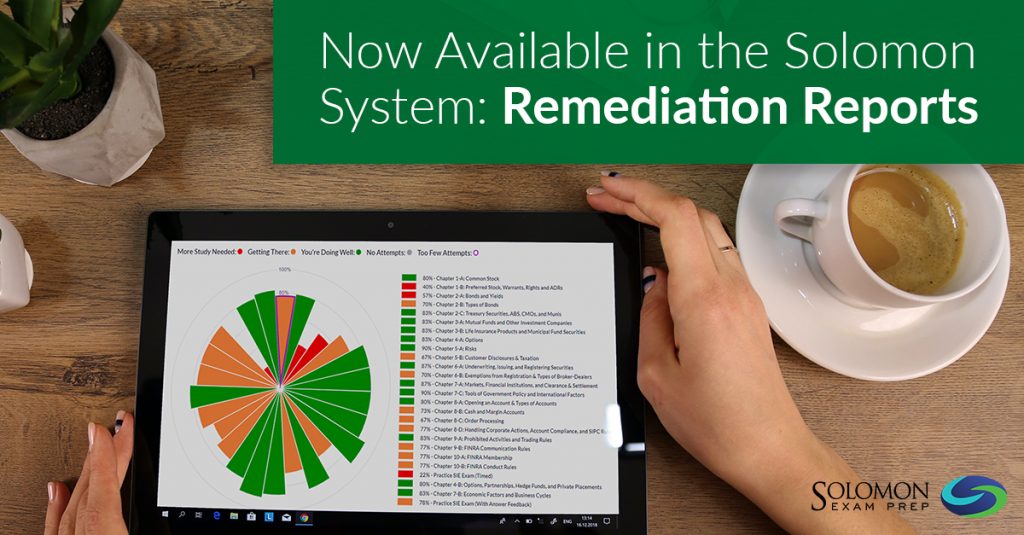

Learn about the Solomon Remediation Report, a new analytical feature designed to help students pass their securities licensing exams the first time. Continue reading

Solomon Exam Prep is delighted to announce an advanced analytical feature called a Remediation Report. The Solomon system analyzes a student’s five most recent practice exams and determines whether a student is ready to take his or her exam. If Solomon AI determines that a student is not ready to sit for their exam, then it creates an individual report with personalized guidance on how to remediate and prepare to pass. This custom Remediation Report is sent to the Solomon student’s email inbox.

The Solomon Remediation Report is connected to the Solomon Pass Probability tool, the industry-leading measure of a security exam prep student’s readiness to pass an exam. Solomon Pass Probability is based on thousands of student data points. Once a Solomon student has taken at least five practice exams, the Solomon Pass Probability feature is activated, and the Pass Probability metric is available in the student’s dashboard. The Solomon Remediation Report provides an additional level of customized study support by helping students focus their efforts and remediate before they sit for their exam.

Watch the latest Solomon Exam Prep video for a complete look at the Solomon learning system and what it offers students and firms. Continue reading

Solomon Exam Prep has helped thousands of financial professionals pass their FINRA, NASAA, MSRB, and NFA licensing exams. Watch the video for a complete look at the Solomon learning system and what it offers students and firms.

To explore Solomon Exam Prep study materials for 21 different securities licensing exams, including the SIE and the Series 3, 6, 7, 14, 22, 24, 26, 27, 28, 50, 51, 52, 53, 54, 63, 65, 66, 79, 82, and 99, visit the Solomon website.

For many when choosing bonds the most important factor is the tax implications. Knowing the after-tax yield and tax-equivalent yield calculations is critical. Continue reading

Bonds can be nice, reliable investments. Pay some money to an issuing company or municipality, receive interest payments twice a year, and then get all of your original investment back sometime down the road. Sounds like a plan.

