida, Elon University, Florida Memorial University, Pepperdine University, the University of North Carolina at Pembroke, Claflin University, University of Delaware, Adelphi University, University of Nebraska-Omaha, Seton Hall University, Ohio Dominican University, Georgetown University, Widener University, and University of Dallas in partnering with Solomon.

To learn more about the ways colleges and universities can partner with Solomon, contact Beth Hamilton, Higher Education Sales Manager, at beth@solomonexamprep.com or 503-601-0212.

If you plan to take the FINRA Series 7 exam, the new edition of the Solomon Series 7 Study Guide covers everything you need to know to pass the exam. Continue reading

There are many exciting careers in the securities industry, such as stockbroker, investment adviser representative, financial advisor, and investment banker. Perhaps less exciting are the securities licensing exams you’re required to pass to pursue these careers. For example, if you’re interested in a career buying and selling all securities products, then you’ll need to pass the FINRA General Securities Representative Exam, also known as the Series 7 (plus the co-requisite Securities Industry Essentials, or SIE, exam).

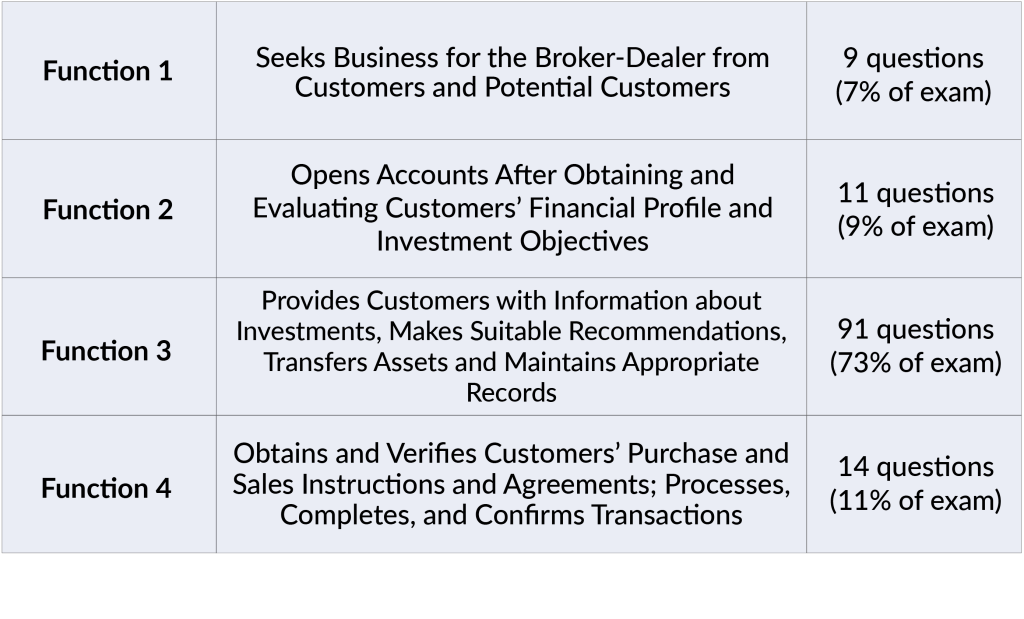

The Series 7 is one of the longest FINRA exams. It is a 135-question test that covers the four main functions of a securities representative. You have three hours and 45 minutes to complete the exam. Like all qualifying exams in the securities industry, the Series 7 is closed-book. As one of the most challenging FINRA exams, it’s a good idea to be well-prepared going into test day. How should you prepare for the Series 7 exam?

Solomon Exam Prep has just released its 4th edition of The Solomon Exam Prep Guide to the Series 7 General Securities Representative Examination. To help professionals pass the exam, the Solomon Series 7 Study Guide is comprehensive and covers exam topics in easy-to-understand language. Charts, graphs, and practice questions throughout the text support learners in understanding and applying key concepts.

“The Series 7 is challenging. To pass this exam, you must learn the concepts, not just memorize test questions. The Solomon system focuses on teaching the core concepts in a digestible way and reinforcing them through examples and quizzes. This prepares customers not only for the exam, but also for their careers.”

Jeremy Solomon

Solomon Exam Prep President and Co-founder

What changes with this new edition?

While the core content remains the same, the 4th edition of the Series 7 Study Guide includes helpful content updates, along with general writing improvements.

Updates are also reflected in the Solomon Series 7 Exam Simulator. Designed to accompany the Study Guide, the online Exam Simulator contains over 4,400 original Series 7 practice questions with rationales that explain why an answer is correct. With the Solomon Series 7 Exam Simulator, learners can take an unlimited number of quizzes and exams, and the simulator comes with helpful self-assessment tools and Solomon’s proprietary Pass Probability™ technology, which calculates the probability that the student will pass the Series 7 exam.

Solomon Exam Prep is committed to providing industry-leading securities licensing materials, which are continuously kept up-to date. If you are an existing Solomon Series 7 customer, the new 4th edition will be automatically updated in your account, free of charge.

To learn more about Solomon Exam Prep’s Series 7 study materials, including Study Guide, Exam Simulator, Audiobook, Video Lecture, Flashcards, and Live Web Classes, visit the Solomon Series 7 product page.

