How to Pass the FINRA Series 22 Exam

Thinking about taking the Series 22 exam? Keep reading to learn what the Series 22 qualifies you to do, what the exam covers, and how you should prepare for it. Continue reading

Thinking about taking the Series 22 exam? Keep reading to learn what the Series 22 qualifies you to do, what the exam covers, and how you should prepare for it. Continue reading

The Series 22, also called the Direct Participation Programs Representative Exam, is a FINRA (Financial Industry Regulatory Authority) exam. FINRA is an independent, self-regulatory organization that creates and enforces rules for registered broker-dealer firms and their representatives. FINRA is also responsible for administering securities licensing exams, such as the Securities Industry Essentials (SIE) exam, Series 7 exam, Series 22 exam, and many more.

The Series 22 exam measures the knowledge of entry-level registered representatives to perform their duties as Direct Participation Programs Representatives. Taking the exam will help you understand your professional responsibilities, including the solicitation, purchase, and sale of limited partnerships, among other products.

Did you know that the Series 22 exam is an easier path to becoming a direct participation program representative than the Series 7? The Series 22 is a shorter exam requiring less study time. Pass it and you’re on your way to being qualified to solicit and sell interests in direct participation programs (DPPs), including real estate, oil and gas, equipment leasing, BDCs, agricultural, and like-kind exchanges.

A DPP is FINRA term for a pass-through entity, such as a limited partnership or S-corp, whose shares indicate ownership, not of an operating company, but of certain physical assets of the company. As a pass-through entity, DPPs can offer tax benefits to investors, but they are not suitable for all investors, and they are not liquid investments.

Other permitted activities and products with a Series 22 license include:

You must be employed and sponsored by a FINRA-member firm to take the Series 22 exam.

To obtain the Series 22 qualification, you must also pass the co-requisite Securities Industry Essentials (SIE) exam. Unlike the Series 22 exam, the SIE does not require you to be sponsored by a broker-dealer.

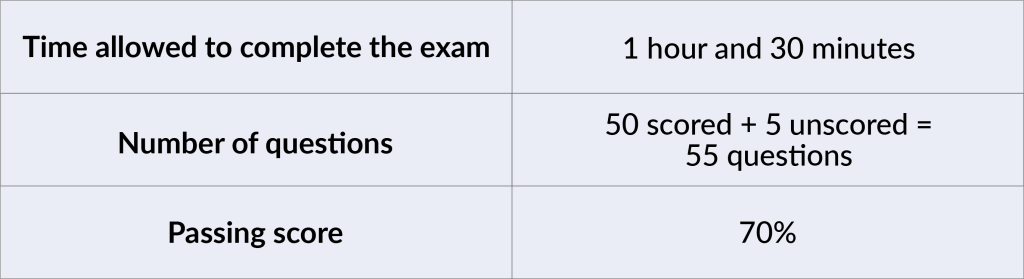

The Series 22 exam consists of 50 scored and five unscored multiple-choice questions. The five unscored questions are experimental questions and appear randomly.

Note: Scores are rounded down to the next lowest whole number (e.g. 69.9% would be a final score of 69%–not a passing score for the Series 22 exam).

Topics Covered on the Exam

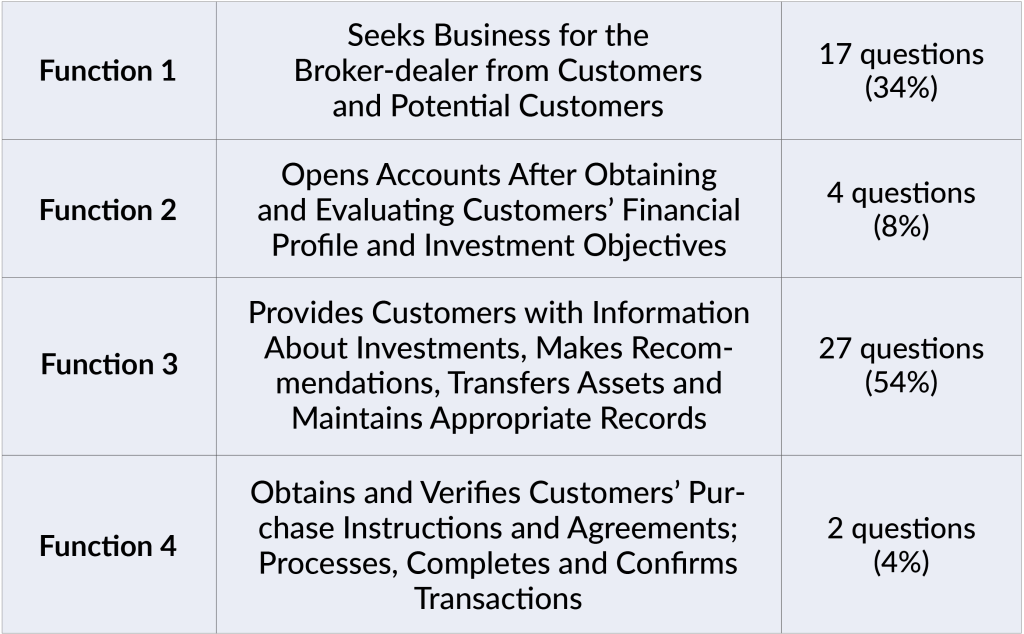

FINRA divides the questions on the Series 22 exam into four areas representing the four major job functions of a Direct Participation Programs Representative. FINRA updates its exam questions regularly to reflect the most current rules and regulations.

Solomon recommends that you print out the current version of the FINRA Series 22 Content Outline and use it in conjunction with the Solomon Series 22 Study Guide. The Content Outline is subject to change without notice, so make sure you have the most recent version.

Series 22 Example Questions

The Series 22 exam consists of multiple-choice questions, each with four options. You may see the following question structures. However, keep in mind that these sample questions don’t necessarily represent the difficulty level or subjects covered in the exam.

This item type asks a question and gives four possible answers to choose from.

Which of the following could potentially be a DPP?

This kind of question has an incomplete sentence followed by four possible conclusions.

Owners of limited liability companies (LLCs) are considered:

This type requires an answer that is incorrect or is an exception among the four answer choices.

Each of the following can cause an LP to be dissolved before the date specified in its Certificate of Limited Partnership, except:

For more Series 22 practice questions, try a free sample of Solomon Exam Prep’s Series 22 Exam Simulator. You’ll receive instant feedback on each question with a robust explanation of the correct answer.

FINRA administers the Series 22 exam, and you must take it at a Prometric test center. The exam is given via computer. Before the exam, you’ll be able to watch a tutorial on how to take the exam.

Like all qualifying exams in the securities industry, the Series 22 is closed-book, and you’re not allowed to bring anything into the exam. The test center will provide you with any materials you need to complete the exam. For instance, the test center may provide a whiteboard with markers or scratch paper and a pencil, as well as a basic electronic calculator. The inspection and sign-in requirements at test centers are stringent, so plan to arrive at least 30 minutes before your scheduled test appointment.

When taking the exam, it helps to keep some test-taking strategies in mind. Try not to spend too long on one question—this may cause you to run out of time and not get to other questions you know. If you don’t know the answer to a question, guess at the answer and mark it for review . There’s no penalty for guessing, so it’s beneficial to answer every question.

After you’ve finished all the questions, you can return to any flagged questions. This strategy allows you to efficiently answer the ones you know. You might also learn something later in the exam that helps you answer an earlier question. Just remember to save enough time to return to the questions you didn’t answer. However, it’s not a good idea to simply skip all of the difficult questions with the plan to answer them later. You should make a serious effort to answer each question before moving on to the next one since your thoughts are often clearer earlier on during the exam.

