SIE Comparison Chart

Need help determining when you should take your exam with the upcoming changes regarding the SIE exam? We made an invaluable chart to help! Continue reading

Need help determining when you should take your exam with the upcoming changes regarding the SIE exam? We made an invaluable chart to help! Continue reading

Submit your answer to info@solomonexamprep.com to be entered to win a $10 Starbucks gift card. Continue reading

Submit your answer to info@solomonexamprep.com to be entered to win a $10 Starbucks gift card.

Congratulations to Elizabeth S., this month’s Study Question of the Month winner!

Question

Relevant to the SIE, Series 7, Series 24, Series 79, and Series 82.

Which of the following would not necessarily be restricted shares when you purchase them?:

A. Shares sold by the CEO of the issuing company

B. Shares sold by the CEO’s wife of the issuing company

C. Shares sold by the assistant to the CEO of the issuing company

D. Shares sold by a major shareholder (more than 10% ownership) of the issuing company

Answer: C.

Securities that are held by control persons are called control securities. A control person, or affiliated person, is an individual in a position to exert direct influence on the actions of an issuer. For example, officers, directors, policy-making executives, major shareholders (generally own 10% or more of outstanding shares), and other people who are in a position to directly or indirectly control the management of the company are considered control persons. This includes spouses, family members who live with them, and other entities such as trusts or corporations affiliated with control persons, as defined in Rule 144. When control securities are sold, they become restricted securities even if they were not restricted securities previously.

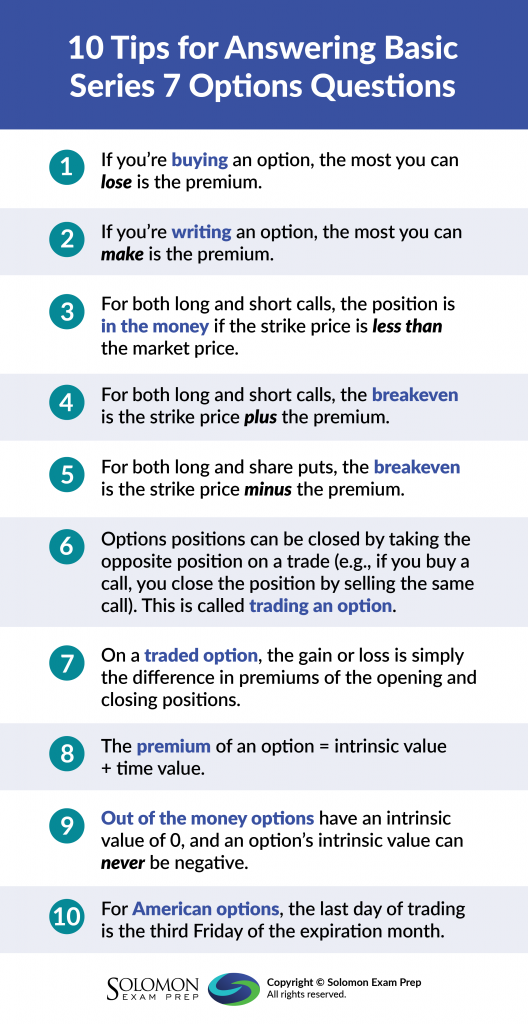

Struggling with options questions on the FINRA Series 7 exam? Here are ten tips to getting basic Series 7 options questions right. Continue reading

Submit your answer to info@solomonexamprep.com to be entered to win a $10 Starbucks gift card. Continue reading

Congratulations to Megan K., this month’s Study Question of the Month winner!

Submit your answer to info@solomonexamprep.com to be entered to win a $10 Starbucks gift card.

Question

Relevant to the Series 6, Series 7, Series 66, and Series 65.

The cost basis for inherited securities is:

A. The same as the deceased person’s cost basis

B. The same as the price of the securities on the date that the original owner dies

C. The same as the price of the securities on the date that the new owner takes possession

D. The lower of the deceased person’s cost basis and the price of the securities when the new owner takes possession

Answer: B.

In the event that the holder of securities dies and passes those securities to one of his heirs, the new owner gets to claim the price of those securities on the deceased person’s date of death as the securities’ new tax basis.