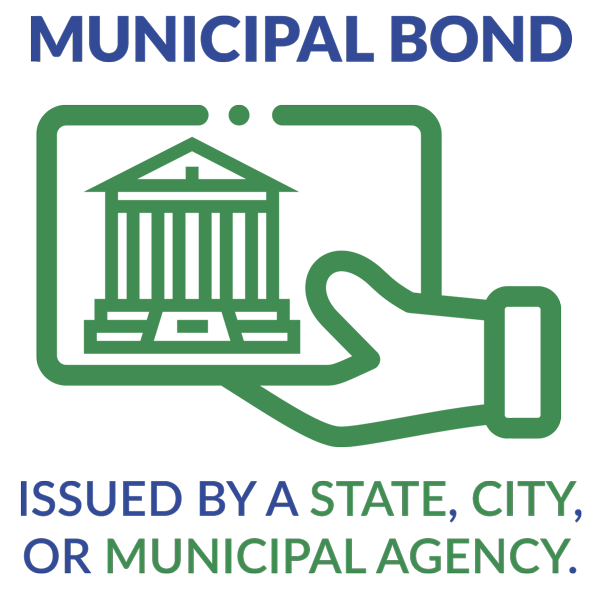

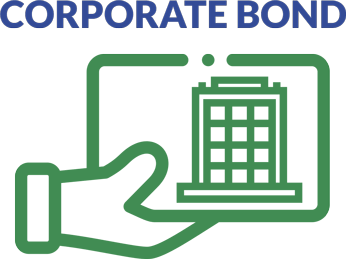

But which bonds are best for a specific investor? There are many factors for bond investors to consider when choosing which bond to buy, but for many the most important is the tax implications of investing in one bond instead of another. This concern is most prominent when an investor compares a corporate bond to a municipal bond. For reference, a corporate bond is one issued by a corporation or business, while a municipal bond is one issued by a state, city, or municipal agency.

Comparing the tax implications of these bonds is important because the interest payments that investors receive from municipal bonds are typically not taxed at the federal level. Conversely, interest payments on all corporate bonds are subject to federal taxation. This means that someone in the 32% tax bracket will have to give Uncle Sam 32% of his interest received from a corporate bond, while he will not give up any of his interest received from a municipal bond. Additionally, an investor does not pay state taxes on municipal bond interest if the bond is issued in the state in which the investor lives. Corporate bond interest, on the other hand, is always subject to state tax.

interest payments taxed federally

interest payments subject to state tax

interest payments not federally taxed

interest payments not taxed by state if issued in state local to investor

For these reasons, when comparing a corporate bond to a municipal bond, understanding the after-tax yield and the tax-equivalent or corporate-equivalent yield is essential. This is true both for investors and for those who will be taking many of the FINRA, NASAA, and MSRB exams. So let’s look at how to calculate those yields.

After-Tax Yield

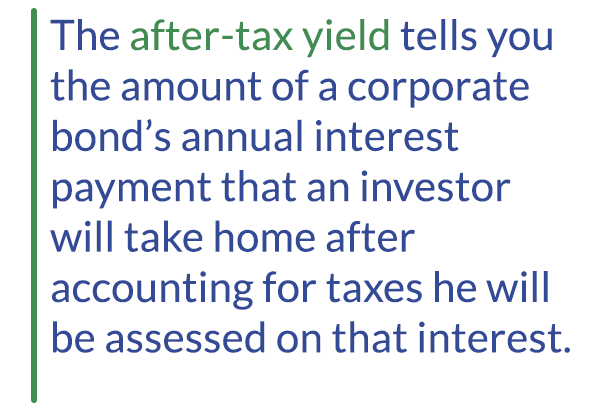

First the after-tax yield. The after-tax yield tells you the amount of a corporate bond’s annual interest payment that an investor will take home after accounting for taxes he will be assessed on that interest. Once that amount is known, the investor can compare it to the yield he would receive from a specific municipal bond and see which potential investment would put more money in his pocket. When calculating the after-tax yield, start with the annual interest percentage (a.k.a. coupon percentage) of the corporate bond, which represents the percent of the bond’s par value that an investor receives each year in interest. For instance, a corporate bond that has a $1,000 par value and an interest rate of 8% will pay an investor $80 dollars in annual interest ($1,000 x 0.08 = $80). You then multiply the coupon percentage by 1 minus the taxes an investor will pay on the corporate bond that he will not pay on the municipal bond that he is considering.

This is where it sometimes gets tricky. What taxes will an investor not pay when investing in a municipal bond that he will pay when investing in a corporate bond? Remember that for just about all municipal bonds, investors do not pay federal tax on interest received.

The formula for after tax yield is:

After-tax yield = Corporate Bond Annual Interest Rate x ( 1 – Taxes Investor Does Not Pay By Investing in Municipal Bond)

On the other hand, an investor always pays federal taxes on interest received from a corporate bond. Additionally, an investor does not pay state taxes on interest payments from a municipal bond issued in the state in which the investor lives.