You can pass the FINRA Series 22 exam! It just takes focus and determination. Solomon Exam Prep is here to support you on your path to becoming a Direct Participation Programs Representative.

Explore all Solomon Series 22 exam prep, including the Study Guide and Exam Simulator.

And join the Solomon email list to hear about new product releases, industry news, and more! Just click the button below:

Thinking about taking the Series 99 exam? Keep reading to learn what the Series 99 qualifies you to do, what the exam covers, and how you should prepare for it. Continue reading

The Series 99, also called the Operations Professionals Exam, is a FINRA (Financial Industry Regulatory Authority) exam. FINRA is an independent, self-regulatory organization that creates and enforces rules for registered broker-dealer firms and their representatives. FINRA is also responsible for administering securities licensing exams, such as the Securities Industry Essentials (SIE) exam, Series 7 exam, Series 99 exam, and many more.

The Series 99 exam measures the knowledge of entry-level registered representatives to perform their duties as Operations Professionals. The exam will help you understand your professional responsibilities, including key regulatory and control requirements. It will assess your broad understanding of the following:

Obtaining a Series 99 qualification will permit you to perform crucial functions in a broker dealer’s operations department. Duties may include customer onboarding, financial control, stock loan/securities lending, trade confirmation, and issuing account statements.

Yes, you must also pass the co-requisite Securities Industry Essentials (SIE) exam to obtain the Series 99 qualification. To take the Series 99 exam, you must be employed and sponsored by a FINRA-member firm.

If you hold any of the following registrations, you can qualify as an Operations Professional without taking the Series 99 exam:

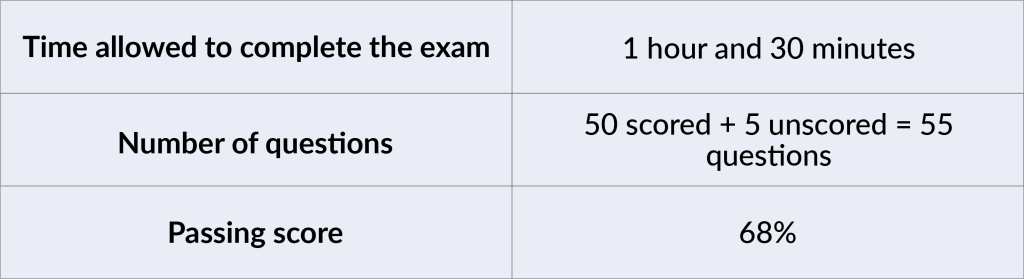

The Series 99 exam consists of 50 scored and five unscored multiple-choice questions. The five unscored questions are experimental questions and appear randomly.

Note: Scores are rounded down to the next lowest whole number (e.g. 67.9% would be a final score of 67%–not a passing score for the Series 99 exam).

Topics Covered on the Exam

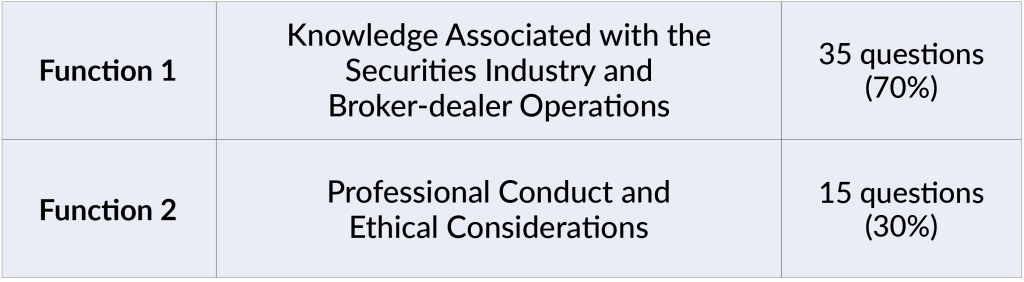

FINRA divides the questions on the Series 99 exam into two parts representing the two major job functions of an Operations Professional.

FINRA updates its exam questions regularly to reflect the most current rules and regulations. Solomon recommends that you print out the current version of the FINRA Series 99 Content Outline and use it in conjunction with the Solomon Series 99 Study Guide. The Content Outline is subject to change without notice, so make sure you have the most recent version.

Series 99 Example Questions

The Series 99 exam consists of multiple-choice questions, each with four options. You may see the following question structures. However, keep in mind that these sample questions don’t necessarily represent the difficulty level or subjects covered in the exam.

This item type asks a question and gives four possible answers to choose from.

Which of the following is not a factor that can be used to determine whether securities were not delivered in good form and are therefore subject to possible rejection?

This kind of question has an incomplete sentence followed by four possible conclusions.

Shoestring Discount Stock Jocks owns no shares of stock in any exchange-traded companies. In its efforts to execute a buy order for your account, it would be acting as a:

This type requires an answer that is incorrect or is an exception among the four answer choices.

All of the following are definitely DTC-eligible securities, except:

Try a free sample of Solomon Exam Prep’s Series 99 Exam Simulator. You’ll receive instant feedback on each question with a robust explanation of the correct answer.

FINRA administers the Series 99 exam, and you must take it at a Prometric test center. The exam is given via computer. Before the exam starts, you’ll take a tutorial on how to take the exam. After you finish the tutorial, the exam will begin and you’ll have one hour and 30 minutes to complete it.

Like all qualifying exams in the securities industry, the Series 99 is closed-book, and you’re not allowed to bring anything into the exam. The test center will provide you with any materials you need to complete the exam. For instance, the test center may provide a whiteboard with markers or scratch paper and a pencil, as well as a basic electronic calculator. Or, a digital calculator and notepad will be available within the computer testing platform.

The inspection and sign-in requirements at test centers are stringent, so plan to arrive at least 30 minutes before your scheduled test appointment.

When taking the exam, it helps to keep some test-taking strategies in mind. Try not to spend too long on one question—this may cause you to run out of time and not get to other questions you know. If you don’t know the answer to a question, guess at the answer and mark it for review . There’s no penalty for guessing, so it’s beneficial to answer every question.

After you’ve finished all the questions, you can return to any flagged questions. This strategy allows you to efficiently answer the ones you know. You might also learn something later in the exam that helps you answer an earlier question. Just remember to save enough time to return to the questions you didn’t answer. However, it’s not a good idea to simply skip all of the difficult questions with the plan to answer them later. You should make a serious effort to answer each question before moving on to the next one since your thoughts are often clearer earlier on during the exam.

You can pass the FINRA Series 99 exam! It just takes focus and determination. Solomon Exam Prep is here to support you on your path to becoming an Operations Professional.

Explore all Solomon Series 99 exam prep, including the Study Guide, Exam Simulator, and Video Lecture.

And join the Solomon email list to hear about new product releases, industry news, and more! Just click the button below:

Be prepared for questions about SIMPLE, SEP, and solo 401(k) retirement account plans on the FINRA Series 6 and Series 7 exams. Continue reading

If you are studying for the FINRA Series 6 or Series 7 exam, you will need to learn about the different types of retirement plan accounts. A retirement account may be an individual plan that is managed by the participant or the participant’s agent, such as an investment firm or a trust bank. Or it may be employer-sponsored, meaning that it is organized and managed by the participant’s employer.

