Securities Exam Score Survey Results Are In

Do you think FINRA should provide exam scores to those who pass their qualification exams? Keep reading to learn the results of the Solomon survey. Continue reading

Do you think FINRA should provide exam scores to those who pass their qualification exams? Keep reading to learn the results of the Solomon survey. Continue reading

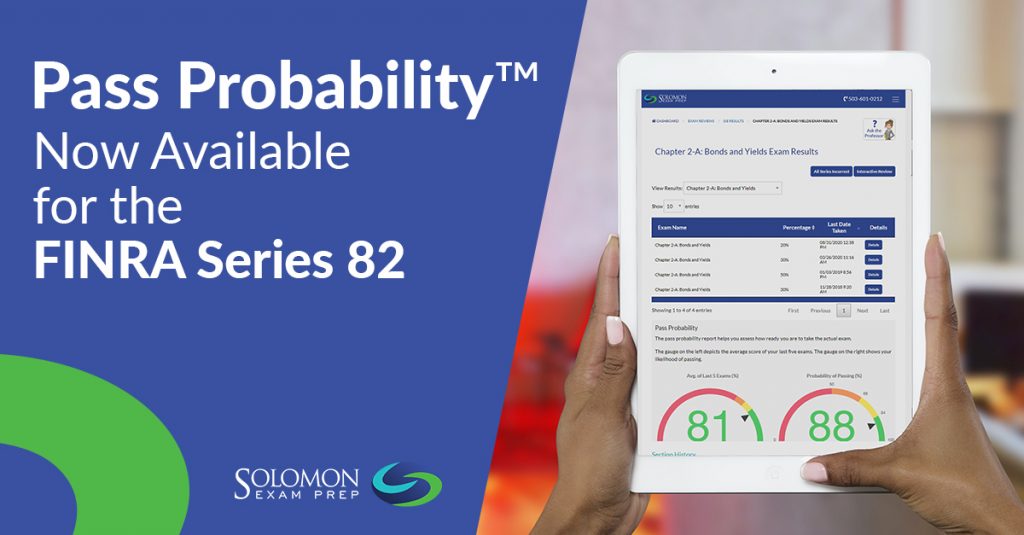

Everyone would like to feel confident when they take their securities exam, but how do you know if you’re ready for test day? Solomon Exam Prep can help – with Pass Probability™. Continue reading

The Series 14 is one of the more difficult FINRA exams, so it’s a good idea to be well-prepared going into test day – Solomon Exam Prep can help! Continue reading

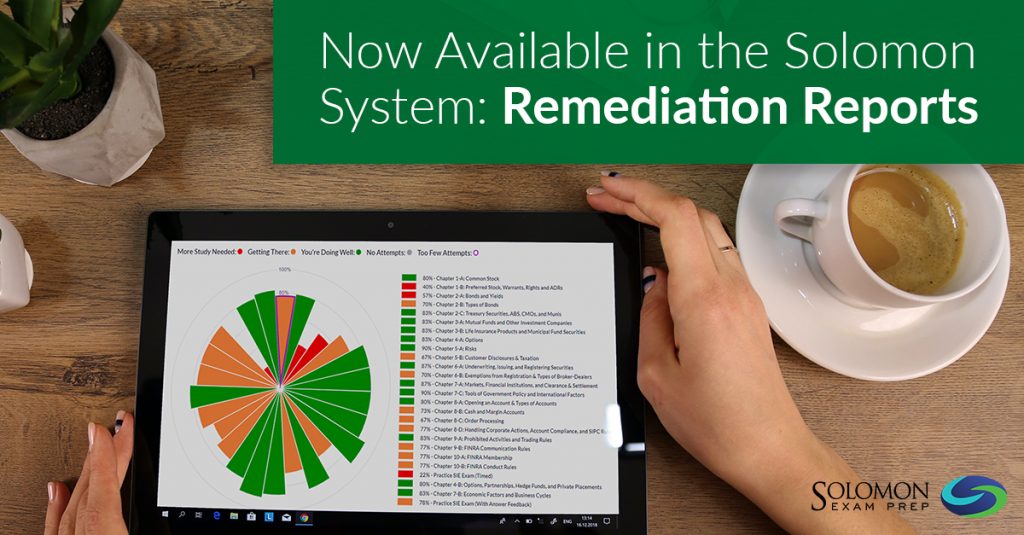

Learn about the Solomon Remediation Report, a new analytical feature designed to help students pass their securities licensing exams the first time. Continue reading