On the other hand, an investor always pays state taxes on interest received from corporate bonds. So if you see an exam question in which you need to calculate the after-tax yield of a corporate bond to compare it the yield on a municipal bond, you will always subtract the investor’s federal income tax rate from 1 in the equation. You will also subtract the investor’s state tax rate from 1 if the municipal bond is issued in the investor’s state of residence.

Seems simple, right? Here’s a question to provide context:

Marilyn is a resident of Kentucky. She is considering a bond issued by XYZ Corporation. The bond comes with a 7% annual interest rate. Marilyn is also interested in purchasing municipal bonds issued in Ohio. If Marilyn has a federal tax rate of 28% and Kentucky’s state tax rate is 4%, what is the after-tax yield on XYZ’s bond?

To answer this question, begin with the interest rate on the XYZ bond, which is 7%. Then subtract from 1 the taxes Marilyn will not pay if she invests in the municipal bond in question. She will not pay federal taxes on the municipal bond interest, so you would subtract 28%, or .28. However, because Marilyn is a resident of Kentucky and the municipal bonds she is considering are issued in Ohio, she will pay state taxes on the bond. That means you would not subtract her state tax rate (0.04) from 1. After subtracting .28 from 1 to get 0.72, you multiply that amount by the 7% coupon payment. Doing so gives you a value of 5.04 (7 x 0.72 = 5.04%). This means that the interest amount she would take home from the XYZ bond would be equivalent to what she would receive from a municipal bond issued in Ohio that has a 5.04% interest payment. If she can get a bond issued in Ohio that has a higher interest payment than 5.04%, she would take home more money in annual interest payments than she would from the XYZ bond.

Tax-Equivalent Yield

The second approach an investor can take to compare how a potential bond investment will be affected by taxation is to calculate the tax-equivalent yield (TEY). This calculation is also known as the corporate-equivalent yield (CEY). The TEY/CEY measures the yield that a corporate bond will have to pay to be equivalent to a given municipal bond after accounting for taxes due. To calculate this yield, you take the annual interest of the given municipal bond and divide it by 1 minus the taxes the investor will not pay if she invests in the municipal bond that she would pay if she invested in a corporate bond.

Here’s the formula for tax-equivalent yield:

Tax-equivalent yield = Municipal Bond Annual Interest Rate / (1 – Taxes Investor Does Not Pay By Investing in Municipal Bond)

When determining what tax rates to subtract from 1 in the denominator, the same principal as described above applies. That is, the investor will not have to pay federal tax on the municipal bond, so her federal rate is always subtracted from 1. The investor will also not have to pay state tax on the bond if it is issued in the state in which she lives. If that is the case, the investor’s state tax rate should also be subtracted from 1. However, if the investor lives in a different state than the state in which the bond is issued, she will have to pay state taxes on the interest payments. In that case, her state tax rate would not be subtracted from 1.

Here’s another question to provide context.

Franz, a resident of Michigan, has purchased a Michigan municipal bond that pays 4% annual interest. If his federal tax bracket is 30% and the Michigan state tax rate is 4%, what interest rate would he need to receive on a corporate bond to have a comparable rate after accounting for taxes owed?

To answer this question, begin with the interest rate on the Michigan municipal bond, which is 4%. Then subtract from 1 the taxes that Franz will not pay on that bond that he would pay if he invested in a corporate bond. He wouldn’t pay federal taxes on the municipal bond interest, so you would subtract 0.30 from 1. Additionally, since the bond is issued in Michigan and he is a Michigan resident, Franz will not pay state taxes on the bond. So you subtract Michigan’s state tax rate of 4%, or 0.04, from 1 as well. After subtracting 0.30 and 0.04 from 1 to get 0.66, you divide that number into the 4% municipal bond annual interest. Doing so gives a value of 6.06 (4 / 0.66 = 6.06). This means Franz would need to find a corporate bond that pays 6.06% in annual interest to match the amount of interest he will take home annually from the Michigan municipal bond after accounting for taxes.

Many people are confused by the concepts of the after-tax and tax-equivalent yields. But you don’t have to be one of them. Just follow this simple approach and any questions you see on this topic will not be overly taxing.

Read Solomon Exam Prep’s expert guide for answering state registration questions on the Series 63, Series 65, and Series 66 exams. Continue reading

If you’re planning to take the NASAASeries 63, Series 65, or Series 66 exam, you can expect to see questions about when broker-dealers and their securities agents need to register in a particular state. You can also expect to see questions about when investment advisers and investment adviser representatives need to register in a state. Instead of feeling intimidated when confronted with such questions, you should relax, smile, and feel confident. That’s because if you follow the simple rules that we’re about to describe, you should get each of these questions right.