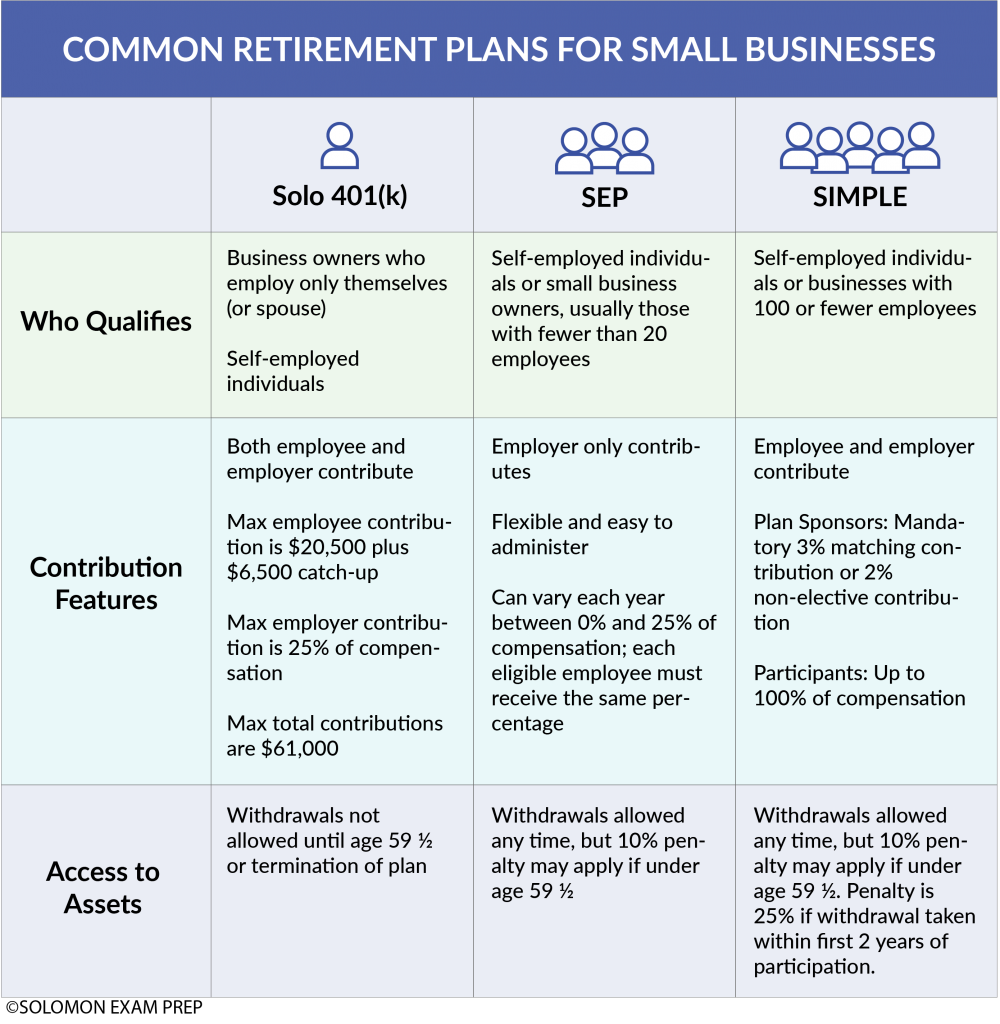

Private employers of any size and structure, from the largest C corporation to a sole proprietorship consisting of a single self-employed individual, may set up and use an employer-sponsored retirement plan. For small business owners, retirement plans offer significant tax advantages and can help attract employees. Since there are several types of retirement plans available for small businesses, it’s important to understand the features of each option. Three plans commonly chosen by small businesses are solo 401(k) plans, SEP plans, and SIMPLE plans.

A business owner can open a solo 401(k) if the business does not employ anyone else. The owner of the business creates a 401(k) plan much like any other employer. Then, as an employee, the owner opens a 401(k) account within that plan.

Both employer and employee contributions can be made in a solo 401(k). The maximum employee contribution is the same as for other 401(k)s. As of 2022, this limit is $20,500 per year, with a catch-up contribution of $6,500 for those aged 50 and above. As an employer, the maximum annual contribution is 25% of what the owner pays herself. The combined annual contribution (employee and employer) cannot exceed $61,000.

The business owner is allowed to employ her spouse and still make use of a solo 401(k) plan. The spouse can open their own 401(k) account using the business’s solo 401(k) plan. A solo 401(k) can be created whether the business is set up as a corporation, LLC, or sole proprietorship. Self-employed people who haven’t set up a business can also create a solo 401(k), although their contribution limits are calculated differently.

Unlike most employer-sponsored retirement plans, solo 401(k)s do not need to comply with ERISA (the Employee Retirement Income Security Act). This is a federal law that requires employers to give employees fair access to the employer’s retirement plan. These concerns do not apply when the business has no other employees.

Simplified Employee Pension (SEP) plans are IRA-based retirement plans for any size business but are usually favored by small businesses. Under this type of plan, the business owner can make pre-tax contributions into IRA accounts set up for eligible employees and also for herself if the owner is self-employed.

The plan allows employers to skip contributions in years when business is bad, but if the owner makes a contribution for herself, she must also make contributions for her employees. When contributions are made, they must be made for all participants who actually performed work during the year for which the contributions are made, including those over 72 years of age (the latter feature is unique to the SEP plan). Contributions for all participants generally must be uniform, for example the same percentage of hourly wage.

The business owner can make contributions of up to 25% of an employee’s salary, or an annual maximum of $61,000, whichever is less. Only the employer, and not the employee, makes contributions to the SEP IRA, but an employee is always 100% vested in his SEP IRA. Generally, the employer can take an income tax deduction for contributions made to each employee’s SEP. SEP contributions are not included on the employee’s W-2 statement for tax purposes. Rules for withdrawal of funds are generally the same as for any other IRA, meaning that withdrawals are subject to income taxes, and early withdrawals are usually subject to a penalty.

Savings Incentive Match Plan for Employees (SIMPLE) plans are retirement plans for businesses having no more than 100 employees. With a SIMPLE IRA or SIMPLE 401(k), the employee may make pre-tax contributions to the plan. The contribution is expressed as a percentage of the employee’s compensation and is limited to $14,000 a year ($17,000 for employees aged 50 and over). The employer is required to either match these contributions up to 1% to 3% of the employee’s compensation or to contribute 2% whether the employee makes a contribution or not. The employer chooses which type of contribution (and if matching, the maximum percentage it will match). This choice applies to all employees. So an employer who chooses matching contributions is not obligated to contribute 2% to an employee who chooses not to contribute.

Any employee who previously earned at least $5,000 during any two years and is reasonably expected to receive at least $5,000 during the current calendar year is eligible to participate in this plan. Unlike the SEP plan, however, premature SIMPLE IRA distributions (withdrawals of account funds) will incur a 25% penalty in the first two years the account exists if made before age 59 1/2.

While the SEP plan is discretionary, in that the employer can decide when to fund the plan, funding the SIMPLE IRA plan is mandatory, no matter what kind of year the business had. A SIMPLE 401(k) functions similarly to a SIMPLE IRA. Both have the same contribution limits and are 100% vested from the beginning.

SEP and SIMPLE IRAs have characteristics in common with traditional IRAs. For example, contributions are generally made with pre-tax dollars, must be earned income, and must only be in cash. Taxes on contributions and earnings are deferred until withdrawal, as long as withdrawals occur after the age of 59 1/2. Required minimum distributions (RMDs) must begin the year the participant turns age 72, although the participant may choose to delay the first payment until April 1 of the following year. After that, RMDs must be taken by December 31 each year. Funds can be distributed as a lump sum or in periodic payments. If the account owner fails to withdraw an RMD or the full amount of the RMD before the deadline, the amount not withdrawn is taxed at 50%.