Solomon Exam Prep is delighted to announce an advanced analytical feature called a Remediation Report. The Solomon system analyzes a student’s five most recent practice exams and determines whether a student is ready to take his or her exam. If Solomon AI determines that a student is not ready to sit for their exam, then it creates an individual report with personalized guidance on how to remediate and prepare to pass. This custom Remediation Report is sent to the Solomon student’s email inbox.

The Solomon Remediation Report is connected to the Solomon Pass Probability tool, the industry-leading measure of a security exam prep student’s readiness to pass an exam. Solomon Pass Probability is based on thousands of student data points. Once a Solomon student has taken at least five practice exams, the Solomon Pass Probability feature is activated, and the Pass Probability metric is available in the student’s dashboard. The Solomon Remediation Report provides an additional level of customized study support by helping students focus their efforts and remediate before they sit for their exam.

Solomon Pass Probability and Remediation Reports are currently available for the following exams: SIE, Series 6, Series 7, Series 63, Series 65, Series 66, Series 79, and Series 82.

To learn about all the features of the Solomon Exam Prep learning system, watch the video overview.

Watch the latest Solomon Exam Prep video for a complete look at the Solomon learning system and what it offers students and firms. Continue reading

Solomon Exam Prep has helped thousands of financial professionals pass their FINRA, NASAA, MSRB, and NFA licensing exams. Watch the video for a complete look at the Solomon learning system and what it offers students and firms.

To explore Solomon Exam Prep study materials for 21 different securities licensing exams, including the SIE and the Series 3, 6, 7, 14, 22, 24, 26, 27, 28, 50, 51, 52, 53, 54, 63, 65, 66, 79, 82, and 99, visit the Solomon website.

For many when choosing bonds the most important factor is the tax implications. Knowing the after-tax yield and tax-equivalent yield calculations is critical. Continue reading

Bonds can be nice, reliable investments. Pay some money to an issuing company or municipality, receive interest payments twice a year, and then get all of your original investment back sometime down the road. Sounds like a plan.

But which bonds are best for a specific investor? There are many factors for bond investors to consider when choosing which bond to buy, but for many the most important is the tax implications of investing in one bond instead of another. This concern is most prominent when an investor compares a corporate bond to a municipal bond. For reference, a corporate bond is one issued by a corporation or business, while a municipal bond is one issued by a state, city, or municipal agency.

Comparing the tax implications of these bonds is important because the interest payments that investors receive from municipal bonds are typically not taxed at the federal level. Conversely, interest payments on all corporate bonds are subject to federal taxation. This means that someone in the 32% tax bracket will have to give Uncle Sam 32% of his interest received from a corporate bond, while he will not give up any of his interest received from a municipal bond. Additionally, an investor does not pay state taxes on municipal bond interest if the bond is issued in the state in which the investor lives. Corporate bond interest, on the other hand, is always subject to state tax.

For these reasons, when comparing a corporate bond to a municipal bond, understanding the after-tax yield and the tax-equivalent or corporate-equivalent yield is essential. This is true both for investors and for those who will be taking many of the FINRA, NASAA, and MSRB exams. So let’s look at how to calculate those yields.

