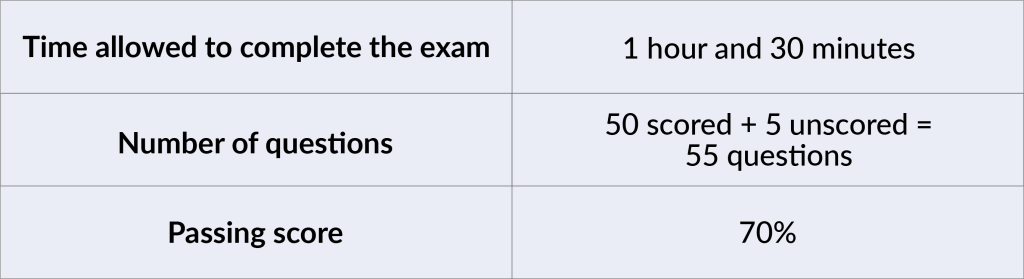

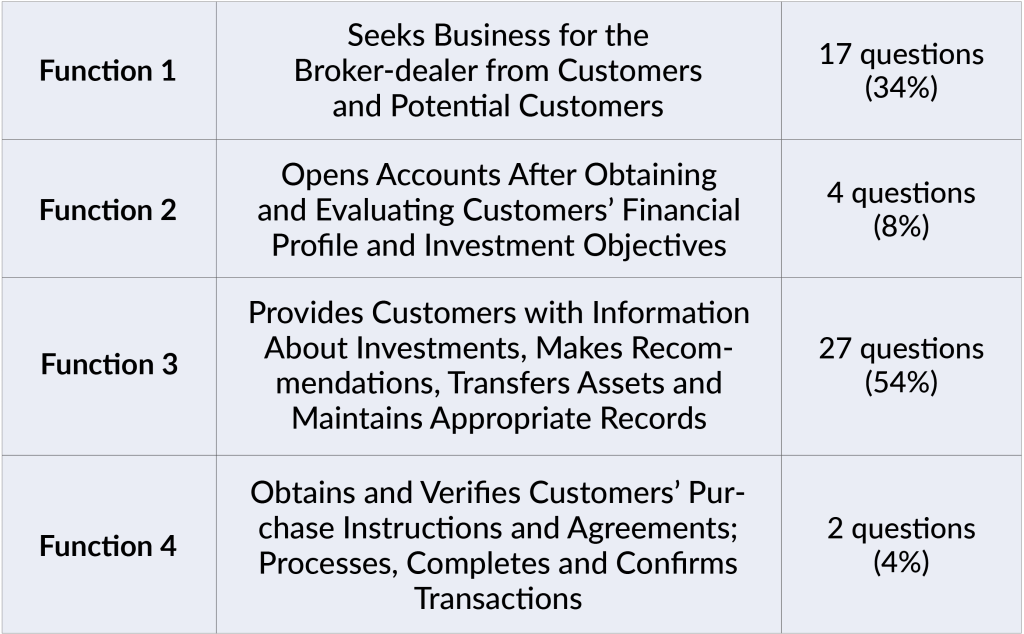

How to Pass the FINRA Series 22 Exam

Thinking about taking the Series 22 exam? Keep reading to learn what the Series 22 qualifies you to do, what the exam covers, and how you should prepare for it. Continue reading

Thinking about taking the Series 22 exam? Keep reading to learn what the Series 22 qualifies you to do, what the exam covers, and how you should prepare for it. Continue reading

If you’re studying for securities licensing exams, such as the SIE or the Series 7, then you should understand the terms “accredited investor” and “QIB.” Continue reading

If you’ve been studying for the Series 7, 6, 14, 22, 24, 65, 79, or 82, or the Securities Industry Essentials (SIE), then you’ve had to learn about Regulation D private placements and Rule 144A sales. Regulation D private placements are securities offerings that are exempt from the normal SEC registration process and in many cases are sold only to “accredited investors” or limit the involvement of investors who are not accredited. Rule 144A sales are sales of unregistered securities to large institutional investors known as “qualified institutional buyers” or QIBs for short.

You may have wondered about the difference between accredited investors and QIBs. On the surface, these may seem similar. Each refers to a category of investor with resources and/or knowledge above and beyond the average retail investor. So why not just have one standard for buyers under both Rule 144A and Regulation D? After all, the purpose of both Regulation D and Rule 144A is the same: to allow wealthier and more sophisticated investors easier access to investments that may be too risky for the average investor.

To begin to answer this question, we have to start with the fact that wealth and sophistication fall on a spectrum. Investors aren’t neatly divided between small retail investors and huge financial institutions that move millions around without blinking an eye.

