If you are studying for the FINRA Series 6 or Series 7 exam, you will need to learn about the different types of retirement plan accounts. A retirement account may be an individual plan that is managed by the participant or the participant’s agent, such as an investment firm or a trust bank. Or it may be employer-sponsored, meaning that it is organized and managed by the participant’s employer.

Private employers of any size and structure, from the largest C corporation to a sole proprietorship consisting of a single self-employed individual, may set up and use an employer-sponsored retirement plan. For small business owners, retirement plans offer significant tax advantages and can help attract employees. Since there are several types of retirement plans available for small businesses, it’s important to understand the features of each option. Three plans commonly chosen by small businesses are solo 401(k) plans, SEP plans, and SIMPLE plans.

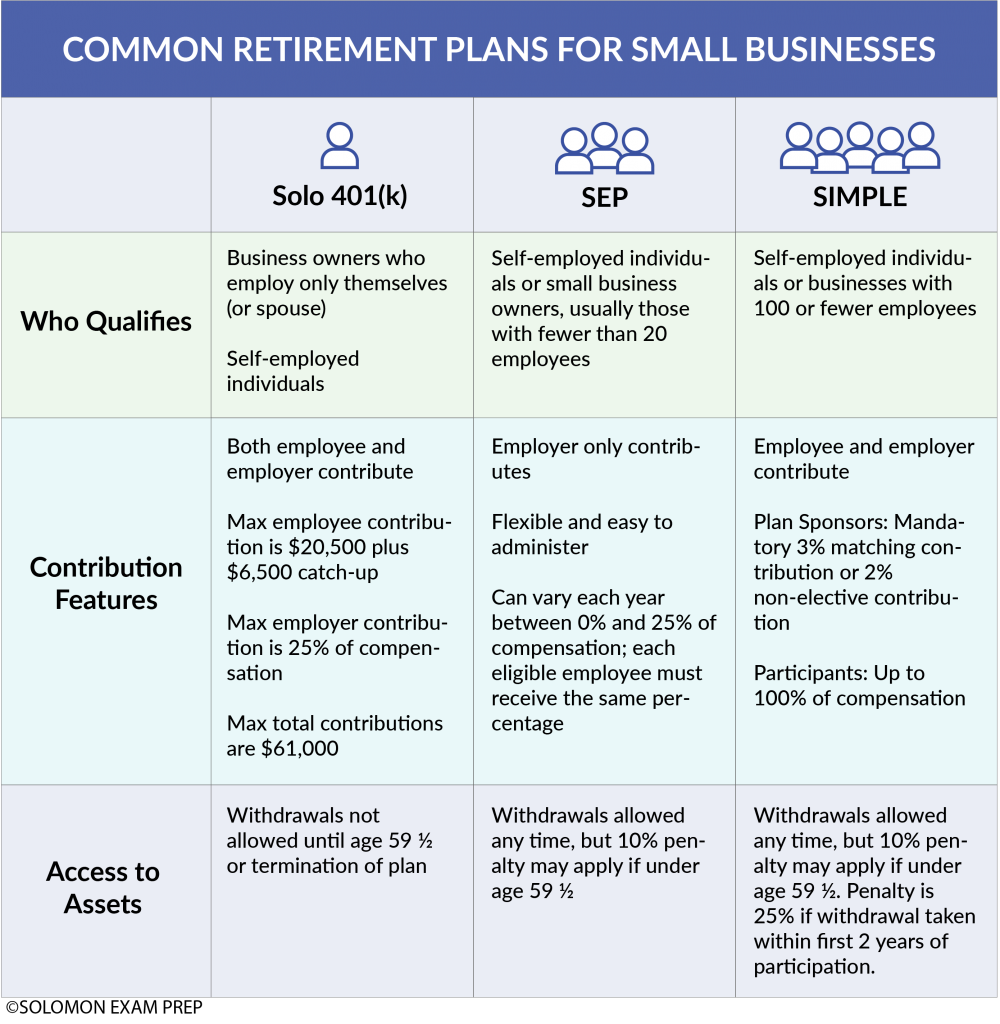

Solo 401(k) Plans

A business owner can open a solo 401(k) if the business does not employ anyone else. The owner of the business creates a 401(k) plan much like any other employer. Then, as an employee, the owner opens a 401(k) account within that plan.