Be prepared for questions about SIMPLE, SEP, and solo 401(k) retirement account plans on the FINRA Series 6 and Series 7 exams. Continue reading

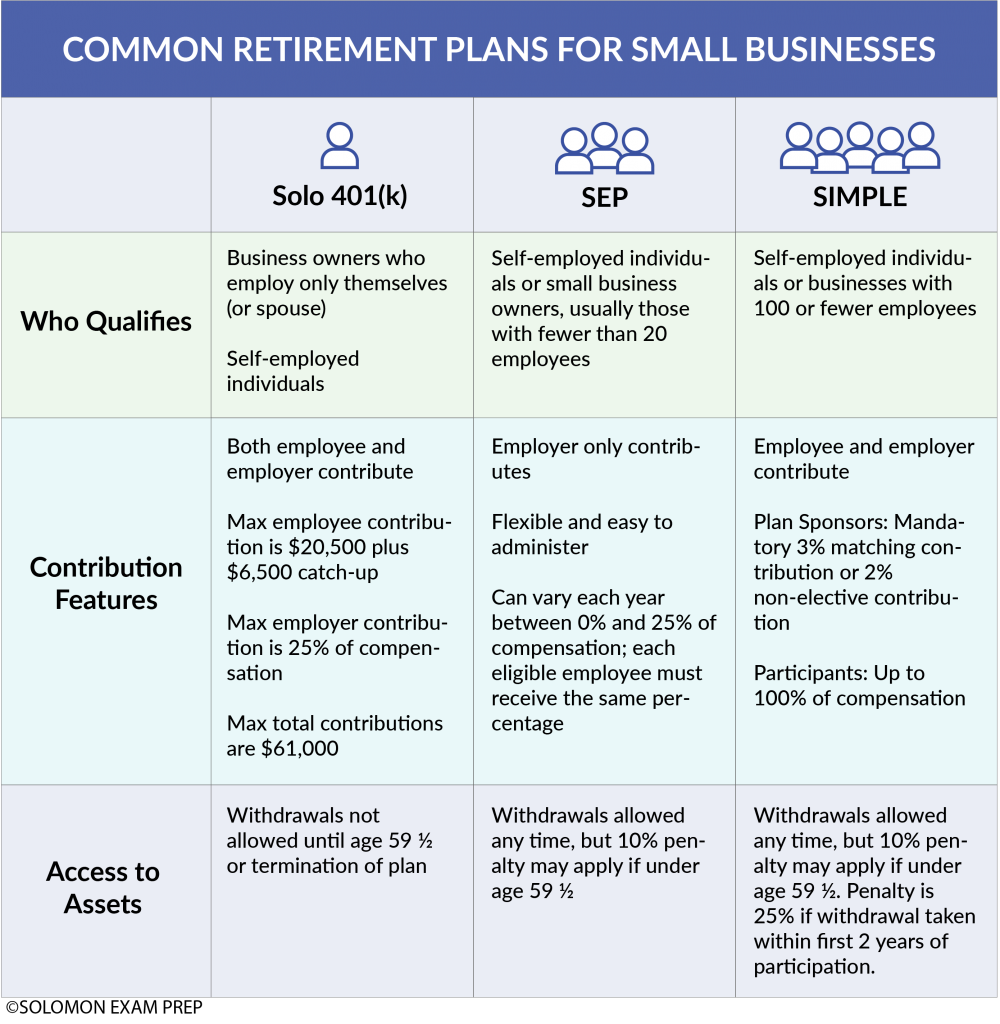

If you are studying for the FINRASeries 6 or Series 7 exam, you will need to learn about the different types of retirement plan accounts. A retirement account may be an individual plan that is managed by the participant or the participant’s agent, such as an investment firm or a trust bank. Or it may be employer-sponsored, meaning that it is organized and managed by the participant’s employer. Private employers of any size and structure, from the largest C corporation to a sole proprietorship consisting of a single self-employed individual, may set up and use an employer-sponsored retirement plan. For small business owners, retirement plans offer significant tax advantages and can help attract employees. Since there are several types of retirement plans available for small businesses, it’s important to understand the features of each option. Three plans commonly chosen by small businesses are solo 401(k) plans, SEP plans, and SIMPLE plans.

Solo 401(k) Plans

A business owner can open a solo 401(k) if the business does not employ anyone else. The owner of the business creates a 401(k) plan much like any other employer. Then, as an employee, the owner opens a 401(k) account within that plan. Both employer and employee contributions can be made in a solo 401(k). The maximum employee contribution is the same as for other 401(k)s. As of 2022, this limit is $20,500 per year, with a catch-up contribution of $6,500 for those aged 50 and above. As an employer, the maximum annual contribution is 25% of what the owner pays herself. The combined annual contribution (employee and employer) cannot exceed $61,000. The business owner is allowed to employ her spouse and still make use of a solo 401(k) plan. The spouse can open their own 401(k) account using the business’s solo 401(k) plan. A solo 401(k) can be created whether the business is set up as a corporation, LLC, or sole proprietorship. Self-employed people who haven’t set up a business can also create a solo 401(k), although their contribution limits are calculated differently. Unlike most employer-sponsored retirement plans, solo 401(k)s do not need to comply with ERISA (the Employee Retirement Income Security Act). This is a federal law that requires employers to give employees fair access to the employer’s retirement plan. These concerns do not apply when the business has no other employees.

SEP

Simplified Employee Pension (SEP) plans are IRA-based retirement plans for any size business but are usually favored by small businesses. Under this type of plan, the business owner can make pre-tax contributions into IRA accounts set up for eligible employees and also for herself if the owner is self-employed.

The plan allows employers to skip contributions in years when business is bad, but if the owner makes a contribution for herself, she must also make contributions for her employees. When contributions are made, they must be made for all participants who actually performed work during the year for which the contributions are made, including those over 72 years of age (the latter feature is unique to the SEP plan). Contributions for all participants generally must be uniform, for example the same percentage of hourly wage. The business owner can make contributions of up to 25% of an employee’s salary, or an annual maximum of $61,000, whichever is less. Only the employer, and not the employee, makes contributions to the SEP IRA, but an employee is always 100% vested in his SEP IRA. Generally, the employer can take an income tax deduction for contributions made to each employee’s SEP. SEP contributions are not included on the employee’s W-2 statement for tax purposes. Rules for withdrawal of funds are generally the same as for any other IRA, meaning that withdrawals are subject to income taxes, and early withdrawals are usually subject to a penalty.