Anyone who plans to become a registered representative by passing the Series 6 or Series 7 exam and assist customers with retirement plans must understand the complexity of retirement planning. The Solomon Exam Prep Series 6 Study Guide and Series 7 Study Guide both cover retirement plan accounts so that you can be prepared for questions about this topic on exam day. Visit the Solomon website to explore study materials for 21 different securities exams, including the Series 6 and 7.

If you’re studying for the FINRA Series 24 exam, take the guesswork out of knowing when you’re ready to take your exam with Solomon’s Pass Probability feature. Continue reading

Preparing for a challenging securities licensing exam like the FINRA Series 24, also known as the General Principal Qualification Exam, can be a stressful experience. In particular, determining when you’ve studied enough and are ready to sit for your exam isn’t always easy. How do you know if those weeks of preparation have paid off?

With the Solomon Exam Prep Pass Probability™ feature, now available in the Solomon Series 24 Exam Simulator, you don’t have to guess whether you’re truly prepared to sit for the Series 24 exam. Pass Probability™ is Solomon Exam Prep’s innovative AI technology that measures your readiness to pass a securities exam. Pass Probability is based on a mathematical model involving the performance of thousands of Solomon students. A correlation analysis has shown that Pass Probability is highly effective at predicting a student’s likelihood of passing.

Here’s how it works: Once you take five full practice exams in the Solomon Series 24 Exam Simulator, the Pass Probability™ tool is activated. Based on your scores on these five practice exams, the tool calculates the probability that you will pass the real test, with a percentage out of 100. Solomon recommends aiming for a Pass Probability of 75% (80% is even better) before taking your exam.

But if your Pass Probability is below 75%, Solomon can help! Connected to the Pass Probability tool, the Solomon Remediation Report provides an additional level of customized study support. If your Pass Probability is lower than 75%, you will receive an individual report with detailed suggestions on how to focus your study efforts BEFORE taking your exam. The Remediation Report is sent straight to your email and includes the following:

Solomon Pass Probability and Remediation Reports are also available for these exams: SIE, Series 6, Series 7, Series 63, Series 65, Series 66, Series 79, and Series 82.

Used Solomon materials for both the SIE and S7. So grateful to these materials for helping me achieve a passing score on my first attempts of both exams. The study guide and videos were thorough, comprehensive and easy to follow. I found the pie charts extremely useful in helping me identify areas where I needed more study, and was grateful for the Pass Probability feature in giving me a bit of extra confidence before sitting for the exam. I would absolutely recommend all of their materials to anyone taking this journey.

Andrew Nerys, Square Inc., Portland, OR

If you have a current subscription to the Solomon Series 24 Exam Simulator, Pass Probability and Remediation Reporting have been added to your product free of charge. These tools are in addition to the other helpful Exam Simulator features:

What can you do with a Series 7 license? What is the exam like and how should you prepare for it? Solomon answers your top Series 7 questions. Continue reading

The Series 7, also known as the General Securities Representative Qualification Exam, was developed by the Financial Industry Regulatory Authority (FINRA) to assess the skills and competency of entry-level registered representatives as general securities representatives. Passing the Series 7 exam qualifies you to solicit, purchase, and/or sell all securities products, including corporate securities, municipal fund securities, options, direct participation programs, investment company products, and variable contracts. As a result of this broad scope, the Series 7 exam is one of the longest and most challenging securities industry exams. The good news, however, is that you will be permitted to perform an impressive range of activities with a Series 7 license. The following are covered activities and products:

In order to be registered as a general securities representative, you must pass two exams: the Series 7 and the FINRA Securities Industry Essentials (SIE) exam. While the Series 7 requires you to be hired and sponsored by a FINRA-member firm, the SIE does not. Therefore, even though you can technically take them in either order, it makes sense to take the introductory-level SIE exam before taking the Series 7 exam.

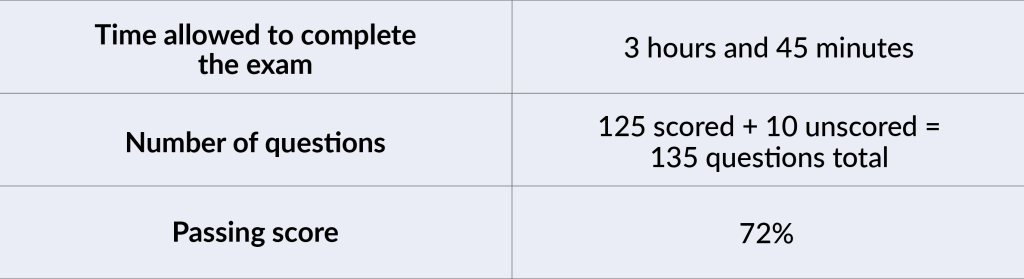

The Series 7 exam consists of 125 scored and 10 un-scored multiple-choice questions covering the four sections of the FINRA Series 7 content outline. The 10 additional un-scored questions are ones that the exam committee is trying out. These are unidentified and are distributed randomly throughout the exam.

Note: Scores are rounded down to the next lowest whole number (e.g. 71.9% would be a final score of 71% – not a passing score for the Series 7 exam).

Topics Covered on the Exam

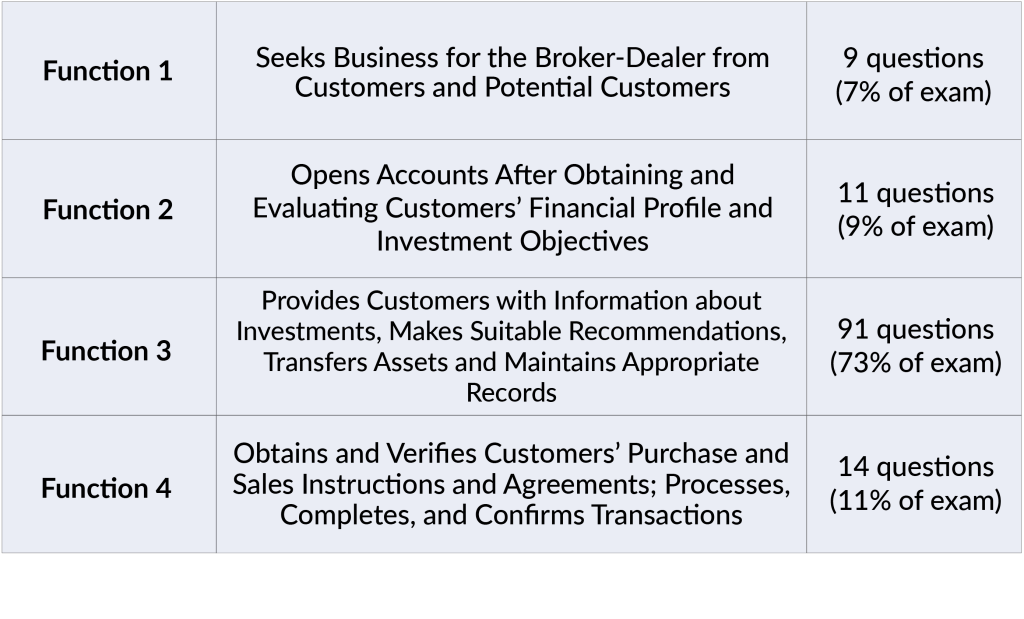

The questions on the Series 7 exam cover the main job functions of a general securities representative, as determined by FINRA:

FINRA updates its exam questions regularly to reflect the most current rules and regulations. Solomon recommends that you print out the current version of the FINRA Series 7 Content Outline and use it in conjunction with the Solomon Series 7 Study Guide. The Content Outline is subject to change without notice, so make sure you have the most recent version.