Submit your answer to info@solomonexamprep.com to be entered to win a $10 Starbucks gift card. Continue reading

Congratulations to Terry F., this month’s Study Question of the Month winner!

Submit your answer to info@solomonexamprep.com to be entered to win a $10 Starbucks gift card.

Question

Relevant to the Series 6, Series 7, Series 65, Series 66

Which of the following is true of UGMA/UTMA accounts?

I. Only family members may contribute to a UGMA/UTMA

II. Annual contribution limit of $13,000 per year, per child

III. Assets may only be used for education expenses

IV. Earnings reported under adult custodian’s tax identification

A. I and II

B. III and IV

C. II and III

D. None of the choices listed

Answer: D.

Anyone may contribute to a Uniform Gifts to Minors Act (UGMA) or Uniform Transfer to Minors Act (UTMA) account and there are no contribution limits. Assets in UGMA/UTMA accounts may be used for any purpose and earnings are reported on the minor’s social security account, not the custodian’s.

*Submit your answer to info@solomonexamprep.com to be entered to win a $10 Starbucks gift card.* Continue reading

Congratulations to Veronika J., this month’s Study Question of the Month winner!

***Submit your answer to info@solomonexamprep.com to be entered to win a $10 Starbucks gift card.***

Question (Relevant to the Series 6, Series 7, Series 65, Series 66)

In her junior year in college, Kim’s grandmother dies and leaves Kim several thousand dollars. Kim wants to put some of the money she received from her grandmother into a retirement account. Given Kim’s young age and status as a full-time college student, what would be her best option?

A. Traditional IRA

B. Roth IRA

C. SIMPLE IRA

D. None of the choices listed

Answer: D. You can only contribute earned income to an IRA or tax-deferred retirement plan and so unless Kim has earned income, she cannot contribute to a tax-deferred retirement plan. A SIMPLE IRA, which stands for Savings Incentive Match Plan for Employees, is an employer-sponsored retirement plan and not available to individuals.

***Submit your answer to info@solomonexamprep.com to be entered to win a $10 Starbucks gift card.*** Continue reading

Congratulations to Diane K., this month’s Study Question of the Month winner!

See the answer below!

***Submit your answer to info@solomonexamprep.com to be entered to win a $10 Starbucks gift card.***

Question (Relevant to the Series 7, Series 52, Series 65, Series 66, Series 79)

When the yield curve inverts, that is, when short-term interest rates are higher than long-term interest rates, all of the following are true EXCEPT:

A. It indicates low or no inflation expectations.

B. It indicates higher demand for long-term bonds and lower demand for short-term bonds.

C. It indicates an economic recession.

D. It indicates an economic expansion.

Answer: D. A yield curve plots the yields of similar bonds based on the term of the bond (maturity) and the yield of the bonds, with term on the x-axis and yield on the y-axis. A normal yield curve is upward sloping, indicating that the longer the term of the bond, the higher yield (interest rate). This is because in normal economic conditions, the longer the term of the investment, the greater the risk that interest rates or the economy will change. Thus investors require greater compensation for uncertainties and risks associated with committing their money for longer time periods. This is called the risk premium. When the yield curve is inverted, however, it slopes downward instead of upward. This means that there is higher demand for long-term bonds compared to short-term bonds because investors believe that interest rates will fall in the future. Also, it means that investors are not concerned about inflation. These conditions are associated with a future economic recession.

***Submit your answer to info@solomonexamprep.com to be entered to win a $10 Starbucks gift card.*** Continue reading

Congratulations to Margaret C., this month’s Study Question of the Month winner!

See the answer below!

***Submit your answer to info@solomonexamprep.com to be entered to win a $10 Starbucks gift card.***

Question (Relevant to the Series 6, Series 7, Series 62, Series 65, Series 66, Series 82)

To qualify as a long-term capital gain or loss, stock must be held for more than one year. At purchase, the holding period clock begins:

A. On the trade date

B. One day after the trade date

C. On the settlement date

D. One day after the settlement date

Answer: B. According to the IRS, the holding period clock begins the day after the shares were purchased.