SIMPLE

Savings Incentive Match Plan for Employees (SIMPLE) plans are retirement plans for businesses having no more than 100 employees. With a SIMPLE IRA or SIMPLE 401(k), the employee may make pre-tax contributions to the plan. The contribution is expressed as a percentage of the employee’s compensation and is limited to $14,000 a year ($17,000 for employees aged 50 and over). The employer is required to either match these contributions up to 1% to 3% of the employee’s compensation or to contribute 2% whether the employee makes a contribution or not. The employer chooses which type of contribution (and if matching, the maximum percentage it will match). This choice applies to all employees. So an employer who chooses matching contributions is not obligated to contribute 2% to an employee who chooses not to contribute. Any employee who previously earned at least $5,000 during any two years and is reasonably expected to receive at least $5,000 during the current calendar year is eligible to participate in this plan. Unlike the SEP plan, however, premature SIMPLE IRA distributions (withdrawals of account funds) will incur a 25% penalty in the first two years the account exists if made before age 59 1/2. While the SEP plan is discretionary, in that the employer can decide when to fund the plan, funding the SIMPLE IRA plan is mandatory, no matter what kind of year the business had. A SIMPLE 401(k) functions similarly to a SIMPLE IRA. Both have the same contribution limits and are 100% vested from the beginning.

Good to know:

SEP and SIMPLE IRAs have characteristics in common with traditional IRAs. For example, contributions are generally made with pre-tax dollars, must be earned income, and must only be in cash. Taxes on contributions and earnings are deferred until withdrawal, as long as withdrawals occur after the age of 59 1/2. Required minimum distributions (RMDs) must begin the year the participant turns age 72, although the participant may choose to delay the first payment until April 1 of the following year. After that, RMDs must be taken by December 31 each year. Funds can be distributed as a lump sum or in periodic payments. If the account owner fails to withdraw an RMD or the full amount of the RMD before the deadline, the amount not withdrawn is taxed at 50%.

Anyone who plans to become a registered representative by passing the Series 6 or Series 7 exam and assist customers with retirement plans must understand the complexity of retirement planning. The Solomon Exam Prep Series 6 Study Guide and Series 7 Study Guide both cover retirement plan accounts so that you can be prepared for questions about this topic on exam day. Visit the Solomon website to explore study materials for 21 different securities exams, including the Series 6 and 7.

What can you do with a Series 7 license? What is the exam like and how should you prepare for it? Solomon answers your top Series 7 questions. Continue reading

What does the Series 7 exam permit me to do?

The Series 7, also known as the General Securities Representative Qualification Exam, was developed by the Financial Industry Regulatory Authority (FINRA) to assess the skills and competency of entry-level registered representatives as general securities representatives. Passing the Series 7 exam qualifies you to solicit, purchase, and/or sell all securities products, including corporate securities, municipal fund securities, options, direct participation programs, investment company products, and variable contracts. As a result of this broad scope, the Series 7 exam is one of the longest and most challenging securities industry exams. The good news, however, is that you will be permitted to perform an impressive range of activities with a Series 7 license. The following are covered activities and products:

Public offerings and/or private placements of corporate securities (stocks and bonds)

Rights

Warrants

Mutual funds

Money market funds

Unit investment trusts (UITs)

Exchange-traded funds (ETFs)

Real estate investment trusts (REITs)

Options on mortgage-backed securities

Government securities

Repos and certificates of accrual on government securities

Direct participation programs (DPPs)

Venture capital

Sale of municipal securities

Hedge funds

Do I need to take any other securities licensing exams?

In order to be registered as a general securities representative, you must pass two exams: the Series 7 and the FINRA Securities Industry Essentials (SIE) exam. While the Series 7 requires you to be hired and sponsored by a FINRA-member firm, the SIE does not. Therefore, even though you can technically take them in either order, it makes sense to take the introductory-level SIE exam before taking the Series 7 exam.

About the Exam

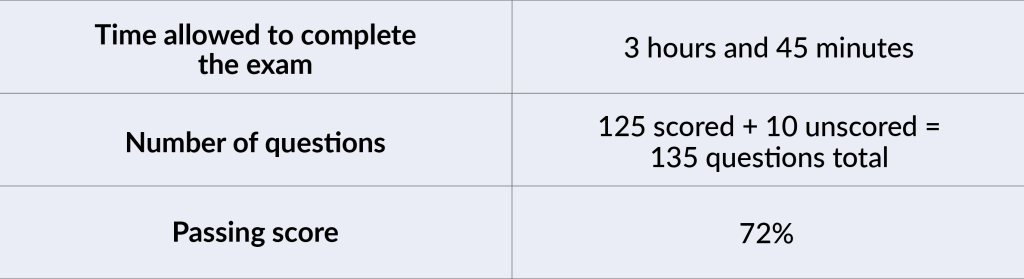

The Series 7 exam consists of 125 scored and 10 un-scored multiple-choice questions covering the four sections of the FINRA Series 7 content outline. The 10 additional un-scored questions are ones that the exam committee is trying out. These are unidentified and are distributed randomly throughout the exam.

Note: Scores are rounded down to the next lowest whole number (e.g. 71.9% would be a final score of 71% – not a passing score for the Series 7 exam).

Topics Covered on the Exam

The questions on the Series 7 exam cover the main job functions of a general securities representative, as determined by FINRA:

FINRA updates its exam questions regularly to reflect the most current rules and regulations. Solomon recommends that you print out the current version of the FINRA Series 7 Content Outline and use it in conjunction with the Solomon Series 7 Study Guide. The Content Outline is subject to change without notice, so make sure you have the most recent version.

Question Types on the Exam

The Series 7 exam consists of multiple-choice questions, each with four options. You will see these question structures:

Closed Stem Format:

This item type asks a question and gives four possible answers from which to choose.

When interest rates go up, what will happen to the price of typical preferred stock?

It will go up.

It will go down.

It will stay the same.

It is unrelated to interest rates, so it is impossible to tell.