Question Types on the Exam

The Series 7 exam consists of multiple-choice questions, each with four options. You will see these question structures:

This item type asks a question and gives four possible answers from which to choose.

When interest rates go up, what will happen to the price of typical preferred stock?

This kind of question has an incomplete sentence followed by four options that present possible conclusions.

The owner of a house with a market value of $450,000 and an assessed value of $300,000, and with an ad valorem tax of 4 mills would pay a property tax of:

This type requires you to recognize the one choice that is an exception among the four answer choices presented.

VRDOs may have their rates automatically reset at any of the following frequencies except:

For this question type, you see a question followed by two or more statements identified by Roman numerals. The four answer choices represent combinations of these statements. You must select the combination that best answers the question.

A Build America Bond may:

This format is also used in items that ask you to rank or order a set of items from highest to lowest (or vice versa), or to place a series of events in the proper sequence.

The flow of funds requirement for a municipality with a net revenue pledge usually prioritizes the following funds in which order, going from highest priority to lowest priority?

Answers: B, B, D, C, B

For an even better idea of the possible question types you might encounter on the Series 7 exam, try Solomon Exam Prep’s free Series 7 Sample Quiz.

The Series 7 exam can be taken at a Prometric test center or remotely online using Prometric’s ProProctor system. If taking the exam at a test center, you will be given a dry erase pen and whiteboard or a pen and scratch paper, and a basic electronic calculator. You cannot bring notes, paper, or your own calculator. Phones and watches are not permitted either. Due to COVID-19, you are required to wear a mask the whole time you are at the test center. Solomon recommends taking timed practice exams in the Series 7 Exam Simulator while wearing a mask to get used to this added discomfort.

If you’re thinking about taking the test from the comfort of your own home or office with ProProctor, it’s important to be aware of the strict procedures you must follow. See this user guide for complete details. And for a first-hand account of the remote testing experience, read this Solomon blog post.

Whether you take the exam in person or online, it helps to keep some test-taking strategies in mind. You have an average of slightly more than a minute and a half per question, so don’t spend too long on one question—this may cause you to run out of time and not get to other questions you know. If you don’t know the answer to a question, guess at the answer and “flag” it. You will not be penalized for guessing.

After you have finished all the questions, you can come back to any flagged questions. Not only does this strategy allow you to efficiently answer the ones you know, but it can also help because you might learn something later in the exam that may help you answer an earlier question. Just remember to save enough time to return to the questions you didn’t answer. However, it is not a good idea to simply skip all of the difficult questions with the intention of answering them later. You should make a serious effort to answer each question before moving on to the next one, as your thoughts are often clearer early on in the exam-taking process than they will be later.

You can pass the FINRA Series 7 Exam! It just takes focus and determination. Solomon Exam Prep is here to support you on your path to becoming a general securities representative.

To explore all Solomon Exam Prep’s Series 7 study materials, including product samples, visit the Solomon website here.

For more helpful securities exam-related content, study tips, industry updates, and promotional offers, join the Solomon email list. Just click the button below:

FINRA announced several important changes to its CE rules affecting registered representatives and principals. Learn how these changes may affect you. Continue reading

On November 17th, FINRA announced the adoption of important amendments to its continuing education (CE) rules. These changes will affect individuals with representative or principal registrations, such as the Series 7, Series 24, Series 79, and Series 82. Some of the changes go into effect as soon as March 15, 2022, while others become effective on January 1, 2023.

FINRA’s current CE program consists of a Regulatory Element and a Firm Element. The Regulatory Element focuses on regulatory requirements and industry standards and must be taken every three years by registered individuals. The Firm Element is provided by each firm to its registered persons yearly, and covers the firm’s securities products, services and strategies, policies, and industry trends. Currently, the FINRA CE program does not allow individuals to maintain terminated qualifications by completing CE. Instead, individuals must requalify by examination if they have not reregistered within the two-year qualification period.

The upcoming changes to FINRA CE are outlined in Regulatory Notice 21-41, which states that the changes to Rules 1210 and 1240 will: “(1) provide eligible individuals who terminate any of their representative or principal registration categories the option of maintaining their qualification for any terminated registration categories by completing annual CE through a new program, the Maintaining Qualifications Program (MQP); (2) require registered persons to complete CE Regulatory Element annually for each representative or principal registration category that they hold; and (3) expressly allow firms to consider other required training toward satisfying an individual’s annual CE Firm Element and extend the Firm Element requirement to all registered persons.”

There will be several changes to the FINRA CE Regulatory Element, effective January 1, 2023. Instead of every three years, registered individuals will have to complete CE every year by December 31st. In addition, individuals must complete CE content for each registration category they hold. Another change is that failure to complete the Regulatory Element by Dec. 31 will result in a CE inactive status. However, if “good cause” is shown, FINRA reserves the right to extend the deadline.

The initial annual Regulatory Element completion date will depend on an individual’s registration status:

The initial completion date will be Dec 31, 2023 if…

On the other hand, the initial completion date will be Dec 31, 2024 if…

Also, effective January 1, 2023, the annual Firm Element CE requirement is being extended to include all registered individuals, not just “covered registered persons.” Covered registered persons include registered persons who work with customers, who are registered as research analysts, and individuals who supervise such persons. Starting in 2023, all registered persons will be required to complete the annual Firm Element CE.

Another rule amendment includes allowing training related to the anti-money laundering compliance program under Rule 3310(e) and annual compliance meeting under Rule 3110(a)(7) to go towards satisfying an individual’s Firm Element CE requirement.

FINRA says that to better accommodate registered persons, “particularly women and underrepresented minorities, whose personal circumstances take them away from the industry for a time,” the regulator is creating the new Maintaining Qualifications Program (MQP). Eligible individuals will be able to complete annual CE through the MQP to maintain their qualification for any terminated registration categories. This program will go into effect March 15, 2022, with MQP content available by July 1, 2022. See Regulatory Notice 21-41 for details on eligibility and participation conditions.

Currently, registered persons must retake their qualification licensing exams after two years of losing their representative or principal registration. MQP participants will have a maximum of five years following the termination of a representative or principal registration category to reregister without having to retake their licensing exam or having to obtain an exam waiver.

Starting November 17, 2021, FINRA will begin notifying individuals who were registered as a representative or principal between March 15, 2020, and March 15, 2022, and those participating in the Financial Services Affiliate Waiver Program (FSAWP) prior to March 15, 2022, of their potential eligibility to participate in the MQP. These individuals can start notifying FINRA on January 31, 2022, that they intend to participate in the MQP. This is done through their FinPro accounts. Individuals will have until March 15, 2022, to notify FINRA of their intention. If an individual’s registration category has been terminated but the firm has not submitted a Form U5 to FINRA, the individual may let FINRA know about their intent to participate in the MQP by sending an email to mqpnotice@finra.org by March 15, 2022, at the latest.

Want a curated collection of our most relevant blog posts delivered straight to your email inbox each month? Subscribe to the Solomon Monthly Newsletter and get securities exam study tips, industry news, and more! Just click the button below to join.

What can you do with a Series 79 license? What is the exam like and how should you prepare for it? Solomon answers your top Series 79 questions. Continue reading

The Series 79, also known as the Limited Representative Investment Banking Exam, was developed by the Financial Industry Regulatory Authority (FINRA) to assess the skills and competency of entry-level investment bankers. If you work for a FINRA member firm as an investment banker, you must pass the Series 79 exam and register as an Investment Banking Representative. Although the Series 79 is designed for junior-level bankers, it proves to be one of the most difficult exams offered by FINRA, particularly for test-takers who do not have education and work experience in accounting and finance. In addition, the Series 79 exam requires a broad knowledge of the rules, regulations and industry practices that govern US capital markets and investment banking.