If you’ve ever traded securities or studied for a securities licensing exam, then you’ve probably come across T+3. No, it’s not an herbal supplement or an embarrassing medical procedure. Continue reading

If you’ve ever traded securities or studied for a securities licensing exam, then you’ve probably come across T+3. No, it’s not an herbal supplement or an embarrassing medical procedure. T+3 refers to the regular-way settlement period for most securities transactions. This means that securities must be paid for and delivered by three business days from the trade date. T+3 also means you don’t become the owner of record of a security until three business days after you purchase it.

Well, add T+3 to the list of things that have gone out of style. Effective May 30, 2017, the SEC will shorten the regular-way settlement period to two business days. And so will begin the age of T+2, which is intended to “increase efficiency and reduce risk for market participants,” according to SEC Acting Chairman Michael Pinowar.

This shorter settlement period for the trading of secondary market securities has been discussed by the SEC for years. The change is expected to lower margin requirements for clearing agency members, reduce liquidity stress when markets are volatile, and harmonize settlement with European markets, which moved to T+2 in 2014.

This settlement period will not apply to every securities transaction, though. T+2, like T+3 before it, will apply to:

The securities industry moves fast. Don’t get left behind! Visit www.solomonexamprep.com or call us at 503-601-0212 for more information about the latest securities exam preparation and education.

Solomon has helped thousands pass their Series 6, Series 7, Series 24, Series 26, Series 27, Series 28, Series 50, Series 51, Series 52, Series 53, Series 62, Series 63, Series 65, Series 66, Series 79, Series 82, and Series 99.

The Department of Labor’s fiduciary rule has been subject to more back and forth than an Olympic table tennis match. Will it go into effect? Will it be repealed? Or will it merely be delayed? The answer seems to change from day to day. Continue reading

Update: On March 1, 2017, the Department of Labor proposed a 60-day delay of implementation of the fiduciary rule. The DOL will allow a 15-day comment period before determining whether to finalize the delay.

***

The Department of Labor’s fiduciary rule has been subject to more back and forth than an Olympic table tennis match. Will it go into effect? Will it be repealed? Or will it merely be delayed? The answer seems to change from day to day. While some groups work toward implementation of the rule, other groups fight against it, questioning whether the Department of Labor even has the authority to issue such a rule.

The fiduciary rule would require financial professionals to put an investor’s interests first—that is, to meet a fiduciary duty—when providing investment advice regarding covered retirement plans.

Let’s look at a brief timeline of the life of the fiduciary rule so far:

February 23, 2015: President Obama called for the Department of Labor to move forward with the creation of rules to limit conflicts of interest regarding investor retirement accounts.

April 14, 2016: The Department of Labor proposed the fiduciary rule, intended to begin implementation on April 10, 2017.

February 3, 2017: President Trump issues an executive order directing the DOL to review the fiduciary rule.

February 8, 2017: A federal district court judge in Texas upheld the Department of Labor’s authority to issue the fiduciary rule.

February 17, 2017: A federal district court judge in Kansas upheld the Department of Labor’s authority to issue the fiduciary rule.

When President Trump issued his executive order, he ordered the Secretary of Labor to provide an “economic and legal analysis” of the rule to answer the following questions:

If the Secretary of Labor determines that the answer to any of these questions is yes, it must revise or rescind the rule.

However, many firms are proceeding with their plans to implement the fiduciary rule whether or not the rule as it now exists goes into effect. For example, Merrill Lynch has said it will no longer offer commission-based brokerage IRA accounts. Instead, the firm will offer level fee investment advisory services regardless of the outcome of the fiduciary rule.

Senator Elizabeth Warren of Massachusetts reached out to over thirty leading finance companies, and the overall response from the companies that responded was that they support the fiduciary rule and are prepared to implement it. For example, TIAA wrote, “Putting our clients’ best interests first is a core value at TIAA and, accordingly, we support a best-interest standard,” and Fidelity noted that the firm is “fully prepared to comply with the rule if and when it becomes applicable.”

So even though we don’t know what will be the ultimate fate of the DOL fiduciary rule, it’s safe to say that it has already begun to change the face of the financial industry.

For more information about the DOL fiduciary rule, see our earlier blogpost: https://solomonexamprep.com/news/finra/ready-or-not-here-it-comes-the-dol-fiduciary-rule-2/.