Incomplete Sentence Format:

This kind of question has an incomplete sentence followed by four options that present possible conclusions.

The owner of a house with a market value of $450,000 and an assessed value of $300,000, and with an ad valorem tax of 4 mills would pay a property tax of:

$1,800

$1,200

$12,000

$18,000

“EXCEPT” Format:

This type requires you to recognize the one choice that is an exception among the four answer choices presented.

VRDOs may have their rates automatically reset at any of the following frequencies except:

Daily

Weekly

Monthly

Yearly

Complex Multiple-Choice (“Roman Numeral”) Format:

For this question type, you see a question followed by two or more statements identified by Roman numerals. The four answer choices represent combinations of these statements. You must select the combination that best answers the question.

A Build America Bond may:

Provide a 35% subsidy on the interest as a tax deduction

Reimburse the issuer for 35% of the interest paid to investors

Provide a 35% subsidy on the interest as a tax credit

Provide a 35% subsidy on the interest as an additional interest payment

I or II

I or IV

II and III

III and IV

This format is also used in items that ask you to rank or order a set of items from highest to lowest (or vice versa), or to place a series of events in the proper sequence.

The flow of funds requirement for a municipality with a net revenue pledge usually prioritizes the following funds in which order, going from highest priority to lowest priority?

Debt service fund

Debt service reserve fund

Operations and maintenance fund

I, II, III

III, I, II

II, I, III

III, II, I

Answers: B, B, D, C, B

For an even better idea of the possible question types you might encounter on the Series 7 exam, try Solomon Exam Prep’s free Series 7 Sample Quiz.

Taking the Series 7 Exam

The Series 7 exam can be taken at a Prometric test center or remotely online using Prometric’s ProProctor system. If taking the exam at a test center, you will be given a dry erase pen and whiteboard or a pen and scratch paper, and a basic electronic calculator. You cannot bring notes, paper, or your own calculator. Phones and watches are not permitted either. Due to COVID-19, you are required to wear a mask the whole time you are at the test center. Solomon recommends taking timed practice exams in the Series 7 Exam Simulator while wearing a mask to get used to this added discomfort.

If you’re thinking about taking the test from the comfort of your own home or office with ProProctor, it’s important to be aware of the strict procedures you must follow. See this user guide for complete details. And for a first-hand account of the remote testing experience, read this Solomon blog post.

Test-Taking Tips

Whether you take the exam in person or online, it helps to keep some test-taking strategies in mind. You have an average of slightly more than a minute and a half per question, so don’t spend too long on one question—this may cause you to run out of time and not get to other questions you know. If you don’t know the answer to a question, guess at the answer and “flag” it. You will not be penalized for guessing.

After you have finished all the questions, you can come back to any flagged questions. Not only does this strategy allow you to efficiently answer the ones you know, but it can also help because you might learn something later in the exam that may help you answer an earlier question. Just remember to save enough time to return to the questions you didn’t answer. However, it is not a good idea to simply skip all of the difficult questions with the intention of answering them later. You should make a serious effort to answer each question before moving on to the next one, as your thoughts are often clearer early on in the exam-taking process than they will be later.

How to Study for the Series 7 Exam

Follow Solomon Exam Prep’s proven study system:

Read and understand. Read the Solomon Study Guide, carefully. The Series 7 is a knowledge test, not an IQ test. Many students read the Study Guide two or three times before taking the exam. To increase your ability to focus while reading, or as an alternative to reading, listen to the Solomon Series 7 Audiobook, which is a word-for-word reading of the Study Guide.

Answer practice questions in the Solomon Exam Simulator. When you’re done with a chapter in the Study Guide, take 4–6 chapter quizzes in the Solomon Series 7 Online Exam Simulator. Use these quizzes to give yourself practice and to find out what you need to study more. Make sure you read and understand the question rationales. When you’re finished reading the entire Study Guide, review your handwritten notes once more. Then, and only then, start taking full practice exams in the Exam Simulator. Aim to pass at least six full practice exams and try to get your Solomon Pass Probability™ score to at least an 80%; when you reach that point, you are probably ready to sit for the Series 7 exam.

Use these effective study strategies:

Take handwritten notes. As you read the Study Guide, take handwritten notes and review your notes every day for 10 to 15 minutes. Studies show that the act of taking handwritten notes in your own words and then reviewing them strengthens learning and memory.

Make flashcards. Making your own flashcards is another powerful and proven method to reinforce memory and strengthen learning. Solomon also offers digital flashcards for the Series 7 exam.

Research. Research anything you do not understand. Curiosity = learning. Students who take responsibility for their own learning by researching anything they do not understand get a deeper understanding of the subject matter and are much more likely to pass.

Become the teacher. Studies show that explaining what you are learning greatly increases your understanding of the material. Ask someone in your life to listen and ask questions. If you don’t have anyone, explain it to yourself. Studies show that helps almost as much as explaining to an actual person (see Solomon’s previous blog post to learn more about this strategy!).

Take advantage of Solomon’s supplemental tools and resources:

Use all the resources. The Series 7 Resources folder in your Solomon student account has helpful study tools, including several documents that summarize important exam concepts. There are also detailed study schedules that you can print out – or use the online study schedule and check off tasks as you complete them.

Watch the Video Lecture. This provides a helpful review of the key concepts in each chapter after reading the Solomon Study Guide. Take notes to help yourself stay focused.

Good practices while studying:

Take regular breaks. Studies show that if you are studying for an exam, taking regular walks in a park or natural setting significantly improves scores. Walks in urban areas or among people did not improve test scores.

Get enough sleep during the period when you are studying. Sleep consolidates learning into memory, studies show. Be good to yourself while you are studying for the Series 7: exercise, eat well, and avoid activities that will hurt your ability to get a good night’s sleep.

You can pass the FINRA Series 7 Exam! It just takes focus and determination. Solomon Exam Prep is here to support you on your path to becoming a general securities representative.