Passing the Series 79 exam qualifies you to advise on and/or facilitate the following:

According to FINRA, the Series 79 does NOT cover sales or marketing of debt or equity securities to investors or potential investors. In order to make investor presentations, an investment banker with the Series 79 registration would also need to be “registered as a General Securities Representative (Series 7), Corporate Securities Representative (Series 62), or Private Securities Offerings Representative (Series 82) depending on the type of offering being made.”

You are also required to take the FINRA Securities Industry Essentials (SIE) exam, unless you have passed certain other licensing exams (such as the Series 7 or Series 82) before October 1st, 2018.

Additionally, in order to comply with state securities regulations, most individuals with the Series 79 registration pass the NASAA Series 63 exam as well. Check with your firm’s compliance officer to determine if this registration applies to you.

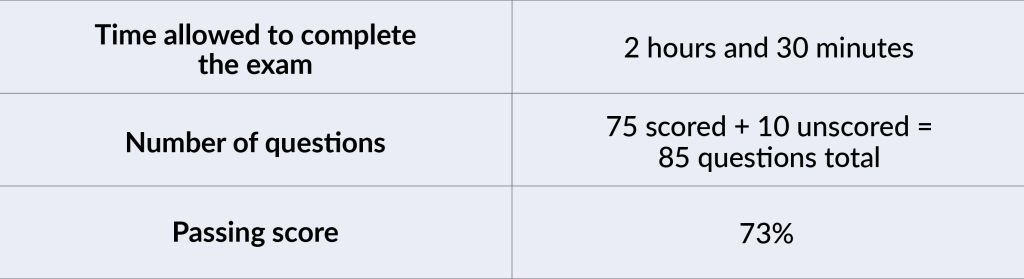

The Series 79 exam consists of 75 scored and 10 un-scored multiple-choice questions covering the three main sections of the FINRA Series 79 content outline. The exam itself is not divided into three sections, so questions from each section appear randomly throughout the exam. The 10 additional un-scored questions are ones that the exam committee is trying out. These are unidentified and are distributed randomly throughout the exam.

Note: Scores are rounded down to the next lowest whole number (e.g. 72.9% would be a final score of 72% – not a passing score for the Series 79 exam).

Topics Covered on the Exam

The questions on the Series 79 exam cover the major job functions of entry-level investment bankers, as determined by FINRA:

FINRA updates its exam questions regularly to reflect the most current rules and regulations. Solomon recommends that you print out the current version of the FINRA Series 79 Content Outline and use it in conjunction with the Solomon Series 79 Study Guide. The Content Outline is subject to change without notice, so make sure you have the most recent version.

The Solomon Exam Prep Series 79 Study Guide introduces you to several different rules instituted by both FINRA and the SEC. While learning about these rules is important, the exam will not ask for specific FINRA rules, so you do not need to memorize those rule numbers. Instead, you should learn and understand the content of those rules. FINRA rules are generally distinguished by having four numbers (i.e., Rule 1250 or Rule 2241).

On the other hand, it is essential that you remember the content, and sometimes the names, of the SEC rules and regulations covered in the Solomon Series 79 Study Guide. In general, SEC rule numbers consist of either (1) three numbers (e.g., Rule 144) or (2) two numbers and a letter, followed by another number or a dash (e.g., Rule 10b-9, or Rule 15c1-3). Also, remember the names of regulations with letters associated with them, such as Regulation A.

Questions on the Series 79 exam do require you to use arithmetic, ratios, and basic algebra. Also, because the Series 79 exam requires you to understand and be able to analyze financial statements, a basic understanding of financial accounting is very helpful.

Question Types on the Exam

The Series 79 exam consists of multiple-choice questions, each with four options. You will see these question structures:

This item type asks a question and gives four possible answers from which to choose.

Which type of SEC filing would you look at to determine the holdings of a large investment manager?

This kind of question has an incomplete sentence followed by four options that present possible conclusions.

If a company were to liquidate all its assets and pay off all its liabilities, the amount that would be left is:

This type requires you to recognize the one choice that is an exception among the four answer choices presented.

All of the following are characteristics of a hedge fund, except:

For this question type, you see a question followed by two or more statements identified by Roman numerals. The four answer choices represent combinations of these statements. You must select the combination that best answers the question.

You are analyzing a public company and your analysis requires you to compile LTM (last 12 months) financial data for the company. Which of the following SEC filings would you typically look to for such data?

This format is also used in items that ask you to rank or order a set of items from highest to lowest (or vice versa), or to place a series of events in the proper sequence.

In marketing a proposed acquisition, a sell-side investment banker typically provides the following materials to prospective buyers in which order?

Answers: A, A, B, D, D

For an even better idea of the possible question types you might encounter on the Series 79 exam, try Solomon Exam Prep’s free Series 79 Sample Quiz.

If taking the test at a test center, you will be given a dry erase pen and whiteboard or a pencil and scratch paper, a basic electronic calculator, and an Exhibits Book. The Exhibits Book may be presented on your computer or as a physical pamphlet. You cannot bring notes, paper, or your own calculator. Phones and watches are not permitted either. Many of the questions will refer to tables or charts in the Exhibits Book, and some questions will require you to perform calculations.

The exam is administered electronically, but the computer format can be tricky. Before the exam, you will be able to take a tutorial on how the electronic system works. You should take the tutorial, since some people find the system awkward to use at first, and you don’t want to use valuable test time dealing with technical issues. There is no scheduled break during the test; you’re allowed to take an unscheduled break, but the clock doesn’t stop.

Due to COVID-19, the Series 79 exam can also be taken online. Candidates must submit an Online Exam Administration Request Form to FINRA. Be sure to review the online system requirements for online testing before submitting the form.

The Series 79 exam has 85 questions to answer in 150 minutes, which is a little under two minutes per question. This means you’ll need to work at an average pace of about 105 seconds per question. Keep in mind that 105 seconds per question is an average speed that you must maintain over two and a half hours. This would be challenging even if every question was short and straightforward. Unfortunately, a number of questions are detailed and time-consuming, and will certainly take more than 105 seconds. You’ll need to work faster on the remaining questions to maintain the necessary pace.

Questions on the Series 79 exam can be intentionally confusing. You should carefully read each question before you answer it and understand exactly what the question is asking. While it is important to make a serious effort on each question, avoid spending a large amount of time on any single question. In general, you should dedicate no more than five minutes to any one question. If you find yourself spending more than five minutes, give it your best guess, flag the question, and move on.

As many of the questions on the Series 79 exam are paragraph length, it is often a good idea to read the last line or two of the question before reading the whole question. This technique will allow you to focus on the aspects of the long-form question that are most relevant, thereby saving you time.

Many test-takers quickly read the question and immediately skip to the answer choices. A better technique is to formulate what you believe is the correct answer before going through the answer choices. If your pre-phrased answer is one of the choices, you should be comfortable in selecting that answer. This technique will also help you increase your speed.

You should always read every answer choice. The exam is full of attractive but incorrect answers. Also, if you notice several correct answers, you may have missed an “except” or “not” in the question. If you consider every answer choice before making your selection, you are less likely to be tricked into picking a wrong but superficially appealing answer.

There is no penalty for guessing. If you honestly don’t know an answer, pick an answer choice and move on. Don’t dawdle. Even a random guess has a 25% chance of being right. If you spend too long trying to narrow down answer choices on one question, you’ve lost precious time on later questions.