You could think of accredited investors as a middle ground between these two extremes. Accredited investors are investors whose financial status or investment knowledge may give them a greater ability to handle the risks inherent in a private placement. There are many ways to qualify as an accredited investor but they all have one thing in common, which is that the SEC believes they indicate an ability to take on risks that regulators believe are unsuitable for most retail investors.

Accredited investors are investors whose financial status or investment knowledge may give them a greater ability to handle the risks inherent in a private placement.

An accredited investor that is not an individual—such as a business, governmental, or nonprofit entity—is sometimes called an institutional accredited investor (IAI).

QIBs are a narrower group of large institutional investors. A QIB is a large institutional investor that owns at least $100 million worth of securities, not counting securities issued by its affiliates. For registered broker-dealers, the threshold is lower, just $10 million. A bank must also have a net worth of at least $25 million in order to be considered a QIB.

If a firm has discretionary authority to invest securities owned by a QIB, those securities count toward whether the firm itself is considered a QIB. So if a broker-dealer has $9 million worth of securities in its own accounts, and holds $1 million worth of securities in a discretionary account belonging to a QIB, then the broker-dealer is itself a QIB.

Common examples of QIBs include broker-dealers, insurance companies, investment companies, pension plans, and banks. However, any corporation, partnership, or LLC could qualify as a QIB. So can an IAI that owns at least $100 million in securities. Individuals can never be QIBs, regardless of their assets or financial sophistication.

Individuals can never be QIBs, regardless of their assets or financial sophistication.

Rule 144A allows QIBs to buy unregistered securities at any time, and freely trade these shares to other QIBs. In effect, QIBs can trade unregistered shares among themselves with almost the same ease as trading registered shares. Selling unregistered securities to anyone other than a QIB commonly requires a the seller to hold the securities for a period of up to 12 months.

A QIB will virtually always meet the criteria to be an accredited investor, whereas an accredited investor may fall well short of QIB status.

Over time, other securities laws and regulations have made use of these two well-known categories. For example, in 2019 the SEC gave issuers more flexibility to test the waters with potential investors before deciding whether to go through with a public offering. When deciding which investors were sophisticated enough to receive test-the-waters communications, the SEC limited these communications to QIBs and institutional accredited investors. Additionally, references to institutional accredited investors have become more common, such as when the SEC revamped its rules around integration of offerings in March 2021.

Know your QIBs from your accredited investors and be ready to pass your securities exam with Solomon Exam Prep.

For more helpful securities exam-related content, study tips, and industry updates, join the Solomon email list. Just click the button below:

Watch the latest Solomon Exam Prep video for a complete look at the Solomon learning system and what it offers students and firms. Continue reading

Solomon Exam Prep has helped thousands of financial professionals pass their FINRA, NASAA, MSRB, and NFA licensing exams. Watch the video for a complete look at the Solomon learning system and what it offers students and firms.

To explore Solomon Exam Prep study materials for 21 different securities licensing exams, including the SIE and the Series 3, 6, 7, 14, 22, 24, 26, 27, 28, 50, 51, 52, 53, 54, 63, 65, 66, 79, 82, and 99, visit the Solomon website.

This month’s study question from the Solomon Online Exam Simulator question database is now available. Continue reading

This month’s study question from the Solomon Online Exam Simulator question database is now available.

***Comment below or submit your answer to info@solomonexamprep.com to be entered to win a $20 Starbucks gift card.***

This question is relevant to the SIE, Series 6, 7, 22, 24, and 82 exams.

Question:

Which of the following people would be considered a specified adult?

Answer Choices:

A. A 16 year old with autism

B. A 30 year old

C. A 60 year old with a heart condition

D. An 18 year old in a coma

Correct Answer: D

Explanation: A specified adult is a natural person age 65 and older or a natural person age 18 and older who the member firm reasonably believes has a mental or physical impairment that renders the individual unable to protect his or her own interests.

On November 2, the SEC announced a collection of rule changes meant to, in the announcement’s words, “harmonize, simplify, and improve” its “overly complex exempt offering framework.” Continue reading

Get answers to some of your burning Series 22 questions from Jeremy Solomon, Solomon Exam Prep owner and president, plus test day tips! Continue reading

Did you know that the FINRA Series 22 exam is a much easier path to becoming a direct participation program representative than the Series 7? A shorter exam requiring less study time, and you’re on your way to being qualified to solicit and sell interests in DPPs, including real estate, oil and gas, equipment leasing, BDCs, agricultural, like-kind exchanges, etc.

Click on the video link above and get answers to some of your burning Series 22 questions from Jeremy Solomon, Solomon Exam Prep owner and president, plus test day tips!