Broker-Dealers and Their Agents

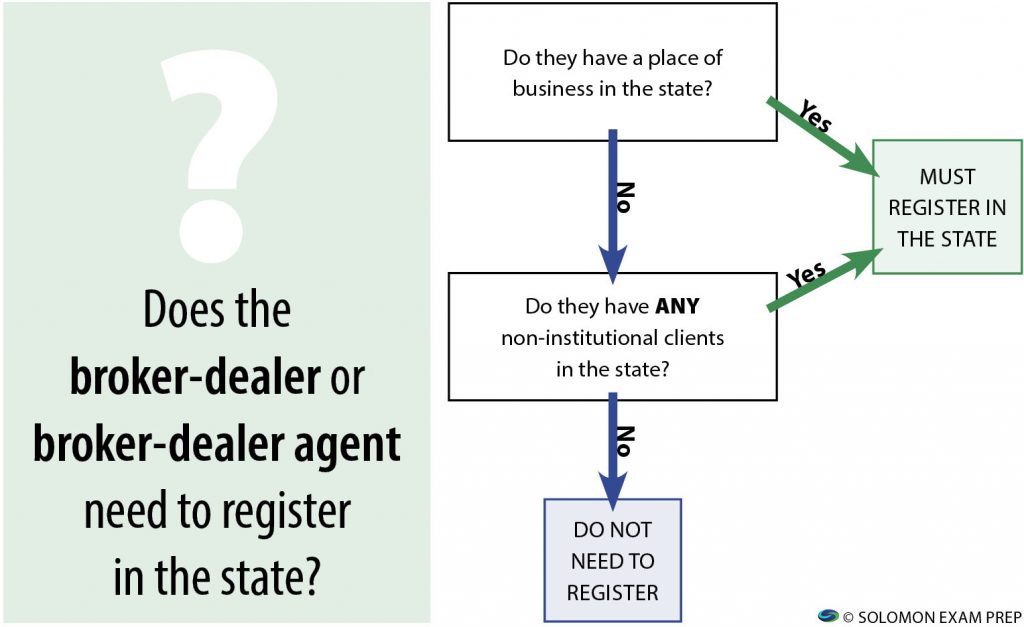

First let’s deal with questions about state registration for broker-dealers (BDs) and their agents. Rule number one here is that when a U.S.-based BD or one of its agents has an office located in a state, that BD or agent must register in the state. It does not matter which types of clients a BD or BD agent with an office in a state has or what types of securities those clients buy from the BD or agent. A BD or agent with an office in a state must register in that state. Period.

What about a BD or BD agent that doesn’t have an office in a state? If a BD or BD agent without an office in a state has any non-institutional clients in that state, the BD or agent must register there. However, if the BD or agent without an office in a state has only institutional clients in the state, no registration in that state is required. Institutional clients include the issuers of securities involved in a specific transaction; other broker-dealers; and institutional buyers, which are big-money entities such as banks, insurance companies, mutual funds, and pension and profit-sharing plans.

Key takeaway:

So when presented with a question about whether a specific broker-dealer or one of its agents must register in a given state or states, there are two potential questions to ask yourself. The first question is: “Does the broker-dealer or BD agent have an office in the state?” If the answer is yes, it’s simple: the BD or agent must register in that state. End of questions. However, if the answer is no, move on to the second question: “Does the BD or BD agent have any non-institutional clients in the state?” If the answer is yes, the BD or agent must register in the state; if the answer is no, they do not need to register in the state.

Here’s a flowchart to help you remember the question-answering process:

Investment Advisers and Their Representatives

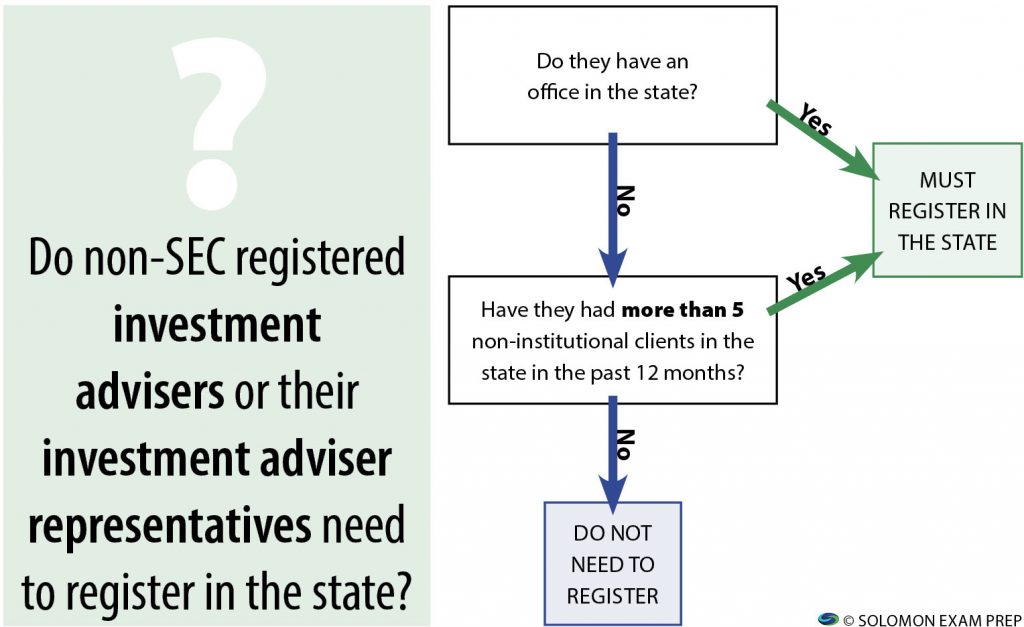

Now let’s look at the state registration requirements for investment advisers that do not register with the SEC. If the investment adviser has an office in the state, it must register there. If the investment adviser doesn’t have an office in the state but has had more than five non-institutional clients in the state during the past twelve months, it also must register there. The rules are the same for investment adviser representatives who work for an investment adviser that does not register with the SEC.

Investment adviser representatives who work for investment advisers that register with the SEC — also known as federal covered advisors — may need to register with the state if they have an office in the state.

Key takeaway:

So if you see a question about state registration requirements for non-SEC registered investment advisers or their investment adviser representatives, the first question to ask yourself is: “Does the IA or IAR have an office in the state?” If the answer is yes, you know the IA or IAR must register there. If the answer is no, move on to the second question: “Has the IA or IAR had more than five non-institutional clients in the state during the preceding twelve months?” If the answer is yes, they must register in the state; if the answer is no, they don’t need to register in the state.

Here’s another flowchart to help you with this type of question:

Remember that if an investment adviser registers with the SEC, it is a federal covered adviser and does not need to register in any state. Instead, a federal covered adviser must notice file to provide investment advice to residents of that state. When it comes to notice filing requirements for federal covered advisers, follow the same thought process as that described above. If the federal covered adviser has an office in a state, it must notice file there. If it has no office in the state but it has had more than five non-institutional clients in the state in the past twelve months, the firm must also notice file there.

Practice question

Simple, right? So let’s put the suggested thought process into practice by looking at a question like one you may see on your exam.

XYZ Broker Dealer has its main office in State A. It also has offices in States B and C. XYZ has non-institutional clients in states A and B, but it only has institutional clients in State C. It does not have an office in State D, but it has three non-institutional clients there. In which states does XYZ need to register?

A. State A only

B. States A and B only

C. States A, B, and C only

D. States A, B, C, and D

Remember the process to follow when you see questions about where a BD must register. There are two possible questions to address as part of that process.

First question: Does the broker-dealer have an office in a state? Answer: XYZ has offices in each of States A, B, and C. Recall that if the answer the first question is “yes, the BD has an office in the state”, then the BD must register in that state. So XYZ needs to register in States A, B, and C.

If the answer to the first question is no, as it is for State D, you move on to the second question: Does the BD have any non-institutional clients in the state? XYZ has non-institutional clients in State D, so the answer is yes to that question. If the answer to the second question is yes, this means the BD must register in the state. Thus, XYZ has to register in State D as well as States A, B, and C. So Choice D is the correct answer.

So now you’re an expert, and you’re one step closer to passing your Series 63, Series 65, or Series 66 exam!

Want more exam tips?

Watch a video version of “How to Answer State Registration Questions on the Series 63, Series 65, and Series 66” on the Solomon YouTube channel, where you’ll find even more exam and study tips!