If you’re struggling with a question or have no idea what the answer is, mark the question and return to answer it later. Not only does this strategy allow you to efficiently answer the ones you know, but it can also help because you may learn something later in the exam that may help you answer an earlier question. Just remember to save enough time to return to the questions you didn’t answer. However, it is not a good idea to simply skip all of the difficult questions with the intention of answering them later. You should make a serious effort to answer each question before moving on to the next one, as your thoughts are often clearer early on in the exam-taking process than they will be later.

You can pass the FINRA Series 79 Exam! It just takes focus and determination. Solomon Exam Prep is here to support you on your path to becoming a registered investment banking representative.

To explore all Solomon Exam Prep’s Series 79 study materials, including product samples, visit the Solomon website here.

For more helpful securities exam-related content, study tips, industry updates, and promotional offers, join the Solomon email list. Just click the button below:

For a number of securities exams, you should understand the term “tender.” Solomon explains what the term means and how it’s used in the securities industry. Continue reading

When studying for a securities exam such as the FINRA Securities Industry Essentials (SIE) exam and the Series 7, Series 14, Series 24, Series 79, or the MSRB Series 50, Series 52, Series 53, or Series 54, it’s likely you will encounter the word “tender.” This bit of terminology may be confusing at first. But learning the ways “tender” is commonly used in the securities industry will prevent you from getting tripped up when you see it on an exam.

You may have heard this word in connection with stock buybacks. When a company offers to buy its shares back from stockholders, the company is said to be conducting a tender offer. The stockholders who take the company up on the offer are said to be tendering their shares. A company may also make a tender offer to a different company’s shareholders, for example if it wants to acquire the other company.

The word “tender” comes from the field of law. To tender is to make a binding offer to enter into an agreement. (It also has a second meaning of presenting payment, which is why your dollar bill has the phrase “legal tender” on it.) So when you tender a security you own, you are offering to sell it on terms that have been spelled out between you and the other party. In the case of a tender offer, the company must specify these terms when it makes the offer and shareholders must take them or leave them. In many cases, the U.S. Securities and Exchange Commission (SEC) requires that these terms include a window of time during which shareholders who tendered their shares may change their minds. In that case, the “binding offer” is not binding right away.

Another securities-related use of “tender” is when a security gives its owner the right to sell it back to the issuer. Exercising this right is sometimes called tendering the security. For example, a municipal bond might have a tender option that gives the bondholder the right to sell it back to the municipality at a certain time for a certain price. Additionally, some variable-rate municipal securities come with a mandatory tender that is triggered when the rate is adjusted. When this happens, the bondholder must choose between tendering the bond or accepting the new rate.

So if you see the word “tender” on a securities exam, it means that the owner of a security is offering to sell it under specific terms and conditions, and the owner’s ability to back out of the offer may be limited.

Want a curated collection of our most relevant blog posts delivered straight to your email inbox each month? Subscribe to the Solomon Monthly Newsletter and get securities exam study tips, industry news, and more! Just click the button below to join.

What can you do with a Series 66 license? What does the exam cover and how should you prepare for it? Keep reading for answers to your Series 66 questions. Continue reading

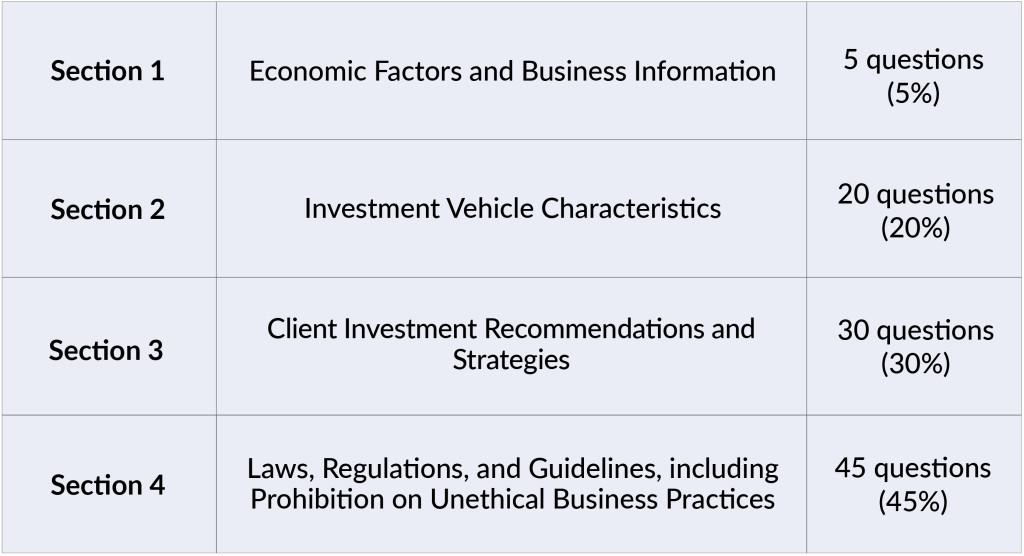

The Series 66, also known as the Uniform Combined State Law Exam, is created by the North American Securities Administrators Association (NASAA), which represents state securities regulators in the United States, Canada, and Mexico. Passing the Series 66 exam is like passing both the Series 63 (Uniform Securities Agent State Law Examination) and the Series 65 (Uniform Investment Adviser Law Examination). However, to register as an investment adviser representative with the Series 66, you must also pass the FINRA Series 7 General Securities Representative exam. In conjunction with the Series 7 license, the Series 66 license qualifies you as both an investment advisor representative and a securities agent.

As an investment adviser representative, an individual can perform the following tasks:

Note that the Series 7 exam is a co-requisite to the Series 66, so you can take the exams in either order. However, Solomon recommends passing the Series 7 before the Series 66 since much of the information tested on the Series 7 is likely to appear on the Series 66 exam.

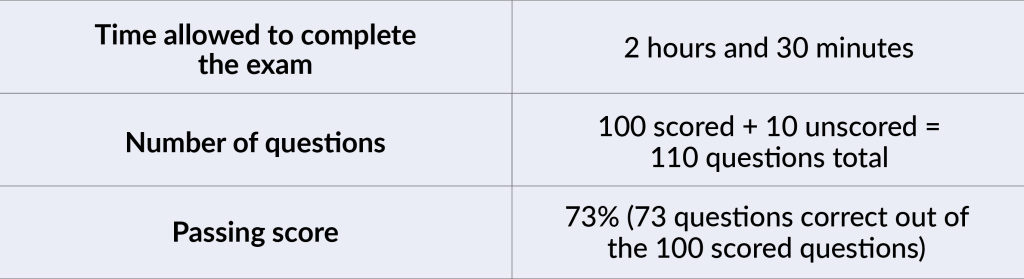

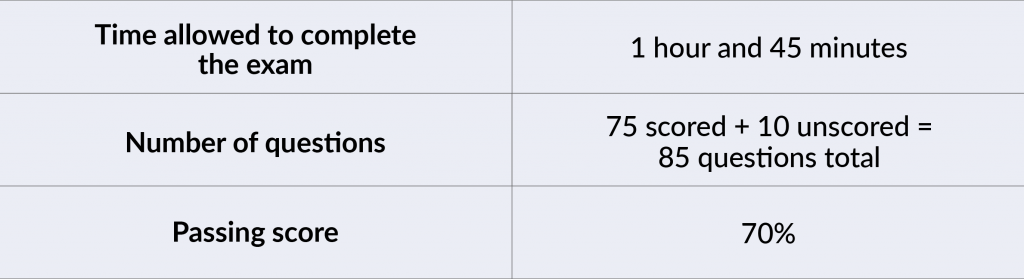

The Series 66 exam consists of 100 scored and 10 unscored multiple-choice questions covering the four sections of the NASAA Series 66 exam outline. The 10 additional unscored questions are ones that the exam committee is trying out. These are unidentified and are distributed randomly throughout the exam. The NASAA updates its exam questions regularly to reflect the most current rules and regulations.