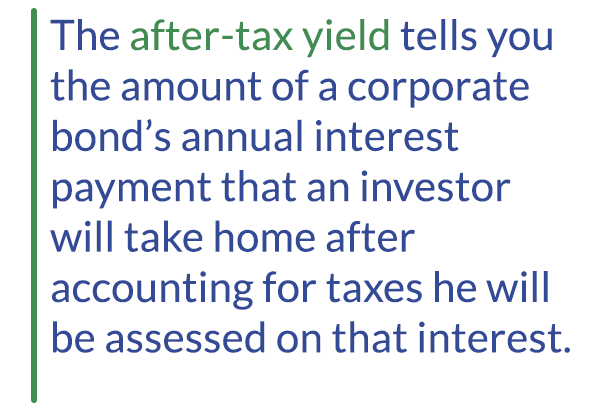

Fir st the after-tax yield. The after-tax yield tells you the amount of a corporate bond’s annual interest payment that an investor will take home after accounting for taxes he will be assessed on that interest. Once that amount is known, the investor can compare it to the yield he would receive from a specific municipal bond and see which potential investment would put more money in his pocket. When calculating the after-tax yield, start with the annual interest percentage (a.k.a. coupon percentage) of the corporate bond, which represents the percent of the bond’s par value that an investor receives each year in interest. For instance, a corporate bond that has a $1,000 par value and an interest rate of 8% will pay an investor $80 dollars in annual interest ($1,000 x 0.08 = $80). You then multiply the coupon percentage by 1 minus the taxes an investor will pay on the corporate bond that he will not pay on the municipal bond that he is considering.

st the after-tax yield. The after-tax yield tells you the amount of a corporate bond’s annual interest payment that an investor will take home after accounting for taxes he will be assessed on that interest. Once that amount is known, the investor can compare it to the yield he would receive from a specific municipal bond and see which potential investment would put more money in his pocket. When calculating the after-tax yield, start with the annual interest percentage (a.k.a. coupon percentage) of the corporate bond, which represents the percent of the bond’s par value that an investor receives each year in interest. For instance, a corporate bond that has a $1,000 par value and an interest rate of 8% will pay an investor $80 dollars in annual interest ($1,000 x 0.08 = $80). You then multiply the coupon percentage by 1 minus the taxes an investor will pay on the corporate bond that he will not pay on the municipal bond that he is considering.

This is where it sometimes gets tricky. What taxes will an investor not pay when investing in a municipal bond that he will pay when investing in a corporate bond? Remember that for just about all municipal bonds, investors do not pay federal tax on interest received.

The formula for after tax yield is:

After-tax yield = Corporate Bond Annual Interest Rate x

( 1 – Taxes Investor Does Not Pay By Investing in Municipal Bond)

On the other hand, an investor always pays federal taxes on interest received from a corporate bond. Additionally, an investor does not pay state taxes on interest payments from a municipal bond issued in the state in which the investor lives.

On the other hand, an investor always pays state taxes on interest received from corporate bonds. So if you see an exam question in which you need to calculate the after-tax yield of a corporate bond to compare it the yield on a municipal bond, you will always subtract the investor’s federal income tax rate from 1 in the equation. You will also subtract the investor’s state tax rate from 1 if the municipal bond is issued in the investor’s state of residence.

Seems simple, right? Here’s a question to provide context:

Marilyn is a resident of Kentucky. She is considering a bond issued by XYZ Corporation. The bond comes with a 7% annual interest rate. Marilyn is also interested in purchasing municipal bonds issued in Ohio. If Marilyn has a federal tax rate of 28% and Kentucky’s state tax rate is 4%, what is the after-tax yield on XYZ’s bond?

To answer this question, begin with the interest rate on the XYZ bond, which is 7%. Then subtract from 1 the taxes Marilyn will not pay if she invests in the municipal bond in question. She will not pay federal taxes on the municipal bond interest, so you would subtract 28%, or .28. However, because Marilyn is a resident of Kentucky and the municipal bonds she is considering are issued in Ohio, she will pay state taxes on the bond. That means you would not subtract her state tax rate (0.04) from 1. After subtracting .28 from 1 to get 0.72, you multiply that amount by the 7% coupon payment. Doing so gives you a value of 5.04 (7 x 0.72 = 5.04%). This means that the interest amount she would take home from the XYZ bond would be equivalent to what she would receive from a municipal bond issued in Ohio that has a 5.04% interest payment. If she can get a bond issued in Ohio that has a higher interest payment than 5.04%, she would take home more money in annual interest payments than she would from the XYZ bond.

