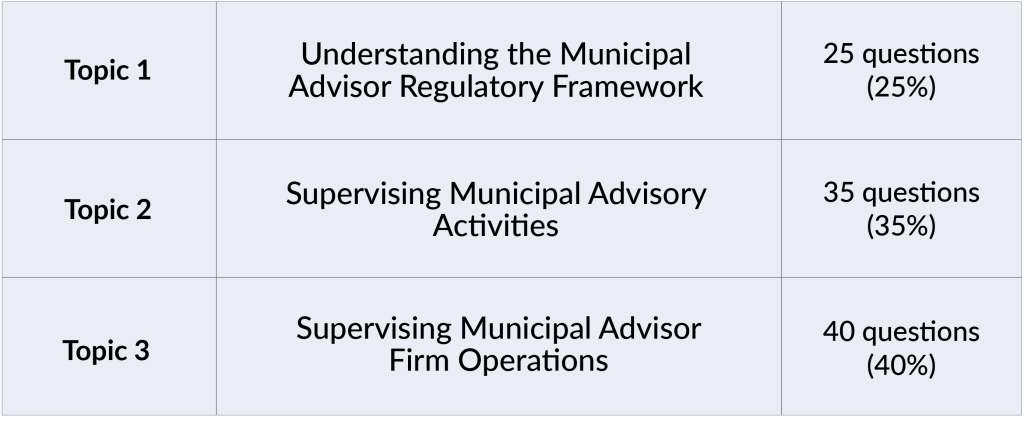

How to Pass the MSRB Series 51 Exam

Considering taking the Series 51 exam? Keep reading to learn what the Series 51 qualifies you to do, what the exam covers, and how you should prepare for it. Continue reading

Considering taking the Series 51 exam? Keep reading to learn what the Series 51 qualifies you to do, what the exam covers, and how you should prepare for it. Continue reading

An audiobook version of the Solomon Exam Prep Series 53 Study Guide is now available for the first time for professionals studying for the MSRB Series 53 exam. Continue reading

The MSRB has proposed several changes to its continuing education requirements to harmonize with FINRA’s new CE requirements. Continue reading

An audiobook version of the Solomon Exam Prep Series 52 Study Guide is now available for the first time for professionals studying for the MSRB Series 52 exam. Continue reading

The MSRB has announced the end of a COVID-related grace period allowing municipal principals to delay taking their qualification exams. Continue reading

Thinking about taking the Series 54 exam? Keep reading to learn what the Series 54 qualifies you to do, what the exam covers, and how you should prepare for it. Continue reading

The new 3rd edition of the Solomon Series 54 Study Guide covers everything you need to know to pass the exam and become a Municipal Advisor Principal. Continue reading

Prometric will no longer require test candidates and test center staff to wear masks at test centers, effective May 1, 2022. Continue reading

The Solomon Series 52 Study Guide, 5th edition, covers everything you need to know to pass the Series 52 Exam and become a Municipal Securities Representative. Continue reading

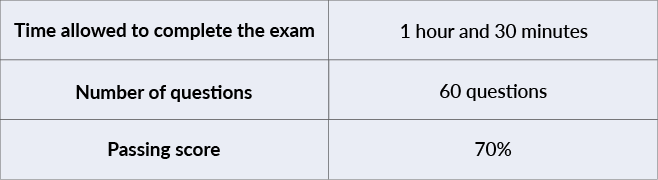

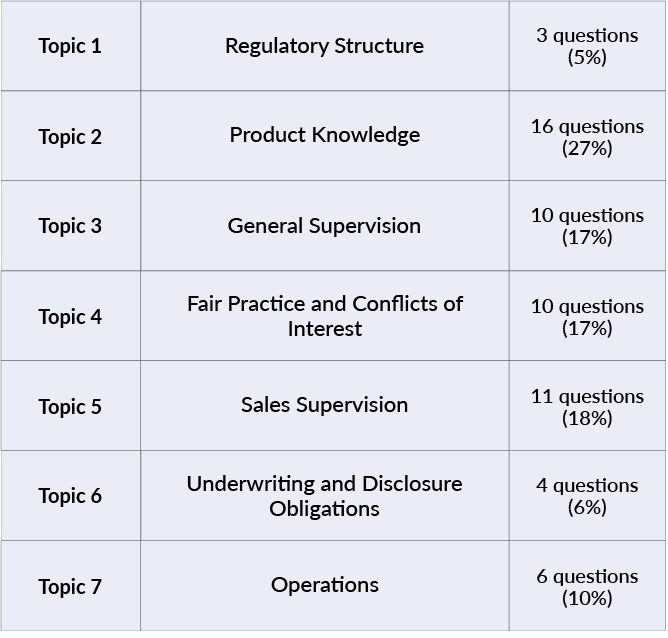

What is the Series 53 exam? Learn what a Series 53 license qualifies you to do, what the exam covers, and how you should prepare for it. Continue reading