Both employer and employee contributions can be made in a solo 401(k). The maximum employee contribution is the same as for other 401(k)s. As of 2022, this limit is $20,500 per year, with a catch-up contribution of $6,500 for those aged 50 and above. As an employer, the maximum annual contribution is 25% of what the owner pays herself. The combined annual contribution (employee and employer) cannot exceed $61,000.

The business owner is allowed to employ her spouse and still make use of a solo 401(k) plan. The spouse can open their own 401(k) account using the business’s solo 401(k) plan. A solo 401(k) can be created whether the business is set up as a corporation, LLC, or sole proprietorship. Self-employed people who haven’t set up a business can also create a solo 401(k), although their contribution limits are calculated differently.

Unlike most employer-sponsored retirement plans, solo 401(k)s do not need to comply with ERISA (the Employee Retirement Income Security Act). This is a federal law that requires employers to give employees fair access to the employer’s retirement plan. These concerns do not apply when the business has no other employees.

SEP

Simplified Employee Pension (SEP) plans are IRA-based retirement plans for any size business but are usually favored by small businesses. Under this type of plan, the business owner can make pre-tax contributions into IRA accounts set up for eligible employees and also for herself if the owner is self-employed.

The plan allows employers to skip contributions in years when business is bad, but if the owner makes a contribution for herself, she must also make contributions for her employees. When contributions are made, they must be made for all participants who actually performed work during the year for which the contributions are made, including those over 72 years of age (the latter feature is unique to the SEP plan). Contributions for all participants generally must be uniform, for example the same percentage of hourly wage.

The business owner can make contributions of up to 25% of an employee’s salary, or an annual maximum of $61,000, whichever is less. Only the employer, and not the employee, makes contributions to the SEP IRA, but an employee is always 100% vested in his SEP IRA. Generally, the employer can take an income tax deduction for contributions made to each employee’s SEP. SEP contributions are not included on the employee’s W-2 statement for tax purposes. Rules for withdrawal of funds are generally the same as for any other IRA, meaning that withdrawals are subject to income taxes, and early withdrawals are usually subject to a penalty.

SIMPLE

Savings Incentive Match Plan for Employees (SIMPLE) plans are retirement plans for businesses having no more than 100 employees. With a SIMPLE IRA or SIMPLE 401(k), the employee may make pre-tax contributions to the plan. The contribution is expressed as a percentage of the employee’s compensation and is limited to $14,000 a year ($17,000 for employees aged 50 and over). The employer is required to either match these contributions up to 1% to 3% of the employee’s compensation or to contribute 2% whether the employee makes a contribution or not. The employer chooses which type of contribution (and if matching, the maximum percentage it will match). This choice applies to all employees. So an employer who chooses matching contributions is not obligated to contribute 2% to an employee who chooses not to contribute.

Any employee who previously earned at least $5,000 during any two years and is reasonably expected to receive at least $5,000 during the current calendar year is eligible to participate in this plan. Unlike the SEP plan, however, premature SIMPLE IRA distributions (withdrawals of account funds) will incur a 25% penalty in the first two years the account exists if made before age 59 1/2.

While the SEP plan is discretionary, in that the employer can decide when to fund the plan, funding the SIMPLE IRA plan is mandatory, no matter what kind of year the business had. A SIMPLE 401(k) functions similarly to a SIMPLE IRA. Both have the same contribution limits and are 100% vested from the beginning.

Good to know:

SEP and SIMPLE IRAs have characteristics in common with traditional IRAs. For example, contributions are generally made with pre-tax dollars, must be earned income, and must only be in cash. Taxes on contributions and earnings are deferred until withdrawal, as long as withdrawals occur after the age of 59 1/2. Required minimum distributions (RMDs) must begin the year the participant turns age 72, although the participant may choose to delay the first payment until April 1 of the following year. After that, RMDs must be taken by December 31 each year. Funds can be distributed as a lump sum or in periodic payments. If the account owner fails to withdraw an RMD or the full amount of the RMD before the deadline, the amount not withdrawn is taxed at 50%.

Anyone who plans to become a registered representative by passing the Series 6 or Series 7 exam and assist customers with retirement plans must understand the complexity of retirement planning. The Solomon Exam Prep Series 6 Study Guide and Series 7 Study Guide both cover retirement plan accounts so that you can be prepared for questions about this topic on exam day. Visit the Solomon website to explore study materials for 21 different securities exams, including the Series 6 and 7.