To explore all Solomon Exam Prep’s Series 7 study materials, including product samples, visit the Solomon website here.

For more helpful securities exam-related content, study tips, industry updates, and promotional offers, join the Solomon email list. Just click the button below:

Do you need to pass the SIE, Series 7, Series 66, or another FINRA or NASAA exam? Hear one student’s experience preparing for and taking her securities exams. Continue reading

There are many career options to choose from in the financial services industry, such as stockbroker, investment banker, financial analyst, or financial advisor. Whether you’re aiming for a job on Wall Street or off, you will probably need to pass a securities licensing exam or two (or three) to be permitted to work in your chosen role. To reach her career goals, Solomon customer Pennie Kincade, Financial Advisor at Raymond James Financial Services, decided to take the FINRA Securities Industry Essentials (SIE) and Series 7, and the NASAASeries 66 exams. Pennie recently shared her experience studying for and passing her exams.

“From passing the exams, I have been able to further my career and truly enjoy coming to work every day. It’s been a privilege to partner with my clients and plan for their retirement.”

Pennie Kincade

Solomon Exam Prep: What led you to take the SIE, Series 7, and Series 66?

Pennie Kincade: When I started working in the financial services industry, I found my passion helping individuals and businesses reach their financial goals. I wanted to take this a step further by helping with their long-term goals, wealth management strategies, business succession planning, and retirement planning. With the SIE, Series 7 and 66, now I can follow my dream of assisting clients with wealth management strategies.

Solomon Exam Prep: Out of the exams you passed, which one did you find the most challenging and why?

Pennie Kincade: The Series 7 was the most challenging and the longest exam. It was helpful to have Solomon Exam Prep available to answer my questions and breakdown concepts into simple terms. They gave me confidence to push through and not give up.

Solomon Exam Prep: How did you approach studying for your exams?

Pennie Kincade: When studying for each exam, it was important to read each chapter and take a chapter exam at the end. Regardless of my scores, I continued reading through, taking an exam and then I started taking half exams once or twice a week. The questions I missed, I wrote down and referred back to for review. I reread my notes and reviewed each chapter on sections I scored low in. Once my scores were in the 80s, I moved onto a full exam once a week. Making note cards and writing out the questions I missed were helpful to review later. Two weeks before the exam, I made a sheet with notes to review each day with definitions, formulas or calculations.

Solomon Exam Prep: How did you take the exams – at a testing center or remotely? How was your experience, and do you have any tips to share?

Pennie Kincade: I completed my exams at the testing center. Before each exam, I would arrive an hour and a half early. During this time, I would have a small snack and drink some water. Then I reviewed my note cards and one page cram sheet. When I was able to write down notes during the exam, I wrote down everything I could remember from my cram sheet since it was fresh in my mind. I found this helpful to refer back to when I was getting a little anxious. It helped me stay focused and maintain confidence.

“It was helpful to have Solomon Exam Prep available to answer my questions and breakdown concepts into simple terms. They gave me confidence to push through and not give up.”

Solomon Exam Prep: Any words of wisdom to help motivate others who are preparing for exams?

Pennie Kincade: Give yourself enough time to study and know when you need a break. I read my notes out loud, while recording my voice and listened to them on the way to work. The chapters I had a difficult time remembering I would read the section before bed and touch on it the next morning. If I felt I had information overload, I would get up for a snack and take a 15-minute break.

Solomon Exam Prep: How has passing these exams affected your work and your career?

Pennie Kincade: From passing the exams, I have been able to further my career and truly enjoy coming to work every day. It’s been a privilege to partner with my clients and plan for their retirement.

Visit the Solomon Exam Prep website to explore study materials for 21 different securities licensing exams, including the SIE, Series 7, andSeries 66.

For a number of securities exams, you should understand the term “tender.” Solomon explains what the term means and how it’s used in the securities industry. Continue reading

When studying for a securities exam such as the FINRA Securities Industry Essentials (SIE) exam and the Series 7, Series 14, Series 24, Series 79, or the MSRBSeries 50, Series 52, Series 53, or Series 54, it’s likely you will encounter the word “tender.” This bit of terminology may be confusing at first. But learning the ways “tender” is commonly used in the securities industry will prevent you from getting tripped up when you see it on an exam.

You may have heard this word in connection with stock buybacks. When a company offers to buy its shares back from stockholders, the company is said to be conducting a tender offer. The stockholders who take the company up on the offer are said to be tendering their shares. A company may also make a tender offer to a different company’s shareholders, for example if it wants to acquire the other company. The word “tender” comes from the field of law. To tender is to make a binding offer to enter into an agreement. (It also has a second meaning of presenting payment, which is why your dollar bill has the phrase “legal tender” on it.) So when you tender a security you own, you are offering to sell it on terms that have been spelled out between you and the other party. In the case of a tender offer, the company must specify these terms when it makes the offer and shareholders must take them or leave them. In many cases, the U.S. Securities and Exchange Commission (SEC) requires that these terms include a window of time during which shareholders who tendered their shares may change their minds. In that case, the “binding offer” is not binding right away. Another securities-related use of “tender” is when a security gives its owner the right to sell it back to the issuer. Exercising this right is sometimes called tendering the security. For example, a municipal bond might have a tender option that gives the bondholder the right to sell it back to the municipality at a certain time for a certain price. Additionally, some variable-rate municipal securities come with a mandatory tender that is triggered when the rate is adjusted. When this happens, the bondholder must choose between tendering the bond or accepting the new rate. So if you see the word “tender” on a securities exam, it means that the owner of a security is offering to sell it under specific terms and conditions, and the owner’s ability to back out of the offer may be limited.

Want a curated collection of our most relevant blog posts delivered straight to your email inbox each month? Subscribe to the Solomon Monthly Newsletter and get securities exam study tips, industry news, and more! Just click the button below to join.

What are inflation and inflation expectations, and why are they important? Learn what these terms mean and the results of the latest Solomon poll. Continue reading

Can you predict what the economic future of the U.S. will be next month? How about next year? If you’re not sure, Solomon Exam Prep suggests you look at leading indicators, which are economic measures that have been found to anticipate a change in the economy. They are also tested subjects on securities licensing exams such as the FINRA Securities Industry Essentials (SIE) exam and the NASAA Investment Adviser (Series 65) exam. One important leading indicator is inflation. So, we asked Solomon LinkedIn followers to predict whether the rate of inflation in 2022 will increase, decrease, or stay the same. According to the poll, a whopping 81% of respondents believe that inflation will increase in 2022. Ten percent predict that inflation will stay the same, and nine percent think it will decrease. For securities licensing exams, leading indicators are important to understand because they are believed to have predictive power, and therefore, allow economists to see what the economic future may hold. That is why Solomon Exam Prep study guides for the Securities Industry Essentials (SIE), Series 7, Series 65, and Series 66 all discuss inflation. So, what exactly is inflation and why does it occur?

What is inflation and why does it happen?

Inflation means an increase in the prices of goods and services and a decline in the purchasing power of a currency. It can be understood as a part of business cycles, which are fluctuations in the economy. A business cycle has four phases. The first phase, expansion, is characterized by an increase in economic activity and above-average economic growth. In this phase, the production of goods rises and unemployment falls. Lenders make credit more available because they believe businesses and people will be able to repay their loans. Available credit means lower interest rates, which fuels expansion, resulting in more jobs. The expansion phase feels good because jobs are plentiful, and wages rise. But a risk of the expansion phase is the possibility of inflation because increasing wages and available credit tend to boost prices. Inflation can result when demand for goods and services outstrips their supply. This usually occurs near the end of an expansionary phase, when too much money is chasing too few goods. Inflation can occur because of:

High consumer confidence in the economy

An economy that has reached its production potential

Excess money in the economy

Increases in wages and other production costs, such as a rise in commodity prices

What does inflation mean for investors?

With rising prices come rising interest rates. For example, if the cost of living is increasing at 5%, as measured by the Consumer Price Index (CPI), investors will be unwilling to purchase a bond paying 4% and lose purchasing power. Lenders will need to raise interest rates to keep up with inflation. In an inflationary environment, investors may be less inclined to make long-term investments. The possibility that a long-term bond or other long-term investment will not keep up with inflation may drive investors to short-term and variable-rate bonds. Unfortunately, to grow, many businesses, especially capital-intensive companies such as oil and gas refineries, airlines, and telecommunications companies need to borrow for the long-term. As a result, an inflationary environment can reduce business investment and cause an economic downturn.

What are inflation expectations?

To return to the Solomon LinkedIn poll – does it matter what people think will happen with inflation in the future? The short answer is yes, and there’s even a term for this: inflation expectations. Inflation expectations refer to the rate at which people and businesses expect prices to rise in the future. Inflation expectations are important because they can actually affect the real rate of inflation. For example, if everyone expects prices to increase by two percent over the next year, then businesses will likely raise their prices by two percent or more, and workers will want comparable salary increases. If the Solomon LinkedIn poll results are any indication, inflation expectations for the next year are that prices will increase. Do you agree that 2022 will see a rise in the rate of inflation? Comment below to share your thoughts on the topic. Follow Solomon on LinkedIn for more polls, industry updates, study tips, and more!

What does it take to pass securities licensing exams like the SIE, Series 24, Series 63, and Series 79? Read about one student’s approach to success. Continue reading

No one said career changes are easy, and when they involve taking several difficult securities licensing exams, the challenge is real. Having an effective study system is an important part of passing securities licensing exams, and hearing about others’ strategies can help you develop a system that works for you. Solomon Exam Prep recently interviewed Alec Orudjev, General Counsel at FT Global Capital, about passing the SIE, Series 24, Series 63, and Series 79 exams (in three months!). Alec shares valuable insights into his study process and how he utilizes Solomon materials to achieve success.

“… the Solomon study materials are the best and the most comprehensive (notes, resources, simulated exam questions, etc.) in their class, in my view.“

Alec Orudjev

Solomon Exam Prep: What motivated you to pursue multiple securities licenses?

Alec Orudjev: After about two decades of being an attorney in private practice, I decided to change my career path and accepted an in-house legal counsel position earlier in the year. As a condition of such change, I needed to secure certain FINRA licenses.

Solomon Exam Prep: Why did you take your exams in the order that you did? Was this order helpful, or would you change anything if you had to do it again?

Alec Orudjev: I have passed the SIE, Series 79, 63 and 24 tests, and am currently studying for the Series 7 exam. While some of this sequence is dictated by FINRA rules, etc., a great deal of it is a matter of personal planning. Given the overlapping nature of the substance of these tests, I thought it would be helpful to plan the sequence to benefit from common points/concepts across different tested areas. Basically, I focused on the end objective and reviewed the substance of each test to line them up so as to utilize my time most efficiently and effectively.

Solomon Exam Prep: Out of the exams you passed, which one required the most study time and why?

Alec Orudjev: Looking back, I think the Series 24 exam commanded most of my study time and attention. I think the volume of what was to be covered and the overall fatigue of having to study and pass three FINRA exams in a 2 ½ month period both made this test preparation more difficult than it would or should have been. It is a very saturated, broad themed exam that requires a lot of focus and attention.

Solomon Exam Prep: How did you approach studying for your exams?

Alec Orudjev: My approach included: (i) outlining, and (ii) attending Solomon live classes and utilizing exam simulators. With respect to the first element, I approached all my exam preparations the way I did my law school exams – by first preparing thorough outlines of the reading materials. I would start by reading the Solomon preparation materials, actively engaging them and highlighting key points, concepts and examples. Next, I would transfer (literally and figuratively) those notes into an outline of my own, condensing the reading materials down to their bare essence. For example, five chapters of the Series 24 prep book (about 500 pages) were condensed to a 50-page outline (10:1 ratio or so) which, then, I used in reviewing in preparation for the test. Needless to say, one’s outline is as good as one’s effort and the quality of the underlying study materials. On the latter point – the Solomon study materials are the best and the most comprehensive (notes, resources, simulated exam questions, etc.) in their class, in my view. While this outlining approach seems like a lot of work, it is. However, it has worked for me for years and I do strongly recommend this approach to all.