The second approach an investor can take to compare how a potential bond investment will be affected by taxation is to calculate the tax-equivalent yield (TEY). This calculation is also known as the corporate-equivalent yield (CEY). The TEY/CEY measures the yield that a corporate bond will have to pay to be equivalent to a given municipal bond after accounting for taxes due. To calculate this yield, you take the annual interest of the given municipal bond and divide it by 1 minus the taxes the investor will not pay if she invests in the municipal bond that she would pay if she invested in a corporate bond.

The second approach an investor can take to compare how a potential bond investment will be affected by taxation is to calculate the tax-equivalent yield (TEY). This calculation is also known as the corporate-equivalent yield (CEY). The TEY/CEY measures the yield that a corporate bond will have to pay to be equivalent to a given municipal bond after accounting for taxes due. To calculate this yield, you take the annual interest of the given municipal bond and divide it by 1 minus the taxes the investor will not pay if she invests in the municipal bond that she would pay if she invested in a corporate bond.

Here’s the formula for tax-equivalent yield:

Tax-equivalent yield = Municipal Bond Annual Interest Rate /

(1 – Taxes Investor Does Not Pay By Investing in Municipal Bond)

When determining what tax rates to subtract from 1 in the denominator, the same principal as described above applies. That is, the investor will not have to pay federal tax on the municipal bond, so her federal rate is always subtracted from 1. The investor will also not have to pay state tax on the bond if it is issued in the state in which she lives. If that is the case, the investor’s state tax rate should also be subtracted from 1. However, if the investor lives in a different state than the state in which the bond is issued, she will have to pay state taxes on the interest payments. In that case, her state tax rate would not be subtracted from 1.

Here’s another question to provide context.

Franz, a resident of Michigan, has purchased a Michigan municipal bond that pays 4% annual interest. If his federal tax bracket is 30% and the Michigan state tax rate is 4%, what interest rate would he need to receive on a corporate bond to have a comparable rate after accounting for taxes owed?

To answer this question, begin with the interest rate on the Michigan municipal bond, which is 4%. Then subtract from 1 the taxes that Franz will not pay on that bond that he would pay if he invested in a corporate bond. He wouldn’t pay federal taxes on the municipal bond interest, so you would subtract 0.30 from 1. Additionally, since the bond is issued in Michigan and he is a Michigan resident, Franz will not pay state taxes on the bond. So you subtract Michigan’s state tax rate of 4%, or 0.04, from 1 as well. After subtracting 0.30 and 0.04 from 1 to get 0.66, you divide that number into the 4% municipal bond annual interest. Doing so gives a value of 6.06 (4 / 0.66 = 6.06). This means Franz would need to find a corporate bond that pays 6.06% in annual interest to match the amount of interest he will take home annually from the Michigan municipal bond after accounting for taxes.

Many people are confused by the concepts of the after-tax and tax-equivalent yields. But you don’t have to be one of them. Just follow this simple approach and any questions you see on this topic will not be overly taxing.

Mastering these equations will help you succeed in passing the Series 6, Series 7, Series 50, Series 52, Series 65, Series 66, and Series 82.

Business icons © MacroOne. Bigstockphoto.com

Meet the newest addition to Solomon Exam Prep’s lineup of free Sample Quizzes: the SIE Sample Exam! Visit the Solomon website to try it out. Continue reading

Meet the newest addition to Solomon Exam Prep’s lineup of free Sample Quizzes: the SIE Sample Exam! Like all Solomon Sample Quizzes, the SIE Sample Exam features questions from our industry-leading Online Exam Simulator. Questions are written by Solomon content experts, who are experienced in both investment education and the process of adult learning.

