Interview: How Fernando Russo passed four securities licensing exams

Preparing for the SIE, Series 63, Series 79, Series 82, or another securities licensing exam? Read about one Solomon Exam Prep student’s path to success. Continue reading

Preparing for the SIE, Series 63, Series 79, Series 82, or another securities licensing exam? Read about one Solomon Exam Prep student’s path to success. Continue reading

Solomon Exam Prep explains what a Series 7 General Securities Representative can and cannot do and how this compares to other rep-level registrations. Continue reading

Options are a common topic on the Series 6, Series 7, Series 65, Series 66, and SIE exams. Read our guide to calculating gains and losses on exercised options. Continue reading

If you’re studying for securities licensing exams, such as the SIE or the Series 7, then you should understand the terms “accredited investor” and “QIB.” Continue reading

If you’ve been studying for the Series 7, 6, 14, 22, 24, 65, 79, or 82, or the Securities Industry Essentials (SIE), then you’ve had to learn about Regulation D private placements and Rule 144A sales. Regulation D private placements are securities offerings that are exempt from the normal SEC registration process and in many cases are sold only to “accredited investors” or limit the involvement of investors who are not accredited. Rule 144A sales are sales of unregistered securities to large institutional investors known as “qualified institutional buyers” or QIBs for short.

You may have wondered about the difference between accredited investors and QIBs. On the surface, these may seem similar. Each refers to a category of investor with resources and/or knowledge above and beyond the average retail investor. So why not just have one standard for buyers under both Rule 144A and Regulation D? After all, the purpose of both Regulation D and Rule 144A is the same: to allow wealthier and more sophisticated investors easier access to investments that may be too risky for the average investor.

To begin to answer this question, we have to start with the fact that wealth and sophistication fall on a spectrum. Investors aren’t neatly divided between small retail investors and huge financial institutions that move millions around without blinking an eye.

You could think of accredited investors as a middle ground between these two extremes. Accredited investors are investors whose financial status or investment knowledge may give them a greater ability to handle the risks inherent in a private placement. There are many ways to qualify as an accredited investor but they all have one thing in common, which is that the SEC believes they indicate an ability to take on risks that regulators believe are unsuitable for most retail investors.

Accredited investors are investors whose financial status or investment knowledge may give them a greater ability to handle the risks inherent in a private placement.

An accredited investor that is not an individual—such as a business, governmental, or nonprofit entity—is sometimes called an institutional accredited investor (IAI).

QIBs are a narrower group of large institutional investors. A QIB is a large institutional investor that owns at least $100 million worth of securities, not counting securities issued by its affiliates. For registered broker-dealers, the threshold is lower, just $10 million. A bank must also have a net worth of at least $25 million in order to be considered a QIB.

If a firm has discretionary authority to invest securities owned by a QIB, those securities count toward whether the firm itself is considered a QIB. So if a broker-dealer has $9 million worth of securities in its own accounts, and holds $1 million worth of securities in a discretionary account belonging to a QIB, then the broker-dealer is itself a QIB.

Common examples of QIBs include broker-dealers, insurance companies, investment companies, pension plans, and banks. However, any corporation, partnership, or LLC could qualify as a QIB. So can an IAI that owns at least $100 million in securities. Individuals can never be QIBs, regardless of their assets or financial sophistication.

Individuals can never be QIBs, regardless of their assets or financial sophistication.

Rule 144A allows QIBs to buy unregistered securities at any time, and freely trade these shares to other QIBs. In effect, QIBs can trade unregistered shares among themselves with almost the same ease as trading registered shares. Selling unregistered securities to anyone other than a QIB commonly requires a the seller to hold the securities for a period of up to 12 months.

A QIB will virtually always meet the criteria to be an accredited investor, whereas an accredited investor may fall well short of QIB status.

Over time, other securities laws and regulations have made use of these two well-known categories. For example, in 2019 the SEC gave issuers more flexibility to test the waters with potential investors before deciding whether to go through with a public offering. When deciding which investors were sophisticated enough to receive test-the-waters communications, the SEC limited these communications to QIBs and institutional accredited investors. Additionally, references to institutional accredited investors have become more common, such as when the SEC revamped its rules around integration of offerings in March 2021.

Know your QIBs from your accredited investors and be ready to pass your securities exam with Solomon Exam Prep.

For more helpful securities exam-related content, study tips, and industry updates, join the Solomon email list. Just click the button below:

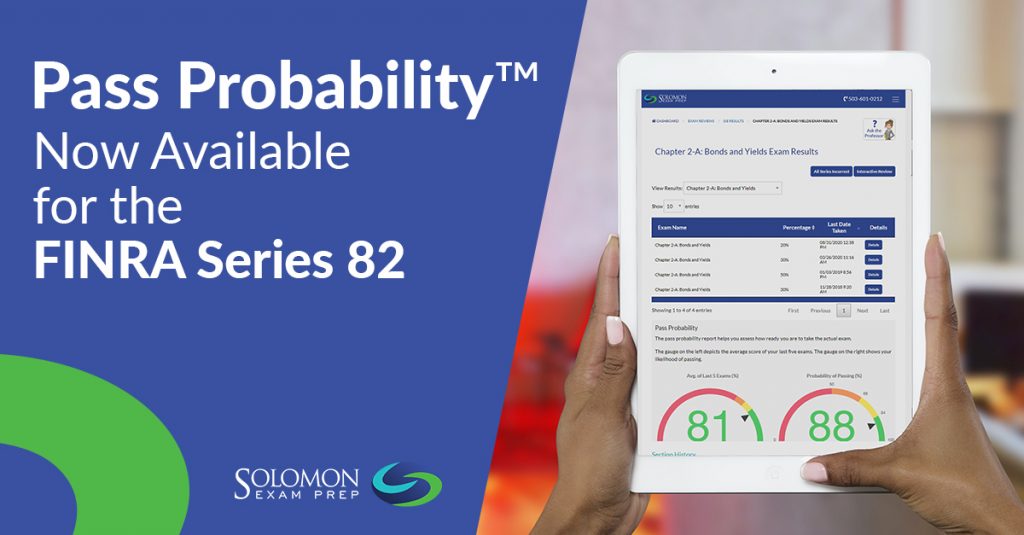

Everyone would like to feel confident when they take their securities exam, but how do you know if you’re ready for test day? Solomon Exam Prep can help – with Pass Probability™. Continue reading

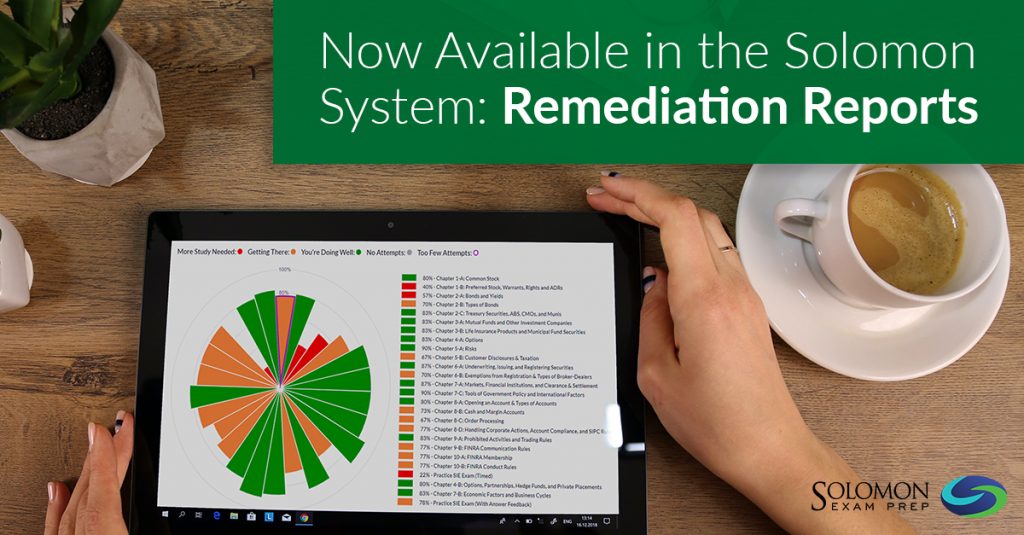

Learn about the Solomon Remediation Report, a new analytical feature designed to help students pass their securities licensing exams the first time. Continue reading

Solomon Exam Prep is delighted to announce an advanced analytical feature called a Remediation Report. The Solomon system analyzes a student’s five most recent practice exams and determines whether a student is ready to take his or her exam. If Solomon AI determines that a student is not ready to sit for their exam, then it creates an individual report with personalized guidance on how to remediate and prepare to pass. This custom Remediation Report is sent to the Solomon student’s email inbox.

The Solomon Remediation Report is connected to the Solomon Pass Probability tool, the industry-leading measure of a security exam prep student’s readiness to pass an exam. Solomon Pass Probability is based on thousands of student data points. Once a Solomon student has taken at least five practice exams, the Solomon Pass Probability feature is activated, and the Pass Probability metric is available in the student’s dashboard. The Solomon Remediation Report provides an additional level of customized study support by helping students focus their efforts and remediate before they sit for their exam.

Solomon Pass Probability and Remediation Reports are currently available for the following exams: SIE, Series 6, Series 7, Series 63, Series 65, Series 66, Series 79, and Series 82.

To learn about all the features of the Solomon Exam Prep learning system, watch the video overview.

If you’re studying for the SIE, Series 65, Series 7, or another securities licensing exam, try this evidence-based study strategy. Continue reading

Research from Dr. Tania Lombrozo of UC Berkeley, published in the journal Trends in Cognitive Science, shows that explaining a new concept to another person is an enormously helpful learning technique. When you explain an unfamiliar concept to another person, your brain makes crucial learning connections. However, many people don’t have a person around them that is ready to listen to their new knowledge. Thus, Dr. Lombrozo recommends self-explanation, which is the practice of explaining concepts to yourself in order to better understand them.

Dr. Lombrozo found that the positive effects of self-explanation can be attributed to the generalization process. Explaining requires you to put new information in the context of “prior beliefs,” which makes you generalize the information. In doing so, you’re forced to pick out what is most necessary for understanding the concept. In thinking about how to explain something, you in fact learn more about the thing itself!

Dr. Lombrozo describes an experiment by psychologists Amsterlaw and Wellman that demonstrates the power of explaining in understanding. In Amsterlaw and Wellman’s experiment, they administered logic tests to children under various conditions. During the course of the experiment, the children were split into groups. One group would answer, and then they would be asked to explain the correct answer once it was revealed. A comparison group did the same, but only for half the problems. The third group was a control group and gave no explanation at all.

According to Amsterlaw and Wellman, “children in the explanation condition significantly outperformed the comparison and control groups….” In other words, explaining increased their understanding.

What does this mean if you’re studying for the Series 65 or the Series 7 or some other securities licensing exam? Solomon Exam Prep suggests finding someone in your life who will listen to you explain topics from your securities exam prep. The person you choose doesn’t need to have any knowledge of securities. The person just needs to be a good listener. Even better, someone who will ask questions.

What if you don’t have anyone who can do that for you? Well, as Dr. Lombrozo showed, the practice of self-explanation is also helpful and will increase your understanding of the material you’re trying to learn.

Visit the Solomon Exam Prep website to explore study materials for 21 different securities licensing exams, including the SIE and the Series 3, 6, 7, 14, 22, 24, 26, 27, 28, 50, 51, 52, 53, 54, 63, 65, 66, 79, 82 and 99.

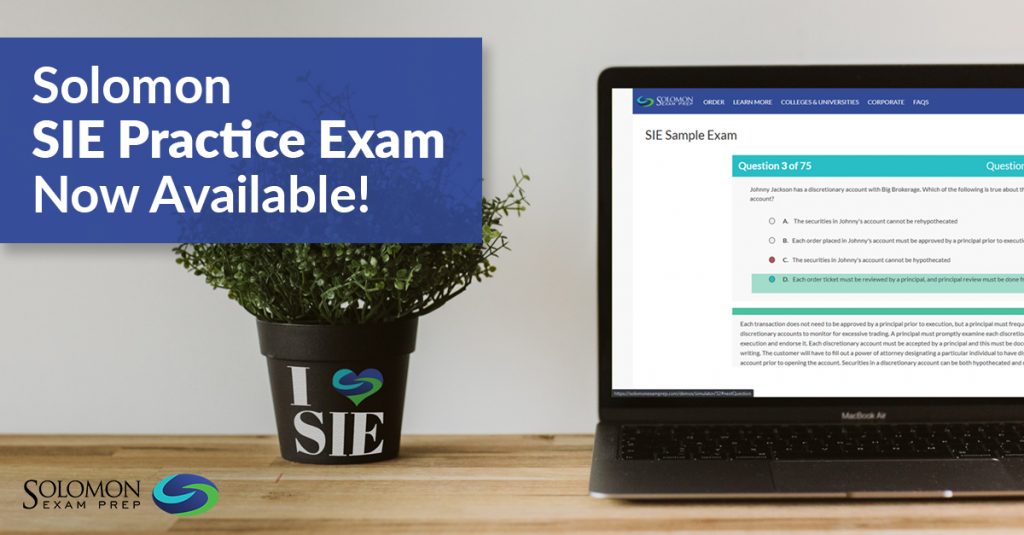

Meet the newest addition to Solomon Exam Prep’s lineup of free Sample Quizzes: the SIE Sample Exam! Visit the Solomon website to try it out. Continue reading

Meet the newest addition to Solomon Exam Prep’s lineup of free Sample Quizzes: the SIE Sample Exam! Like all Solomon Sample Quizzes, the SIE Sample Exam features questions from our industry-leading Online Exam Simulator. Questions are written by Solomon content experts, who are experienced in both investment education and the process of adult learning.

But unlike other Solomon Sample Quizzes, the SIE Sample Exam is a FULL exam – it contains 75 questions, just like the real FINRA SIE exam – giving you an even better idea of what the actual exam is like. You will encounter easy, medium, and difficult questions so that you can more easily gauge your current knowledge of SIE content.

All Solomon Sample Quizzes and Exams also provide instant feedback for each answer, with a full rationale to help you understand the WHY behind the what. Plus, you get a report at the end detailing your results and giving you the opportunity to review all the questions.

Visit the Solomon website here to try out the SIE Sample Exam and explore free samples of quizzes for 21 different exams.

This month’s study question from the Solomon Exam Prep Online Exam Simulator question database is now available. Continue reading

This month’s study question from the Solomon Online Exam Simulator question database is now available.

*** Comment below or submit your answer to info@solomonexamprep.com to be entered to win a $20 Starbucks gift card.***

This question is relevant to the SIE and the Series 7, 14, 50, 52, and 54.

Question: A Municipal Finance Professional (MFP) hosted a $500 plate fundraiser for a governmental issuer. Does this event trigger a ban on business for two years?

A. Yes, it will trigger a ban because an MFP may not host a fundraiser.

B. Yes, it will trigger a ban because the cost per plate is above the de minimis amount.

C. No, it will not trigger a ban because the MFP did not contribute money, only time and space.

D. No, it will not trigger a ban because the MFP was holding the fundraiser, not the municipal dealer.

Correct Answer: A

Explanation: MFPs are not permitted to solicit funds for municipal issuers or their officials without triggering a two-year ban on business for their firm. Thus, holding fundraisers is not allowed. Municipal dealers are also forbidden from holding fundraisers.

To explore free samples of Solomon Exam Prep’s industry-leading online exam simulators for the SIE, Series 7, Series 14, Series 50, Series 52, Series 54, and other FINRA, MSRB, NASAA, and NFA exams, visit the Solomon website here.

Do your customers know the difference between an IA and BD? Do you know the importance of this distinction and how it may affect your registration status? Continue reading

Do your customers know the difference between an investment adviser and broker-dealer? Do you know the importance of this distinction and how it may affect your registration status?

For many retail customers, the difference between an investment adviser (IA) and a broker-dealer (BD) may not seem important. A customer may have received an investment recommendation from a BD, or owned securities through an IA account. However, which kind of firm you work for is important for knowing which services you may provide, how you may provide them, and which qualification exams you must pass.

Investment advisers are usually firms, though they can be an individual operating as a sole proprietor, whose primary business is providing investment advice, and who are paid for the advice itself. Investment adviser representatives (IARs) are individuals who work for IAs and advise the IA’s clients on the IA’s behalf. IAs and IARs are not “stockbrokers” and cannot directly buy or sell securities for their customers. While many have IA accounts through which they own stocks, mutual funds, and other securities, in fact these are accounts an IA opens on the customer’s behalf with a BD.

Broker-dealers are usually firms, though they can be an individual operating as a sole proprietor, that execute securities transactions for customers. An individual who is employed by a BD to handle customer accounts is called an “agent of a broker-dealer” on some exams, or a “registered representative” (RR) on others. BDs can offer investment advice incidental to their work with customers but cannot be compensated for the advice itself. If a BD acts as an intermediary between a buyer and a seller, then the BD can charge a commission on the trade. If a BDs buys or sells from its own inventory, then the BD makes money by charging a markup on securities that they sell and taking a markdown on securities that they buy.

Finally, many firms, especially larger ones, maintain both IA and BD registrations. When working for these “dual registrants,” you may be asked to qualify as an IAR, BD agent, or both, depending on your role.

In fact, an increase in dual registrations is one of the note-worthy trends Solomon discusses in our recent white paper, “Optimizing On-Boarding in 2021: 7 Key Trends for the Securities Industry,” available for download from this blog post.

To become an agent of a broker-dealer (registered representative), you must pass the Securities Industry Essentials (SIE), and a “top-off” exam such as the Series 6 or Series 7, and for state registration usually the Series 63. To become an IAR, you must pass either the Series 65, or, if you work for a dually registered firm, the SIE, the Series 7, and the Series 66.