Audiobook Study Guide for the Series 53 Exam Now Available

An audiobook version of the Solomon Exam Prep Series 53 Study Guide is now available for the first time for professionals studying for the MSRB Series 53 exam. Continue reading

An audiobook version of the Solomon Exam Prep Series 53 Study Guide is now available for the first time for professionals studying for the MSRB Series 53 exam. Continue reading

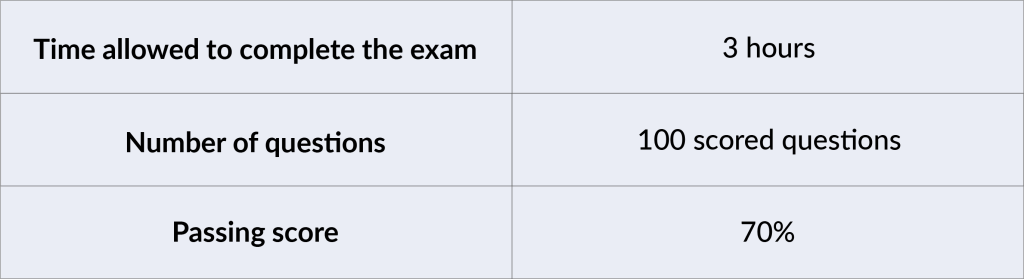

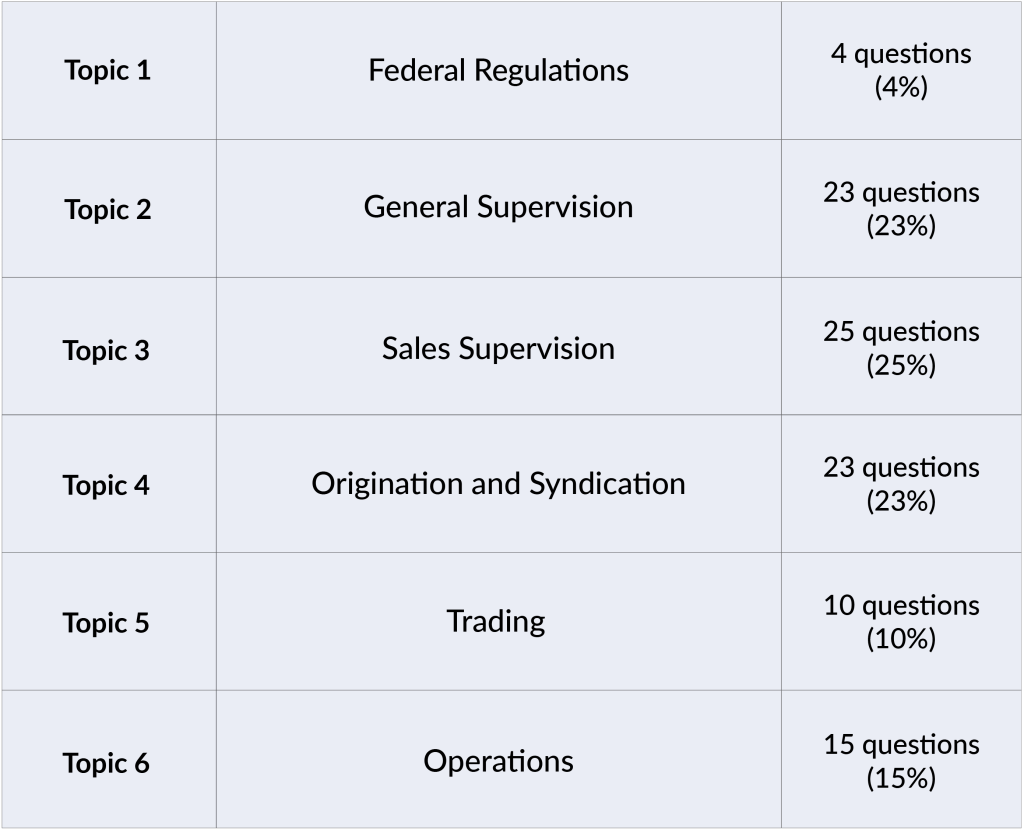

What is the Series 53 exam? Learn what a Series 53 license qualifies you to do, what the exam covers, and how you should prepare for it. Continue reading

The 4th edition of the Solomon Series 53 Study Guide covers everything you need to know to pass the Series 53 Exam and become a Municipal Securities Principal. Continue reading

For a number of securities exams, you should understand the term “tender.” Solomon explains what the term means and how it’s used in the securities industry. Continue reading