But unlike other Solomon Sample Quizzes, the SIE Sample Exam is a FULL exam – it contains 75 questions, just like the real FINRA SIE exam – giving you an even better idea of what the actual exam is like. You will encounter easy, medium, and difficult questions so that you can more easily gauge your current knowledge of SIE content.

All Solomon Sample Quizzes and Exams also provide instant feedback for each answer, with a full rationale to help you understand the WHY behind the what. Plus, you get a report at the end detailing your results and giving you the opportunity to review all the questions.

Visit the Solomon website here to try out the SIE Sample Exam and explore free samples of quizzes for 21 different exams.

This month’s study question from the Solomon Exam Prep Online Exam Simulator question database is now available. Continue reading

This month’s study question from the Solomon Online Exam Simulator question database is now available.

*** Comment below or submit your answer to info@solomonexamprep.com to be entered to win a $20 Starbucks gift card.***

This question is relevant to the SIE and the Series 7, 14, 50, 52, and 54.

Question: A Municipal Finance Professional (MFP) hosted a $500 plate fundraiser for a governmental issuer. Does this event trigger a ban on business for two years?

A. Yes, it will trigger a ban because an MFP may not host a fundraiser.

B. Yes, it will trigger a ban because the cost per plate is above the de minimis amount.

C. No, it will not trigger a ban because the MFP did not contribute money, only time and space.

D. No, it will not trigger a ban because the MFP was holding the fundraiser, not the municipal dealer.

Correct Answer: A

Explanation: MFPs are not permitted to solicit funds for municipal issuers or their officials without triggering a two-year ban on business for their firm. Thus, holding fundraisers is not allowed. Municipal dealers are also forbidden from holding fundraisers.

To explore free samples of Solomon Exam Prep’s industry-leading online exam simulators for the SIE, Series 7, Series 14, Series 50, Series 52, Series 54, and other FINRA, MSRB, NASAA, and NFA exams, visit the Solomon website here.

The Internal Revenue Service announced April 1 that it was approving a third accounting method called TYPO. Continue reading

The Internal Revenue Service announced April 1 that it was approving a third accounting method called TYPO. This new method will join LIFO and FIFO as a government-approved way to manage and calculate the cost of inventory.

LIFO stands for “last in first out,” with the most recent (last) unit considered sold first. FIFO stands for “first in first out,” with the oldest (first) unit considered sold first.

The IRS announcement did not state what TYPO stands for or how it works.

Observers were surprised and confused. “Are you sure that’s not a mistake?” was the reaction from Deb It, spokesperson for the American Society of Accountants.

Read Solomon Exam Prep’s expert guide for answering state registration questions on the Series 63, Series 65, and Series 66 exams. Continue reading