Solomon Exam Prep has helped thousands pass their securities licensing exams, including the SIE and the Series 3, 6, 7, 14, 22, 24, 26, 27, 28, 50, 51, 52, 53, 54, 63, 65, 66, 79, 82 and 99.

FINRA and the NASAA are now offering Prometric’s ProProctor remote assessment service which allows you to choose where and when you take your security exam. This user-friendly testing platform Continue reading

FINRA and the NASAA are now

offering Prometric’s ProProctor remote assessment service which allows

you to choose where and when you take your security exam. This user-friendly

testing platform offers self-service capabilities, with live agents available

at all times to offer support for candidates if required.

ProProctor

features advanced security measures to ensure the same safety standard is being

met comparable to conventional test centers, guaranteeing a consistent and fair

testing experience for all candidates. These advanced security measures include

multiple ID authentication and facial detection checks, personal security

checks, 100% live-monitoring, 360-degree environmental readiness checks, live

security agents, proactive protocols such as device checks, as well as record

and review functionalities.

Each test candidate is assigned three agents to ensure

the exam is administered safely and securely, with a proctor present throughout

the entire test.

In order to access Prometric’s ProProctor system, you

must install an application on your laptop or desktop and perform a system

check.

It is important to note the following difference with

exams at the traditional test center: online tests via ProProctor are

forward-moving only. No flagging a question and returning to it. No changing

your answer.

The

online exams have an onscreen calculator, a virtual scratchpad to capture your

notes digitally as well as highlight and strikethrough functionality, which

allow you to mark through or bring attention to the portions of the displayed

exam question.

Test-takers

and firms may schedule online test appointments for the following six exams:

the SIE, Series 6, Series 7, Series 63, Series 65, and Series 66.

It was previously announced that FINRA and NASAA had been working to introduce an online testing service as an alternative to candidates taking their exam at traditional test centers, to be launched Continue reading

It was previously announced that FINRA and NASAA had been

working to introduce an online testing service as an alternative to candidates

taking their exam at traditional test centers, to be launched on May 24th.

FINRA has now announced that this service, which is

currently in its pilot phase, requires further validation before it can be

implemented and therefore will not be launched on May 24th as

planned. This also means that there will be a delay in booking appointment

times for the five exams that will be included in its initial launch, including

the SIE, Series 6, Series 7, Series 63, and Series 66 exams.

FINRA has also updated policies for test candidates,

extending enrollment windows that have either expired, or are due to expire

between March 16th and June 30th, 2020. This includes all

FINRA, NASAA and MSRB exam enrollment dates, with affected enrollment windows

being systematically updated in CRD.

Prometric will continue to reopen test centers in accordance

with local, state and federal regulations. You can check their Site Openings page, which is

continually being updated. You can also read more about the Prometric policies

to ensure candidate safety on their Covid-19 Update page.

If your Solomon Exam Prep materials are due to expire

before June 1st, contact Customer Service on 503 601 0212 or by

email at info@solomonexamprep.com

for a complimentary extension until August 1st.

Notice filing is a topic that often confuses people studying for the Series 63 Uniform Securities Agent State Law exam or the Series 65 Uniform Continue reading

Notice filing is a topic that often confuses people studying for the Series 63 Uniform Securities Agent State Law exam or the Series 65 Uniform Investment Adviser Law exam or the Series 66 Uniform Combined State Law exam. Some mistakenly assume that notice filing is the same as state registration. While there are some similarities, notice filing and state registration are different and the Series 63, Series 65 and Series 66 exams require that you understand the distinction.

So what is notice filing, and how does it work?

To understand the concept of a notice filing, it’s important to know a bit about the entities to which it applies: federal covered advisers and federal covered securities. First, let’s look at federal covered advisers. A federal covered adviser is an SEC-registered adviser that offers investment advice in exchange for compensation. Any adviser with assets under management of $110 million must register as a federal covered adviser.

When it comes to registration, advisers are not subject to double registration, meaning that an investment adviser registered with the SEC does not need to register with any state, and an adviser that is required to register with a state does not register with the SEC. For federal covered advisers, this makes life easier because a federal covered adviser only needs to go through the rigorous registration process one time. Instead of registering in a state, on Form ADV that it files with the SEC, a federal covered adviser lists any states in which it will either have an office or more than five retail clients in a twelve-month period. The SEC then gives notice to the administrator in any state noted on the adviser’s form ADV that the adviser intends to do business in that state. This is a notice filing: a simple heads-up to the state administrator that the advisor will be doing business in its state. Depending on the requirements of the given state, the adviser may be asked to file additional paperwork and pay a fee before offering advice to clients in the state. But, happy day, the adviser gets to skip the state registration process.