MSRB Rule G-18, effective March 21, 2016, establishes a best-execution rule for municipal security transactions. The rule requires brokers and dealers to make reasonable efforts to find as favorable a price as possible for a customer’s transaction, given the prevailing conditions of the market. G-18 is comparable to FINRA Rule 5310, though it is designed specifically to meet the needs of the municipal securities market. —This post is relevant to the Series 52 and Series 53.— Continue reading

MSRB Rule G-18, effective March 21, 2016, establishes a best-execution rule for municipal security transactions. The rule requires brokers and dealers to make reasonable efforts to find as favorable a price as possible for a customer’s transaction, given the prevailing conditions of the market. G-18 is comparable to FINRA Rule 5310, though it is designed specifically to meet the needs of the municipal securities market.

In deciding how and where to execute a trade, a broker-dealer is expected to consider these factors:

• The character of the market for the security, such as its price, volatility, and liquidity

• The size and the type of transaction

• The number of markets checked

• The information reviewed to determine the current market for the security or similar securities

• The accessibility of the quotation

• The terms and conditions of the transaction as communicated to the broker-dealer

Because municipal securities trade over-the-counter, the term “market” should be interpreted broadly to include trading among broker’s brokers, alternative trading systems, or other counter-parties. Dealers must be especially vigilant with transactions in markets where trading is thin and limited pricing information is available.

If a dealer does not get the best price possible in the market, this does not necessarily mean that reasonable diligence was not used. However, if the dealer makes another trade soon after and gets a better price for a similar security and there has been no significant change in the market, this is an indicator that the dealer did not use reasonable diligence.

The following are a few examples of characteristics that may be used to determine if two securities are similar:

• Issuer

• Source of repayment

• Credit rating

• Coupon

• Maturity

• Redemption features

• Sector of the market

• Geographical region

• Tax status

Broker-dealers must institute written policies and procedures that address how they will make a best-execution determination in the absence of pricing information or multiple quotations. They must document compliance with those policies and conduct reviews at least once a year to assess their effectiveness.

Broker-dealers are exempt from the best execution requirement when acting on behalf of a sophisticated municipal market professional (SMMP). An SMMP is:

• A bank, savings and loan association, insurance company, or investment company

• A registered investment adviser

• Any other individual or entity having total assets of at least $50 million

Note: Because broker-dealers are not considered to be customers, the best-execution standard does not have to be applied to trades between broker-dealers that are not on behalf of a customer.

This post is relevant to the Series 52 and Series 53.

EMMA, the Electronic Municipal Market Access website, now allows issuers to voluntarily share bank loan disclosure information online. Continue reading

EMMA, the Electronic Municipal Market Access website, now allows issuers to voluntarily share bank loan disclosure information online.

EMMA was created by the MSRB to give investors online access to official statements for municipal bonds, as well as other disclosure documents. By adding the ability for issuers to share bank loan disclosure information, the MSRB is helping to provide investors with more transparency and more information with which to approach the municipal market.

The information can be posted on the issuer’s customized homepage. Getting it displayed is a two-step process. First, the issuer must submit the bank loan disclosure via the EMMA Dataport Submission Portal. Once the information is submitted, it can be published on the Customized Issuer Homepage by using the Issuer Dashboard.

Investors will find bank loan disclosures and other documentation under the Continuing Disclosure tab on the issuer’s customized homepage.

EMMA is covered on the Series 7, 50, 51, 52, and 53 exams. For more information about EMMA and the services it provides, please visit: http://emma.msrb.org/aboutemma/overview.aspx

“I passed my Series 53! “ Continue reading

This month’s study question from the Solomon Online Exam Simulator question database is now available. Submit your answer for a chance to win a $10 Starbucks gift card! Relevant to the Series 7, 24, 26, 27, 51, 52, 53, 62, 79, 82, 99. –ANSWER POSTED– Continue reading

This month’s study question from the Solomon Online Exam Simulator question database is now available.

***Submit your answer to info@solomonexamprep.com to be entered to win a $10 Starbucks gift card.***

Question (Relevant to the Series 7, Series 24, Series 26, Series 27, Series 51, Series 52, Series 53, Series 62, Series 79, Series 82, Series 99)

Jon and Jenny are married. They each have an individual account and they have a joint account owned by both of them. What is the combined maximum SIPC coverage for all their accounts?