With respect to the second element of my approach, I made every effort to attend live classes and utilize exam simulator questions. I will then turn to Solomon’s online exam question bank and answer those questions, noting what I got right and, more importantly, what and why I got wrong. Also, a significant part of my preparations involved participation in live classes offered by Solomon (I enrolled in the SIE and 63 sessions). You tend to get lot more out of these sessions if you review the materials ahead of time. Overall, they are terrific – the instructor is sharp and very knowledgeable, with a healthy sense of humor to get you through some rather dense and tedious parts of the material. I would highly recommend taking live sessions as they force you to focus on the totality of the study materials in five days, 3-4 hours a day – a daunting, but useful exercise.

“Studying for any difficult test is no pleasant experience … take breaks, change the nature of your mental engagement (read something else altogether, watch, take a walk, etc.) to refresh and resume your studying effort.”

Solomon Exam Prep: How did you take the exams – at a testing center or remotely? How was your experience, and do you have any tips to share?

Alec Orudjev: I took all exams (4 + 1 more to go) at the ProMetric testing center in Bethesda, MD. Given the stress of test-taking, in general, I did not want to add the stress of doing it remotely, etc. The conditions at the center were superb, the staff – very friendly and helpful. I offer no new advice on how to handle this experience other than what is commonly suggested for test takers, e.g., arrive early, read test center instructions carefully and follow them to the letter, give yourself enough time to travel, relax and focus before the test, pace yourself during the test, etc. Keep in mind, however, that FINRA tests are uniquely stringent in the way they are administered, etc. So, to reiterate – read the test taking instructions closely.

Solomon Exam Prep: Any words of wisdom to help motivate others who are preparing for exams?

Alec Orudjev: Focus on the reasons why you have undertaken this effort. Studying for any difficult test is no pleasant experience, and very few things can make that less so. However, take breaks, change the nature of your mental engagement (read something else altogether, watch, take a walk, etc.) to refresh and resume your studying effort. There will be many distractions and excuses – acknowledge and indulge to some extent, but do not lose your focus. Most importantly, be honest with yourself about how disciplined you are studying and preparing for your exams.

Solomon Exam Prep: How has passing the SIE, Series 24, Series 63, and Series 79 exams affected your work and your career?

Alec Orudjev: Certainly. Apart from the obvious, studying helped me to be a better legal professional and advisor. Understanding and internalizing a large, complex body of laws, rules and regulations governing the conduct of member firms is a daunting task indeed. These exams set a useful baseline for developing this understanding and building upon it. Take solace in this idea and keep at it.

If you’re preparing to take a securities licensing exam, such as the SIE, Series 7, or Series 63 (or all three!), Solomon’s latest student interview is a must-read. Continue reading

If you’re interested in becoming a securities industry professional, there are many paths to follow, most of which require you to pass one or more securities licensing exams. Depending on your work and the type of employer, a common exam track is the SIE, Series 7, and Series 63 exams.

The SIE exam covers fundamentals of the securities industry and is a co-requisite to several qualification exams, including the Series 7. The Series 7 qualifies you to buy and sell the widest range of securities. The Series 63 covers the principles of state securities regulation.

Passing all three exams requires considerable effort – but it is possible! Solomon Exam Prep recently interviewed Andrew Nerys, Brokerage Operations Specialist at Cash App Investing, about passing the SIE, Series 7, and Series 63. Read about how Andrew approached studying for these exams, his experience taking exams both remotely and in-person, and how passing these securities licensing exams has benefited his career.

“Passing these exams allowed me to make an exciting transition to a new team and gave me a sense of direction for my professional future.”

Andrew Nerys

Solomon Exam Prep: What motivated you to pursue multiple securities licenses?

Andrew Nerys: To be considered for a permanent role with my organization, it was required for me to pass the three exams I took.

Solomon Exam Prep: Why did you take your exams in the order that you did? Was this order helpful, or would you change anything if you had to do it again?

Andrew Nerys: I took the SIE, followed by the Series 7 and, lastly, the Series 63. I ultimately didn’t get much say in the order or scheduling of my exams but I did find it helpful all the same. I found that preparing for the SIE (and taking the exam) was a good introduction to the concepts and regulations of the securities industry. The Series 7 built on the concepts that were introduced in the SIE and gave me a good foundation. Taking the Series 63 last was refreshing, in a way, since I found it easier to absorb the material and there was much less to cover in preparation for the exam. I don’t think I’d change anything if I had to do it all again which, hopefully, won’t ever be the case!

Solomon Exam Prep: Out of the exams you passed, which one required the most study time and why?

Andrew Nerys: The Series 7 definitely required the most study time. There’s a lot of material to cover and some of the concepts were challenging for me to understand. As a result, I found the need to re-read several sections and to take more of the practice tests at the end of each chapter. I also started studying each chapter by watching its corresponding Video Lecture, so it sometimes took several hours to get through one chapter’s worth of material. In total, I estimate that I spent just under 100 hours studying for that one exam.

Solomon Exam Prep: How did you approach studying for your exams?

Andrew Nerys: For each of the exams, I started by watching the chapter’s Video Lecture and taking very brief notes. Once finished with the video, I’d move on to reading the Study Guide and taking more comprehensive notes to fill in the gaps. I used a couple of wire-bound notebooks and tried to space everything out so I’d have an easy time finding any info I might be hunting for when I went back to review my notes.