Now let’s discuss notice filing for federal covered securities. What is a federal covered security? Well, many of the securities that the average investor is likely to own are federal covered securities. For example, any security traded on an exchange like the NYSE or NASDAQ is a federal covered security. Additionally, securities issued by investment companies that are registered under the Investment Company Act of 1940, such as mutual funds and closed-end funds, are federal covered securities. A federal covered security must be registered with the SEC, but the issuing company is not required to register it with any state. Instead, the issuer must note on its registration statement any state in which it intends to sell the security. The SEC then notifies the administrator of each noted state of the issuer’s intention to sell in that state. Sound familiar? It should because this is also a notice filing: a simple shout-out by the SEC to the state administrator that the security will be sold in its state. Typically the issuer is then required to submit its SEC registration documents to the administrator and pay a filing fee, but, and this is a biggie, the issuer does not need to go through the demanding state registration process in order to sell its securities in the state.

So it’s actually pretty simple. A federal covered security or adviser is registered once with the big boys at the SEC. After that, it’s all smooth sailing. No need for further registration, just a simple notice given to states in which the security will be sold or the adviser will offer investment advice.

Now that you’ve learned the difference between notice filing and state registration, let’s do a practice question to get you ready for the Series 63, Series 65 or Series 66 exam:

**

Spencer Investments is a federal covered investment adviser doing business in Oregon. The Administrator in Oregon requires a notice filing. Does this mean Spencer Investments must register in Oregon as well as with the SEC?

A. No. What it means is that Spencer needs to request that the SEC send the Oregon Administrator a copy of Spencer’s Form ADV, and Spencer needs to pay a notice filing fee to the Oregon Administrator. B. Yes. Spencer does business in Oregon, so it must register in Oregon. C. Spencer Investments does not have to register in Oregon but does need to fill out and file all the paperwork for registration so the Oregon Administrator is on “notice” regarding Spencer’s business in Oregon. D. Yes. The Oregon requirements for registration may be more stringent than the SEC’s, so Spencer must comply with them to do business in Oregon.

Correct Answer: A. No. What it means is that Spencer needs to request that the SEC send the Oregon Administrator a copy of Spencer’s Form ADV, and Spencer needs to pay Oregon a notice filing fee. A notice filing for an investment advisor is not a registration but means the registration papers Spencer Investments filed with the SEC are shared with the Oregon Administrator, and the Oregon Administrator receives a filing fee.

If you’re studying for a FINRA, NASAA or MSRB securities licensing exam such as the Series 6, Series 7, Series 65, Series 66, Series 50, Series 52, Series 79, Series 82 or Series 99, and you’re wondering how the sweeping tax overhaul might affect your exam and your studying, have no fear, the Solomon Exam Prep team is hard at work figuring out what the changes might mean for securities exam-takers. Continue reading

If you’re studying for a FINRA, NASAA or MSRB securities licensing exam such as the Series 6, Series 7, Series 65, Series 66, Series 50, Series 52, Series 79, Series 82 or Series 99, and you’re wondering how the sweeping tax overhaul might affect your exam and your studying, have no fear, the Solomon Exam Prep team is hard at work figuring out what the changes might mean for securities exam-takers. Regulators and exam committees have yet to weigh in, so what follows is just a first pass at the tax reform law that might be of particular interest to Solomon securities exam-takers:

Investment management fees

The new tax law eliminated a bunch of deductions that had been grouped together as “miscellaneous itemized deductions.” This includes deductions for unreimbursed employee expenses, union dues, legal expenses, and tax preparation, all of which are now gone. The biggest loss for investment advisers is that customers may no longer deduct their fees.

The loss of these deductions only applies to individuals. Businesses (including sole proprietorships) will still be able to deduct fees for investment advice. Individuals would have been less likely to use the deduction anyway, since the increase in the standard deduction makes itemizing less attractive.

The pass-through deduction

There is a new 20% deduction for people who get their income through a “pass-through entity” like a partnership, LLC, or S corporation. But not all pass-through income gets the deduction. This is one of the more complex provisions in the new law. A major limitation is that the deduction begins phasing out after $157,500 for certain “service trades or businesses,” defined as “any trade or business where the principal asset of such trade or business is the reputation or skill of 1 or more of its employees or owners.” Financial and brokerage services are specifically named as among the businesses in this category.

Benefits to REITs

REITs are pass-through entities, and income from REIT dividends gets the pass-through deduction, while avoiding the cap for income from service trades or businesses. The portion of a REIT’s dividends that comes from capital gains on the REIT’s property is specifically excluded from the new deduction. However, as a capital gain this portion is taxed at a lower rate to begin with.

REITs were also given the ability to opt out of a provision of the new law that could have hindered them. Most businesses must now accept a cap on the amount they can deduct for interest on their debt. A REIT can choose not to be subject to this limitation, if it also agrees to deduct depreciation on its real estate at a slower rate.

Advance refundings no longer tax-exempt

Under the new law, bonds issued for the purpose of “advance refunding” are never tax-exempt, not even for government bonds. Advance refunding is when the bond issuer wants to take advantage of lower interest rates by selling new bonds to pay off old bonds. If the old bonds are more than 90 days from maturity, this practice is considered advance refunding and the new bonds lose their tax-exempt status.

New income tax brackets for estates and trusts

The new law doubles the threshold before the estate tax kicks in, from $5.6 million to $11.2 million.

Estates and trusts also got lower tax rates and new tax brackets along with other types of taxpayers, as follows:

Old

New

Income

Rate

Up to $1,500

15%

$1,501 – $3,500

28%

$3,501 – $5,500

31%

$5,501 – $7,500

36%

$7,501 +

39.6%

Income

Rate

Up to $2,550

10%

$2,551 – $9,150

24%

$9,151 – $12,500

35%

$12,501 +

37%

In addition, disability trusts still get the personal exemption that was eliminated for individuals.

Fewer taxpayers subject to alternative minimum tax

The alternative minimum tax (AMT) is designed to make sure wealthy taxpayers don’t reduce their taxes beyond a certain amount. Under the old law, individual taxpayers had to have an income of $54,300 for singles or $84,500 for married couples before they needed to worry about the AMT. Those amounts were raised to $70,300 for singles and $109,400 for married couples.

The AMT for corporations has been eliminated entirely.

Changes for special savings plans

The bill included several changes to IRAs, 401(k)s, and 529s. For example, converting a traditional IRA into a Roth IRA no longer comes with the option to change your mind and convert back within a limited period of time. People who lose or leave a job with an outstanding 401(k) loan now have longer to pay it back. 529 accounts can now be used for elementary and secondary school expenses, up to a limit of $10,000.

What didn’t make it into the final bill

The final version of the bill passed on December 20th. When you search for information about it, you should pay close attention to when that information was published or posted.

For example, at one point the bill included a proposed FIFO (first-in, first-out) rule, which said that when selling part of your stock in a company you have to sell the oldest shares first. Since the oldest shares have probably gained the most value, you would have owed more capital gains tax, at least in the short term.

However, the FIFO rule was dropped from the final version of the bill. You may have also read about a major reduction in the annual contribution limits for 401(k)s, or a proposal to remove the tax-exempt status of private activity bonds. Neither made it into the final bill.

This process is not over. Although the ink has dried on the legislation itself, the situation is still developing with regard to how the law will actually be applied in practice and how it will affect your licensing exam. Count on Solomon Exam Prep to be there with the most up-to-date information as it relates to FINRA, NASAA and MSRB securities licensing exams.

With the release of the Solomon Exam Prep app, you have full mobile access to your Solomon study materials with the click of a button. Continue reading

Do you need to take a securities licensing exam?

Do you wish you had more time to study?

With the release of the Solomon Exam Prep Android app, you have full mobile access to your Solomon study materials at the click of a button.

Easier and quicker—Just click the Solomon Exam Prep icon on your phone to be taken directly to your account.

Access all your materials—The app provides full site functionality and access to your study guide, exam simulator, audiobook, and video lecture.

No typing on tiny keyboards—Don’t worry about typing in a web address! Our app will take you right where you need to be.

Move into the future of mobile securities exam prep with the Solomon Exam Prep app!

Solomon Exam Prep has helped thousands of financial professionals pass their FINRA, NASAA, and MSRB licensing exams, including the Series 6, Series 7, Series 24, Series 26, Series 27, Series 28, Series 50, Series 51, Series 52, Series 53, Series 62, Series 63, Series 65, Series 66, Series 79, Series 82, and the Series 99.