Answers:

A. $500,000

B. $1,000,000

C. $1,500,000

D. $750,000

Correct Answer: C. $1,500,000

Rationale: SIPC covers a maximum of $500,000 per “separate customer” at a broker-dealer or clearing firm including up to $250,000 in cash.Total coverage can be higher for multiple accounts if the accounts are considered to be held by separate customers. There are five categories of separate customers defined by SIPC. These categories include 1) individual accounts, 2) joint accounts, 3) accounts held by executors, administrators, and guardians/custodians/conservators (such as UGMA accounts), 4) accounts held by corporations, partnerships, or unincorporated associations, and 5) trust accounts. Thus, two individual accounts held by two different people, and one joint account would be considered three separate customers by the SIPC, and therefore subject to a maximum of $1,500,000 of coverage.

Congratulations! This month’s winner is Abe B.

Weekly study questions are from Solomon’s industry-leading Online Exam Simulator.

The MSRB has added two new rules effective July 9, 2014. They are Rule G-47 (Time of Trade Disclosure) and Rule G-48 (Transactions with Sophisticated Municipal Market Professionals). MSRB has also amended Rule G-3 (Classification of Principals and Representatives) and Rule G-19 (Suitability), effective September 30, 2014. These four changes coordinate MSRB rules with FINRA rules and remove regulatory redundancies. Continue reading

The MSRB has added two new rules effective July 9, 2014. They are Rule G-47 (Time of Trade Disclosure) and Rule G-48 (Transactions with Sophisticated Municipal Market Professionals). MSRB has also amended Rule G-3 (Classification of Principals and Representatives) and Rule G-19 (Suitability), effective September 30, 2014. These four changes coordinate MSRB rules with FINRA rules and remove regulatory redundancies.

MSRB Rule G-3. MSRB narrows the definition of Limited Representative – Investment Company and Variable Contracts Products (Series 6). Under FINRA rules, a Series 6 license only allows individuals to be involved in the purchase and sale of funds and variable products. The new MSRB rule will now be consistent with the FINRA rules. Representatives who want to participate in broader activities, such as underwriting, research and investment advice must now take and pass the Municipal Securities Representative Qualification Examination (Series 52).

Amended Rule G-3 also eliminates the designation of Municipal Securities Financial and Operations Principal (FINOP). Since municipal securities dealers that require a FINOP are also FINRA members and since FINRA has similar FINOP requirements, Rule G-3 eliminates the redundancy by removing its separate FINOP designation.

MSRB Rule G-19. MSRB’s amended suitability rule conforms to FINRA’s own recent changes to its rule. Specifically, the amended rule recognizes three components to a broker-dealer’s suitability obligations. First, a broker-dealer must understand the complexity and risks of a security or investment strategy and consciously decide its suitability for at least some investors. Second, it must reasonably believe that a recommendation is suitable for a particular customer based on the customer’s personal and investment profile. Third, when a broker-dealer has control over a customer account, it must reasonably believe that a series of recommended securities transactions are not excessive.

MSRB Rule G-47. This new rule requires broker-dealers to disclose to its customers all material information about a transaction and the security at or prior to the time of trade. Information is considered “material” if a reasonable investor is likely to consider it important in making an investment decision. Disclosures must include a complete description of the security and any facts important to assessing the potential risks of the investment.

MSRB Rule G-48. Rule G-48 exempts broker-dealers from any obligation to disclose material information to customers who are sophisticated municipal market professionals (SMMPSs). It also exempts broker-dealers from informing an SMMP that the price of a secondary market agency transaction is fair and reasonable, as long as the broker-dealer has not recommended the transaction or exercised discretion as to its execution. Finally, Rule G-48 exempts broker-dealers from the obligation to perform a customer-specific suitability analysis for an SMMP.

This week’s study question from the Solomon Online Exam Simulator question database is now available. Relevant to the Series 7, 51, 52, 53, 62, 82, and 99. –ANSWER POSTED– Continue reading

This week’s study question from the Solomon Online Exam Simulator question database is now available.

Question (Relevant to the Series 7, Series 51, Series 52, Series 53, Series 62, Series 82, and Series 99):

When money is regularly put into an escrow account in order to redeem the bonds before maturity this is called:

Answers:

A. A sinking fund redemption

B. Advance refunding

C. Defeasement

D. A make whole provision

Correct Answer: A. A sinking fund redemption

Rationale: A sinking fund redemption requires the issuer to set money aside regularly in a reserve account for the redemption of the bonds before maturity.

Weekly study questions are from Solomon’s industry-leading Online Exam Simulator.