I also tried to stick to the study schedules provided by Solomon as much as I could, but didn’t beat myself up if I fell a day behind. I found that I’d usually make up for it soon enough. I only made flashcards for concepts that I really struggled with, or specific equations that required memorization. Otherwise, I leaned heavily on practice tests – both for each chapter and the ones provided for exam review. The pie charts and Pass Probability™ metrics were very useful in helping me identify areas where I needed more study.

“It’s always worth remembering that passing these exams is achievable, especially on those days where it feels impossible.”

Solomon Exam Prep: How did you take the exams – at a testing center or remotely? How was your experience, and do you have any tips to share?

Andrew Nerys: I had a blended experience with taking the actual exams: I took the SIE and 63 at a testing center and took the Series 7 remotely. I didn’t really have a preference for one over the other, but I’d strongly encourage anyone taking it remotely to make the space as distraction-free and free of clutter as possible. Not only did I find that helpful in keeping me focused, but it also made me feel more confident that my exam result wouldn’t be nullified for failing to meet the remote testing requirements.

The other thing to consider when deciding whether or not to take an exam remotely is that you’re not allowed to have any paper, pen, or calculator on your desk when testing remotely. That means all of the notes and calculations have to be done using your computer, which might be a disadvantage when compared to taking the exam at a testing center.

Solomon Exam Prep: Any words of wisdom to help motivate others who are preparing for exams?

Andrew Nerys: Establish a study routine early in the process that’s easy to stick to and that keeps you regularly engaged in the material. If I took more than one day off between studying, I found it more difficult to get back into study mode.

It’s always worth remembering that passing these exams is achievable, especially on those days where it feels impossible. I also use Reddit and subscribed to a couple of Subreddits that focus on the Series 7 and other related exams. I found it really helpful to have a community that was going through the experience (or had recently been through it) to help keep me motivated and to encourage my success.

Solomon Exam Prep: How has passing the SIE, Series 7, and Series 63 exams affected your work and your career?

Andrew Nerys: Passing these exams allowed me to make an exciting transition to a new team and gave me a sense of direction for my professional future. In a more indirect way, it also helped reinforce the feeling that I’m capable of achieving my goals when I have the right resources and mindset.

Visit the Solomon Exam Prep website to explore study materials for 21 different securities licensing exams, including the SIE, Series 7, and Series 63.

Read the results of Solomon Exam Prep’s latest poll on the topic of cryptocurrency regulation – and learn which license you’d need for either outcome. Continue reading

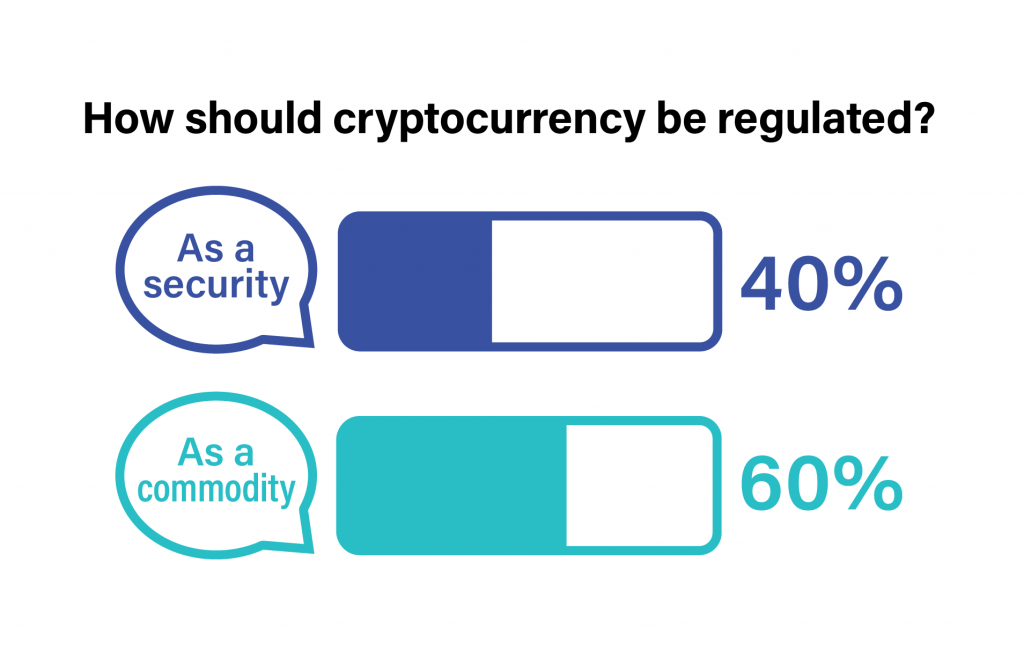

With the regulatory status of Bitcoin and other cryptocurrencies still up in the air, a recent Solomon LinkedIn poll found that 60% of Solomon customers think cryptocurrencies should be treated as commodities, while 40% said they thought cryptocurrencies should be regulated as securities.

Thus far the SEC has avoided clearly stating that cryptocurrencies are securities. To do so, the SEC would likely have to show that cryptocurrencies meet the “Howey Test,” which says that securities must have four characteristics. According to this test, a security involves (1) an investment of money that (2) involves a common enterprise (3) in which the investors expect to make a profit, and (4) the profits will be derived from the efforts of someone other than the investor.

If the SEC, Congress, or the courts declare that cryptocurrencies meet the Howey Test and are therefore securities, Solomon’s got you covered with the Series 7 General Securities Representative Exam Guide. This FINRA license allows you to engage in “the solicitation, purchase and/or sale of all securities products.”

If cryptocurrencies don’t meet the Howey Test, they could be regulated as commodities. These are goods such as wheat, gold, and pork bellies. Why might cryptocurrencies fit in with these others? Because commodities are all highly standardized so that they can be freely bought and sold on exchanges without worrying about differences in quality—every ounce of gold is pretty much like every other ounce of gold. Likewise, every Bitcoin is like every other Bitcoin.