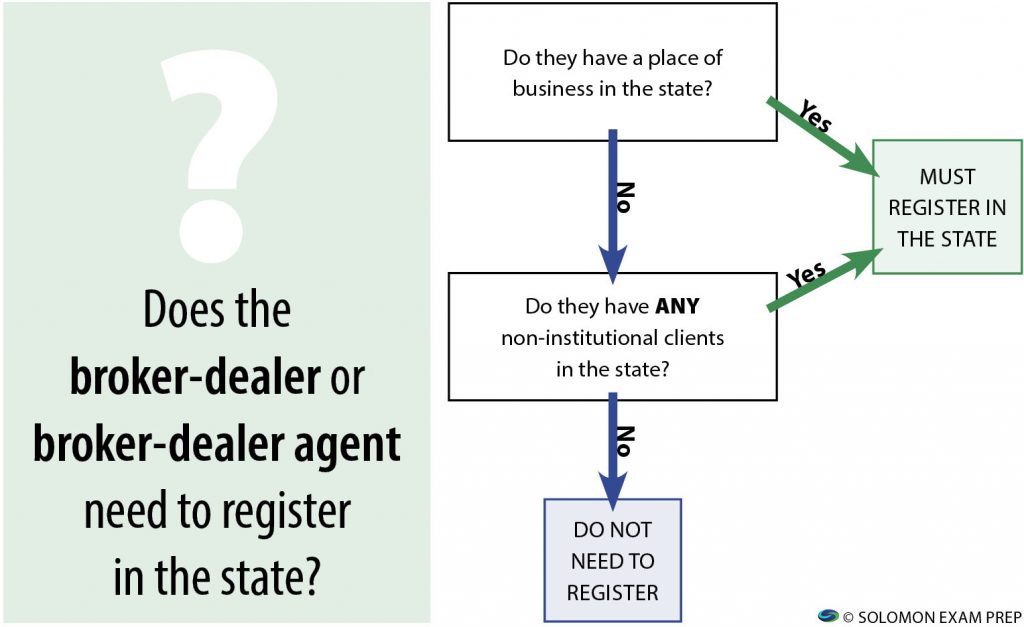

If you’re planning to take the NASAA Series 63, Series 65, or Series 66 exam, you can expect to see questions about when broker-dealers and their securities agents need to register in a particular state. You can also expect to see questions about when investment advisers and investment adviser representatives need to register in a state. Instead of feeling intimidated when confronted with such questions, you should relax, smile, and feel confident. That’s because if you follow the simple rules that we’re about to describe, you should get each of these questions right.

First let’s deal with questions about state registration for broker-dealers (BDs) and their agents. Rule number one here is that when a U.S.-based BD or one of its agents has an office located in a state, that BD or agent must register in the state. It does not matter which types of clients a BD or BD agent with an office in a state has or what types of securities those clients buy from the BD or agent. A BD or agent with an office in a state must register in that state. Period.

What about a BD or BD agent that doesn’t have an office in a state? If a BD or BD agent without an office in a state has any non-institutional clients in that state, the BD or agent must register there. However, if the BD or agent without an office in a state has only institutional clients in the state, no registration in that state is required. Institutional clients include the issuers of securities involved in a specific transaction; other broker-dealers; and institutional buyers, which are big-money entities such as banks, insurance companies, mutual funds, and pension and profit-sharing plans.

So when presented with a question about whether a specific broker-dealer or one of its agents must register in a given state or states, there are two potential questions to ask yourself. The first question is: “Does the broker-dealer or BD agent have an office in the state?” If the answer is yes, it’s simple: the BD or agent must register in that state. End of questions. However, if the answer is no, move on to the second question: “Does the BD or BD agent have any non-institutional clients in the state?” If the answer is yes, the BD or agent must register in the state; if the answer is no, they do not need to register in the state.

Here’s a flowchart to help you remember the question-answering process:

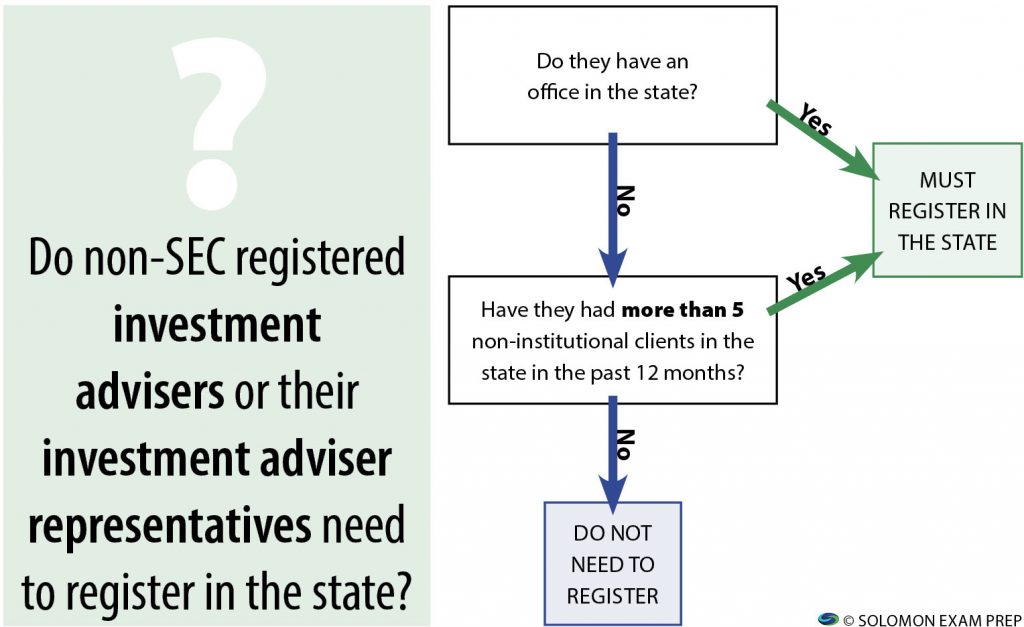

Now let’s look at the state registration requirements for investment advisers that do not register with the SEC. If the investment adviser has an office in the state, it must register there. If the investment adviser doesn’t have an office in the state but has had more than five non-institutional clients in the state during the past twelve months, it also must register there. The rules are the same for investment adviser representatives who work for an investment adviser that does not register with the SEC.

Investment adviser representatives who work for investment advisers that register with the SEC — also known as federal covered advisors — may need to register with the state if they have an office in the state.

So if you see a question about state registration requirements for non-SEC registered investment advisers or their investment adviser representatives, the first question to ask yourself is: “Does the IA or IAR have an office in the state?” If the answer is yes, you know the IA or IAR must register there. If the answer is no, move on to the second question: “Has the IA or IAR had more than five non-institutional clients in the state during the preceding twelve months?” If the answer is yes, they must register in the state; if the answer is no, they don’t need to register in the state.

Here’s another flowchart to help you with this type of question:

Remember that if an investment adviser registers with the SEC, it is a federal covered adviser and does not need to register in any state. Instead, a federal covered adviser must notice file to provide investment advice to residents of that state. When it comes to notice filing requirements for federal covered advisers, follow the same thought process as that described above. If the federal covered adviser has an office in a state, it must notice file there. If it has no office in the state but it has had more than five non-institutional clients in the state in the past twelve months, the firm must also notice file there.

Simple, right? So let’s put the suggested thought process into practice by looking at a question like one you may see on your exam.

XYZ Broker Dealer has its main office in State A. It also has offices in States B and C. XYZ has non-institutional clients in states A and B, but it only has institutional clients in State C. It does not have an office in State D, but it has three non-institutional clients there. In which states does XYZ need to register?

A. State A only

B. States A and B only

C. States A, B, and C only

D. States A, B, C, and D

Remember the process to follow when you see questions about where a BD must register. There are two possible questions to address as part of that process.

First question: Does the broker-dealer have an office in a state? Answer: XYZ has offices in each of States A, B, and C. Recall that if the answer the first question is “yes, the BD has an office in the state”, then the BD must register in that state. So XYZ needs to register in States A, B, and C.

If the answer to the first question is no, as it is for State D, you move on to the second question: Does the BD have any non-institutional clients in the state? XYZ has non-institutional clients in State D, so the answer is yes to that question. If the answer to the second question is yes, this means the BD must register in the state. Thus, XYZ has to register in State D as well as States A, B, and C. So Choice D is the correct answer.

So now you’re an expert, and you’re one step closer to passing your Series 63, Series 65, or Series 66 exam!

Watch a video version of “How to Answer State Registration Questions on the Series 63, Series 65, and Series 66” on the Solomon YouTube channel, where you’ll find even more exam and study tips!

Solomon Exam Prep has helped thousands pass their securities licensing exams, including the SIE and the Series 3, 6, 7, 14, 22, 24, 26, 27, 28, 50, 51, 52, 53, 54, 63, 65, 66, 79, 82 and 99.