Note: Scores are rounded down to the next lowest whole number (e.g. 72.9% would be a final score of 72% – not a passing score for the Series 66 exam).

Topics Covered on the Exam

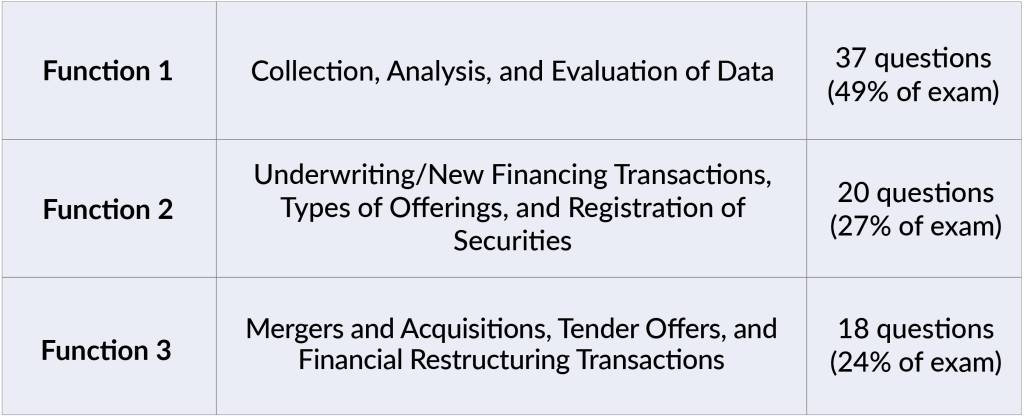

The NASAA divides the Series 66 exam into four sections:

The Series 66 exam covers many topics including the following:

Question Types on the Exam

The Series 66 exam consists of multiple-choice questions, each with four options. You will see these question structures:

This item type asks a question and gives four possible answers from which to choose.

Which of the following is not a current asset?

This kind of question has an incomplete sentence followed by four options that present possible conclusions.

Callable preferred stock is more likely to be called when:

This type requires you to recognize the one choice that is an exception among the four answer choices presented.

An investor calculating the investing merits of a payment or payments not yet received might potentially use all of the following except:

For this question type, you see a question followed by two or more statements identified by Roman numerals. The four answer choices represent combinations of these statements. You must select the combination that best answers the question.

Pick two statements that best represent time-weighted and dollar-weighted returns:

This format is also used in items that ask you to rank or order a set of items from highest to lowest (or vice versa), or to place a series of events in the proper sequence.

Rank the following categories of mutual funds in order of volatility, from highest to lowest.

Answers: D, B, C, B, D

For an even better idea of the possible question types you might encounter on the Series 66 exam, try Solomon Exam Prep’s free Series 66 Sample Quiz.

You can pass the NASAA Series 66 Exam! It just takes focus and determination. Solomon Exam Prep is here to support you on your path to becoming a registered securities agent and investment advisor representative.

To explore all Solomon Exam Prep’s Series 66 study materials, including product samples, visit the Solomon website here.

For more helpful securities exam-related content, study tips, and industry updates, join the Solomon email list. Just click the button below:

Thinking about taking the SIE exam? Keep reading to learn what the SIE is, what topics the exam covers, and how you should prepare for it. Continue reading

Updated June 9, 2022

Are you interested in the world of stocks, bonds, and investments? Thinking about a career as a financial advisor? Or perhaps your goal is to become an investment banker or a hedge fund manager? There are many attractive career options in the securities industry, but no matter which path you’re considering, you’ll probably need to take the Securities Industry Essentials (SIE) Exam.

If you’re not sure whether a career as a securities industry professional is right for you, the SIE is a great way to test the waters. For college students, the SIE provides a broad overview of the securities industry and financial knowledge that will be helpful even if you don’t pursue a securities industry career. And passing the SIE will make you more competitive when looking for a financial or investment-related internship.

For job seekers in general, having the SIE under your belt shows potential employers that you are serious about a career in the industry and have mastered industry fundamentals. And because the SIE is a co-requisite to several securities industry qualification exams, passing it allows you to jumpstart your career goals.

The SIE exam is an introductory-level exam that covers fundamental securities industry knowledge. The SIE focuses on industry terminology, securities products, the structure and function of the markets, regulatory agencies and their functions, and regulated and prohibited practices.

The SIE is a co-requisite of several qualification exams, including the Series 6, Series 7, Series 22, Series 79, Series 82, and Series 99. Passing the SIE does not qualify you to become a registered securities industry professional, but it is usually the first step. Because the SIE is “co-requisite,” instead of “pre-requisite,” you don’t have to take the SIE before taking other FINRA exams. However, taking the SIE first is highly recommended because what you learn on the SIE is extremely helpful to you when you take any other security exam. The knowledge that you learn on the SIE is wind in your sails when you take any other registered representative level securities qualification exam, such as the Series 6 or Series 7.

Any individual 18 or older may take the SIE exam. Unlike other FINRA securities exams, employment and sponsorship by a FINRA member firm is not required in order to take the SIE, and exam results are valid for four years. Individuals can sign up to take the SIE exam on the FINRA website by creating an account, paying the $80 exam fee, and scheduling the exam. The SIE can be taken at a Prometric test center or online via the ProProctor platform.

The SIE exam consists of 75 scored and 10 unscored multiple-choice questions covering the four sections of the FINRA SIE exam outline. The 10 additional unscored questions are ones that the exam committee is trying out. These are unidentified and are distributed randomly throughout the exam. FINRA updates its exam questions regularly to reflect the most current rules and regulations.

Note: Scores are rounded down to the next lowest whole number (e.g. 69.9% would be a final score of 69% – not a passing score for the SIE exam).

Topics Covered on the Exam

FINRA divides the SIE exam into four sections:

The SIE exam covers many topics including the following:

Question Types on the SIE Exam

The SIE exam consists of multiple-choice questions, each with four options. You will see these question structures:

This item type asks a question and gives four possible answers from which to choose.

When interest rates go up, what happens to the price of typical preferred stock?

This kind of question has an incomplete sentence followed by four options that present possible conclusions.

ADRs trade in:

This type requires you to recognize the one choice that is an exception among the four answer choices presented.

All of the following are advantages to the issuer of debt financing over equity financing except:

For this question type, you see a question followed by two or more statements identified by Roman numerals. The four answer choices represent combinations of these statements. You must select the combination that best answers the question.

The prices of which of the following two types of preferred stock are least sensitive to changes in interest rates?

This format is also used in items that ask you to rank or order a set of items from highest to lowest (or vice versa), or to place a series of events in the proper sequence.

Rank the following yields for a premium bond held to maturity from highest to lowest.

For an even better idea of the possible question types you might encounter on the SIE exam, try Solomon Exam Prep’s free SIE Sample Quiz and SIE Sample Exam.

You can pass the FINRA SIE Exam! It just takes focus and determination. Earning this certification will provide valuable knowledge and open up rewarding career opportunities. Solomon Exam Prep is here to support you on your first step to entering the securities industry.

To explore all Solomon Exam Prep’s SIE study materials, including product samples, visit the Solomon website here.

For more helpful securities exam-related content, study tips, and industry updates, join the Solomon email list. Just click the button below: