Solomon Exam Prep explains what a Series 7 General Securities Representative can and cannot do and how this compares to other rep-level registrations. Continue reading

Of the representative-level FINRA registrations categories, the General Securities Representative (Series 7) registration is considered by many to be the most valuable, due to the range of products it allows you to sell. But how “general” is it? Are there other representative-level registrations that permit you do things a Series 7 representative cannot?

What is a Series 7 representative permitted to do?

FINRA allows a General Securities Representative to solicit the purchase and sales of all securities products, including:

Stocks, whether from IPOs, private placements, or secondary market trading

Other corporate securities, such as bonds, rights, and warrants

Mutual funds

Closed-end funds

Money market funds

Unit investment trusts (UITs)

Exchange-traded funds (ETFs)

Real estate investment trusts (REITs)

Variable contracts (insurance products whose funds are invested in securities)

Municipal securities

Municipal fund securities, such as 529 plans

Options

Government securities

Direct participation programs (DPPs)

Venture capital

Hedge funds

This long list of products means that a Series 7 registered rep may perform the functions of an Investment Company and Variable Contracts Representative (Series 6), Direct Participation Programs Representative (Series 22), or Private Securities Offerings Representative (Series 82).

Besides sales, General Securities Representatives may also perform certain activities closely related to sales. They may:

recommend investments after performing a suitability analysis for the customer

accept unsolicited orders

open customer accounts, subject to approval by a principal

What is a Series 7 representative NOT permitted to do?

Though a General Securities Representative may solicit purchases of IPO shares, he may not work on underwriting or structuring an IPO, or any other securities offerings. This means that he is not permitted to advise an issuer on an offering. This work requires registration as an Investment Banking Representative (Series 79). Likewise, working on municipal underwriting requires registration as a Municipal Securities Representative (Series 52).

A Series 7 representative is also not qualified to perform the back-office functions of an Operations Professional (Series 99). Among these functions are maintaining possession or control of the firm’s securities, calculating margin for margin accounts, and sending trade confirmations and account statements.

Of course, every registered representative must also pass the FINRA Securities Industry Essentials (SIE) exam. The SIE doesn’t qualify you to do anything, instead it is a foundational exam that focuses on industry terminology, securities products, the structure and function of the markets, regulatory agencies and their functions, and regulated and prohibited practices. Unlike other FINRA securities exams, you do not need to be employed or sponsored by a broker-dealer in order to take the SIE. The only requirement is that you be 18 years old.

If you’re considering taking the Series 7 exam, Solomon Exam Prep is here to help. Solomon provides a wide variety of study materials, together with resources such as study schedules, the Ask The Professor function, and helpful exam information. Explore Solomon’s Series 7 study materials.

Options are a common topic on the Series 6, Series 7, Series 65, Series 66, and SIE exams. Read our guide to calculating gains and losses on exercised options. Continue reading

Options are a topic that many taking the Series 6, Series 7, Series 65, Series 66, and SIE exams have to deal with. One of the biggest problems that students have with options questions occurs when they are asked to calculate gains and losses on exercised options. As long as you understand a few basic points, these types of questions can be a breeze and definitely nothing to lose sleep over.

First of all, let’s remind ourselves of what an option is. An option is a contract between two parties that gives the buyer of the contract the right to buy or sell an underlying asset to the other party in the future for a specific price. The specific price is called the “exercise” or “strike” price. The seller of the option, on the other hand, is obligated to buy or sell, at the strike price. The option to buy is a “call” option, the option to sell is a “put” option.

To calculate gains and losses on exercised options, you first need to understand what is happening as a result of an options transaction. When an option is exercised, that means its holder chooses to either buy or sell the underlying security at the strike price. With an exercised call option, the holder purchases shares of the underlying security from the options seller; with an exercised put option, the holder sells shares of the underlying security to the options seller. The sale in each case occurs at the option’s strike price.

Buying – Exercised Call Option

When a call options holder exercises her option by purchasing the underlying shares, she must add the cost of those shares to the premium she paid to obtain the option in the first place. This sum represents the option holder’s total money spent as a result of her options transaction. If the option holder then elects to sell the underlying securities she’s just purchased at their current market price, the money she receives from the sale will be money she takes in. To calculate her gain or loss, subtract the money she paid out from the money she took in. It’s as simple as that.

So, if, for instance, Marie paid $200 in premiums to purchase a call option with a strike price of $20 and then exercised the option by purchasing 100 shares of the underlying stock, the money she spent as a result of her options transaction will be $2,200 ($200 premium paid + $2,000 purchase price for underlying securities). If she then sells those 100 shares at the market price of $25, she will receive $2,500 in sales proceeds. Subtracting the money she spent from the amount she received will result in a $300 gain ($2,500 sale proceeds – $2,000 purchase price – $200 premium paid = $300 gain.)

Buying – Exercised Put Option

In order for a put options holder to exercise his option, he must have 100 shares of the underlying security to sell to the options seller. That means he needs to go out in the market and purchase shares at their market price. The money he pays for those securities plus the premium he paid to purchase his put option in the first place represents money spent as a result of his options transaction. The options holder will then sell those 100 shares to the options seller at the strike price. When he does this, he receives the sale proceeds. Subtracting the money spent on the put from the sale proceeds will result in the put investor’s gain or loss.

So, if, for instance, Pierre paid $300 in premiums to purchase a put option with a strike price of $30 and then purchases 100 shares of the underlying stock when its market price drops to $25, he will have spent $2,800 as a result of his options transaction ($300 premium + $2,500 purchase price for underlying shares). He will then sell those 100 shares to the options seller at their strike price of $30 and take in $3,000 from his sale. Thus, Pierre will make a total of $200 on his options transaction ($3,000 sale proceeds - $300 premium – $2,500 purchase price = $200 gain).

Selling an Option

Now let’s look at gains or losses from the perspective of an options seller. Remember that when someone sells an option, he receives the premium from the options buyer. If the option expires unexercised, the seller gets to keep his entire premium received, which represents his maximum potential gain. If the option is exercised, he will either be required to sell shares of the underlying security to the option holder in the case of a call option or buy shares from the option holder in the case of a put option. Each of an exercised call or an exercised put option transaction is made at the option’s strike price.

Selling – Exercised Call Option

When a call option is exercised, the option seller must obtain 100 shares of the underlying stock to sell to the options holder. To do so, he will have to purchase the shares at their current market price, which will be higher than the option’s strike price. He will then sell them to the option holder at the strike price. The money he takes in from the sale is added to the premiums he received when shorting the option, and this totals the money he takes in as part of his options transaction. The money he paid to obtain the underlying securities is the money he pays out. Subtracting the money he pays out from the money he takes in results in his overall gain or loss.

For example, let’s say Michael sells a call option with a strike price of $50 and receives premiums totaling $500. If the option is exercised, and Mike purchases the underlying shares at $55, he will have paid out $5,500 as a result of his options transaction. At the same time, he will have received $5,500 ($500 premium + $5,000 strike price). Thus, Mike will break even on this transaction; money taken in will be equal to money paid out.

Buying – Exercised Put Option

When a put option is exercised, the option seller must purchase 100 shares of the underlying security from the options holder at the strike price. This represents money the options seller pays out. The options holder has already received the premium when she sold the option, and after purchasing the 100 shares, she can sell them for their current market price. The combination of the seller’s sale proceeds and the premium received represents money taken in. Subtracting money paid out from money taken in will result in the investor’s gain or loss.

Let’s say Maribel shorts a put option and receives premiums totaling $400. The option has a strike price of $40, and the option holder exercises it when the underlying stock is trading at $35. This means Maribel is obligated to pay $4,000 total for the 100 underlying shares. This is money she pays out. She has already taken in $400, and if she chooses to sell the underlying stock at its current market price, she will take in an additional $3,500 in sales proceeds. This means she will receive a total of $3,900 from his options transaction ($3,500 sale proceeds + $400 premium) and paid out a total of $4,000. As a result, she has lost $100 on his options transaction ($3,900 money in – $4,000 money out = -$100).

As long as you understand what is occurring when an option is exercised, calculating gains and losses is as simple as comparing the money the investor takes in to the money she pays out. Calculating gains and losses on exercised options requires an understanding of the transaction and some simple math. Follow the guidance above and you will be able to correctly answer this type of question on your securities licensing exam.

For more helpful securities exam-related content, study tips, and industry updates, join the Solomon email list. Just click the button below:

If you’re studying for securities licensing exams, such as the SIE or the Series 7, then you should understand the terms “accredited investor” and “QIB.” Continue reading

If you’ve been studying for the Series 7, 6, 14, 22, 24, 65, 79, or 82, or the Securities Industry Essentials (SIE), then you’ve had to learn about Regulation D private placements and Rule 144A sales. Regulation D private placements are securities offerings that are exempt from the normal SEC registration process and in many cases are sold only to “accredited investors” or limit the involvement of investors who are not accredited. Rule 144A sales are sales of unregistered securities to large institutional investors known as “qualified institutional buyers” or QIBs for short.

You may have wondered about the difference between accredited investors and QIBs. On the surface, these may seem similar. Each refers to a category of investor with resources and/or knowledge above and beyond the average retail investor. So why not just have one standard for buyers under both Rule 144A and Regulation D? After all, the purpose of both Regulation D and Rule 144A is the same: to allow wealthier and more sophisticated investors easier access to investments that may be too risky for the average investor.

To begin to answer this question, we have to start with the fact that wealth and sophistication fall on a spectrum. Investors aren’t neatly divided between small retail investors and huge financial institutions that move millions around without blinking an eye.

Accredited Investors

You could think of accredited investors as a middle ground between these two extremes. Accredited investors are investors whose financial status or investment knowledge may give them a greater ability to handle the risks inherent in a private placement. There are many ways to qualify as an accredited investor but they all have one thing in common, which is that the SEC believes they indicate an ability to take on risks that regulators believe are unsuitable for most retail investors.

Accredited investors are investors whose financial status or investment knowledge may give them a greater ability to handle the risks inherent in a private placement.

All of the following are considered accredited investors:

Banks, broker-dealers, investment advisers, insurance companies, and investment companies

Corporations, trusts, partnerships, and LLCs with more than $5 million in assets

Most employee benefit plans with more than $5 million in assets

The issuer’s directors, executive officers, and general partners

If the issuer is a privately owned fund, (such as a hedge fund), a knowledgeable employee of the fund, which means an employee with at least 12 months’ experience working on the fund’s investment activities

Individuals with income of $200,000 in each of the last two years, or $300,000 in combination with a spouse or spousal equivalent such as a domestic partner

Individuals with a net worth more than $1 million, alone or with a spouse or spousal equivalent, not including primary residence

Individuals who hold any of these three designations in good standing:

Licensed General Securities Representative (Series 7)

Any firm where all owners are accredited investors (e.g., venture capital firms)

Any other entity with more than $5 million in investments that was not formed specifically to qualify as an accredited investor; the purpose of this category is to include entities that don’t neatly fit into any of the above categories, such as:

Native American tribes

Labor unions

Government bodies, including those of foreign governments

Investment funds created by government bodies

New types of business entities that may be introduced by new laws

An accredited investor that is not an individual—such as a business, governmental, or nonprofit entity—is sometimes called an institutional accredited investor (IAI).

Qualified Institutional Buyers

QIBs are a narrower group of large institutional investors. A QIB is a large institutional investor that owns at least $100 million worth of securities, not counting securities issued by its affiliates. For registered broker-dealers, the threshold is lower, just $10 million. A bank must also have a net worth of at least $25 million in order to be considered a QIB.

If a firm has discretionary authority to invest securities owned by a QIB, those securities count toward whether the firm itself is considered a QIB. So if a broker-dealer has $9 million worth of securities in its own accounts, and holds $1 million worth of securities in a discretionary account belonging to a QIB, then the broker-dealer is itself a QIB.

Common examples of QIBs include broker-dealers, insurance companies, investment companies, pension plans, and banks. However, any corporation, partnership, or LLC could qualify as a QIB. So can an IAI that owns at least $100 million in securities. Individuals can never be QIBs, regardless of their assets or financial sophistication.

Individuals can never be QIBs, regardless of their assets or financial sophistication.

Rule 144A allows QIBs to buy unregistered securities at any time, and freely trade these shares to other QIBs. In effect, QIBs can trade unregistered shares among themselves with almost the same ease as trading registered shares. Selling unregistered securities to anyone other than a QIB commonly requires a the seller to hold the securities for a period of up to 12 months.

A QIB will virtually always meet the criteria to be an accredited investor, whereas an accredited investor may fall well short of QIB status.

Over time, other securities laws and regulations have made use of these two well-known categories. For example, in 2019 the SEC gave issuers more flexibility to test the waters with potential investors before deciding whether to go through with a public offering. When deciding which investors were sophisticated enough to receive test-the-waters communications, the SEC limited these communications to QIBs and institutional accredited investors. Additionally, references to institutional accredited investors have become more common, such as when the SEC revamped its rules around integration of offerings in March 2021.

Know your QIBs from your accredited investors and be ready to pass your securities exam with Solomon Exam Prep.

For more helpful securities exam-related content, study tips, and industry updates, join the Solomon email list. Just click the button below:

Suitability questions may appear daunting. But they don’t have to be – read the Solomon guide to answering suitability questions with ease. Continue reading

If you’re taking the FINRASeries 7 exam, you very possibly dread the term suitability. We understand that suitability questions may appear daunting. But to enhance your chances of passing the exam, you should have a good understanding of the concept and how it applies to certain test questions.

Suitability questions can be difficult because they often contain more than one answer choice that seems plausible. In short, they are more open-ended than other questions that appear on the exam. While this can make these questions tough, keep in mind that in each suitability question has one BEST answer given the information provided. This blog will help you select that that best answer choice.

First, what is a suitability question? The most basic type of suitability question presents a hypothetical investor and his profile and asks you which investment or investments is most suitable for him. Other suitability questions are about specific products. For instance, a question might ask you to choose the bond that would be most suitable for a high-income earner – usually a municipal bond. Finally, other types of suitability questions may provide an information about an investor and her profile and you will be asked which investments should be removed and/or added to her portfolio, or which proposed asset allocation is best.

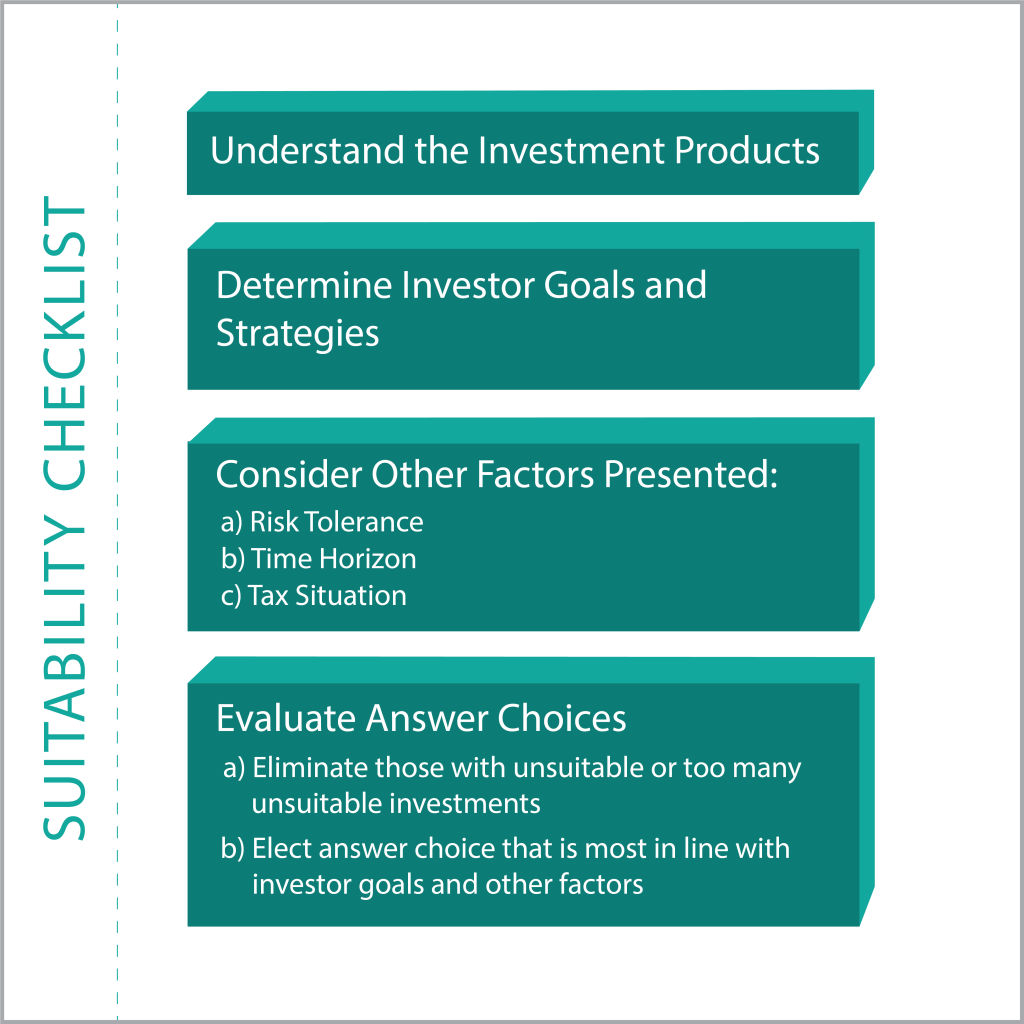

So, what’s the best strategy for answering these questions?

1. Learn and memorize the characteristics of the investment products.

The most basic requirement for properly approaching any of these questions is to have a good understanding of the investment products mentioned in the question. Think about it this way: if you don’t know the characteristics a product, it’s difficult to know who should and shouldn’t buy it. For instance, if you don’t know the characteristics of a growth fund or a municipal bond it will be hard to assess which investors should own these products or avoid them in favor of other products. This means learning and memorizing the characteristics of the major investment products, such as stocks, bonds, funds, and options, is the first step to mastering suitability.

2. Categorize the investment goals of the investor in the question.

Assuming that you understand the products mentioned in a question, let’s look at what else you should consider when answering a suitability question. First, when reading a suitability question, focus on the financial goals attributed to the hypothetical investor presented in the question.

There are four major investing goals and strategies that you should keep in mind when doing this. First, there are capital preservation investors. These investors are interested in obtaining a minimum level of return while not putting their principal at any significant risk. Then there are the income investors. These want to receive a steady stream of payments in hopes of supplementing their income. Third, there are capital growth investors. These are long-term investors whose primary hope is seeing the value of their investments rise over time. Finally, there are the speculative investors. These investors are willing to take on more risk in the hopes of earning higher gains in a shorter amount of time. Placing an investor in one of these categories, or a blend of two of these categories, will help you figure out which investments are most suitable for the investor.

3. Analyze the profile of the Investor, looking for risk tolerance, time horizon and tax bracket.

Risk Tolerance:

Look for the investor’s risk tolerance. If an investor is not willing to take on much risk, only the most conservative investments are suitable for him. In contrast, an investor with a high risk tolerance is willing to own more volatile types of investments. Typically, conservative risk tolerance correlates with capital preservation investors, and sometimes income investors, while high risk tolerance correlates with speculative investors and many capital growth investors. Examples of conservative investments include U.S. Treasury securities, money market funds, and bank CDs. Examples of high-risk investments include penny stocks, options, junk bonds, and possibly growth stocks.

Time Horizon:

An investor’s time horizon is another factor you must consider. Is the investor hoping for long-term growth, or is he going to need to cash out of his investments in a relatively short amount of time? Sometimes a question will not present you with this exact information but instead will give an investor’s age. Questions that mention an investor who is in his 20s or 30s are indicating someone with a long time horizon. In contrast, questions that describe an investor who only has a few years until retirement are usually describing someone with a shorter time horizon. Scenarios that describe a couple who wants to buy a house or pay for college in the next year, will also have a short time horizon, and therefore, will require liquid investments.

So which investments are best for long- and short-term investors? An investor with a long time horizon is able to invest in products that are expected to grow over time, such as growth stocks, equity mutual funds and ETFs, or annuities. He is also more likely to take on riskier investments since he has more time to make up for any losses. On the other hand, a short-term investor should invest in less volatile securities or debt investments that mature in the near term, such as U.S. Treasuries and money market funds. An investor with a short time horizon is also less likely to take on a high level of risk than a long-term investor because a short-term investor does not have as much time to make up any losses.

Tax Bracket:

A final factor to consider when determining suitability is income level or tax bracket. An investor who makes a lot of money will typically have a higher federal income tax rate. This means the money he receives from his investments will be more heavily taxed than the money someone in a lower tax bracket. Additionally, for a high income investor, capital gains are taxed at a lower rate than interest income. Oftentimes, it is best to recommend investments with fewer tax implications for a high-income investor. Municipal bonds, whose interest payments are usually tax-free at the federal level and often also tax-free at the state level, are typically suitable investments for high-income investors. In contrast, because the interest rates for municipal bonds are often lower than the interest rates for corporate bonds, investors in lower tax brackets may be better off purchasing corporate bonds than municipal bonds. Additionally, stocks are often suitable for investors with higher tax rates because their gains are not taxed until the stocks are actually sold. At the same time, investments that pay regular interest, but do not come with tax advantages may not be suitable for high-income investors because they will have to pay taxes on this interest.

So now that you know what to look for in suitability-type questions, let’s look at a couple of them:

QUESTION ONE:

Mary is an investor in her thirties. She makes $50,000 a year and is hoping to find an investment that will provide capital appreciation. At the same time, she would not mind supplementing her income by receiving regular payments from her investment. Which of the following would be most suitable for her?

A municipal bond fund

A growth and income fund

A small-cap stock fund

Penny stocks

This question tells you Mary’s investment goals and objectives. She’s looking for capital growth and secondarily income, so she’s a blend between a capital growth and income investor. Additionally, since she’s in her thirties, you can assume that she has a relatively long time horizon. Finally, her low income means she is not in a high tax bracket.

You know that Mary needs an investment option that provides the potential for both capital growth and income payments. Both penny stocks and small-cap stocks carry the potential for capital growth; however, neither of them typically offers income payments. That is because neither penny stocks nor small-cap stocks pay meaningful dividends. This eliminates choices C and D. A municipal bond fund would provide income because municipal bonds make semi-annual interest payments. However, outside of high-yield bonds, bonds in general don’t offer much in the way of capital growth. Also, since interest from municipal bonds is generally not taxed at the federal level, municipal bond interest payments are lower than corporate debt securities and thus are not the best debt investment option for an investor who is not in a high tax bracket. Given all of this information, you can eliminate choice A as well. Now let’s look at choice B. A growth and income fund contains stocks with `capital growth potential along with stocks that provide regular dividend payments. Also, growth stocks are also good for investors like Mary who have long time horizons. Looks like you’ve found the correct answer: Choice B makes the most sense.

QUESTION TWO:

Alisha is 26 and has just received an MBA. She’s starting on a career as a sales manager at a large company and has a bright future. She has $15,000 to invest with your firm, and she tells you that she would like to see that principal appreciate as much as possible over the next two to three decades. She also says she has no problem taking on a high level of risk to help make that happen. Which of the following asset allocations would be most suitable for Alisha?

20% income fund, 20% municipal bond fund, 20% fixed annuities, 20% dividend-paying stocks, 10% non-traditional ETFs, 10% cash

20% bond mutual fund, 20% agency bonds, 10% money market funds, 15% bank CDs, 15% dividend-paying stocks, 10%, 10% cash

30% large-cap stocks, 20% equity index mutual fund, 20% U.S. Treasuries, 20% AAA-rated corporate bond funds, 10% FDIC-insured bank CDs

20% small-cap stocks, 20% medium-cap stocks, 20% growth fund, 15% high-yield bond funds, 15% balanced fund, 10% interval fund

Again, you’re presented with the investor’s investment goals and objectives in the question prompt. In stating that Alisha hopes to see her principal appreciate as much as possible over a long period of time, the question is telling you that she is a capital growth investor. It also is implying that she has a long time horizon. Additionally, it states that she is willing to take on a high level of risk in meeting her investing goals, which means she’s an investor with a high risk tolerance.

Given each of these factors, you need to look for the portfolio that makes the most sense for her. That portfolio should contain more equity investments than debt investments. That is because in general equities provide better capital growth potential than bonds. Additionally, you should look for investments that have higher growth potential and which carry more than a moderate level of risk. Remember that higher risk often equals higher potential reward, and Alisha is willing to take this gamble.

So let’s look at each of the possible answer choices.

Alisha isn’t really interested in earning income as part of her strategy and wants the potential for large gains. That means choice A, which is heavy on income and low-return investments, should be discarded. The same is true of choice B. Choice C is a bit tougher to eliminate. That’s because this hypothetical portfolio does include some growth-type investments, such as large-cap stocks and equity index mutual funds. However, these are both equity investments that are known to provide a more moderate return potential than Alisha is seeking. Additionally, choice C contains a relatively high percentage of fixed and low-return investments, and thus it doesn’t look like a great answer choice. That leaves choice D. The hypothetical portfolio presented in that answer choice is heavy on aggressive growth-type stocks and funds that carry a high level of risk, such as small-cap stocks, mid-cap socks, and growth funds. Additionally, a high-yield bond fund is a type of debt security that comes with capital growth potential. And it includes 10% allocation to an interval fund, a type of fund that invests in non-publicly traded securities that are illiquid and may be less correlated to the other publicly trade securities in this portfolio. Thus, choice D is the best choice and the correct answer.

Suitability questions are definitely not easy. But if you consider all of the relevant aspects presented in the answer choices and have a solid understanding of different types of investments, they are something you can master. And master them you must if you want to pass the Series 7 or the Series 6 exam.

For more helpful securities exam-related content, study tips, and industry updates, join the Solomon email list. Just click the button below:

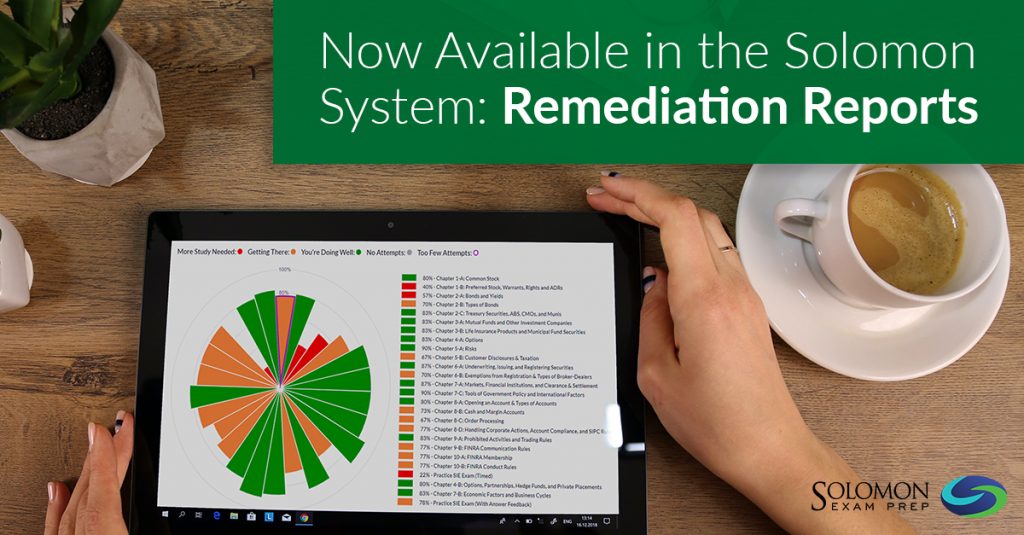

Learn about the Solomon Remediation Report, a new analytical feature designed to help students pass their securities licensing exams the first time. Continue reading

Solomon Exam Prep is delighted to announce an advanced analytical feature called a Remediation Report. The Solomon system analyzes a student’s five most recent practice exams and determines whether a student is ready to take his or her exam. If Solomon AI determines that a student is not ready to sit for their exam, then it creates an individual report with personalized guidance on how to remediate and prepare to pass. This custom Remediation Report is sent to the Solomon student’s email inbox.

The Solomon Remediation Report is connected to the Solomon Pass Probability tool, the industry-leading measure of a security exam prep student’s readiness to pass an exam. Solomon Pass Probability is based on thousands of student data points. Once a Solomon student has taken at least five practice exams, the Solomon Pass Probability feature is activated, and the Pass Probability metric is available in the student’s dashboard. The Solomon Remediation Report provides an additional level of customized study support by helping students focus their efforts and remediate before they sit for their exam.

Watch the latest Solomon Exam Prep video for a complete look at the Solomon learning system and what it offers students and firms. Continue reading

Solomon Exam Prep has helped thousands of financial professionals pass their FINRA, NASAA, MSRB, and NFA licensing exams. Watch the video for a complete look at the Solomon learning system and what it offers students and firms.

To explore Solomon Exam Prep study materials for 21 different securities licensing exams, including the SIE and the Series 3, 6, 7, 14, 22, 24, 26, 27, 28, 50, 51, 52, 53, 54, 63, 65, 66, 79, 82, and 99, visit the Solomon website.

For many when choosing bonds the most important factor is the tax implications. Knowing the after-tax yield and tax-equivalent yield calculations is critical. Continue reading

Bonds can be nice, reliable investments. Pay some money to an issuing company or municipality, receive interest payments twice a year, and then get all of your original investment back sometime down the road. Sounds like a plan.

But which bonds are best for a specific investor? There are many factors for bond investors to consider when choosing which bond to buy, but for many the most important is the tax implications of investing in one bond instead of another. This concern is most prominent when an investor compares a corporate bond to a municipal bond. For reference, a corporate bond is one issued by a corporation or business, while a municipal bond is one issued by a state, city, or municipal agency.

Comparing the tax implications of these bonds is important because the interest payments that investors receive from municipal bonds are typically not taxed at the federal level. Conversely, interest payments on all corporate bonds are subject to federal taxation. This means that someone in the 32% tax bracket will have to give Uncle Sam 32% of his interest received from a corporate bond, while he will not give up any of his interest received from a municipal bond. Additionally, an investor does not pay state taxes on municipal bond interest if the bond is issued in the state in which the investor lives. Corporate bond interest, on the other hand, is always subject to state tax.

interest payments taxed federally

interest payments subject to state tax

interest payments not federally taxed

interest payments not taxed by state if issued in state local to investor

For these reasons, when comparing a corporate bond to a municipal bond, understanding the after-tax yield and the tax-equivalent or corporate-equivalent yield is essential. This is true both for investors and for those who will be taking many of the FINRA, NASAA, and MSRB exams. So let’s look at how to calculate those yields.

After-Tax Yield

First the after-tax yield. The after-tax yield tells you the amount of a corporate bond’s annual interest payment that an investor will take home after accounting for taxes he will be assessed on that interest. Once that amount is known, the investor can compare it to the yield he would receive from a specific municipal bond and see which potential investment would put more money in his pocket. When calculating the after-tax yield, start with the annual interest percentage (a.k.a. coupon percentage) of the corporate bond, which represents the percent of the bond’s par value that an investor receives each year in interest. For instance, a corporate bond that has a $1,000 par value and an interest rate of 8% will pay an investor $80 dollars in annual interest ($1,000 x 0.08 = $80). You then multiply the coupon percentage by 1 minus the taxes an investor will pay on the corporate bond that he will not pay on the municipal bond that he is considering.

This is where it sometimes gets tricky. What taxes will an investor not pay when investing in a municipal bond that he will pay when investing in a corporate bond? Remember that for just about all municipal bonds, investors do not pay federal tax on interest received.

The formula for after tax yield is:

After-tax yield = Corporate Bond Annual Interest Rate x ( 1 – Taxes Investor Does Not Pay By Investing in Municipal Bond)

On the other hand, an investor always pays federal taxes on interest received from a corporate bond. Additionally, an investor does not pay state taxes on interest payments from a municipal bond issued in the state in which the investor lives.

On the other hand, an investor always pays state taxes on interest received from corporate bonds. So if you see an exam question in which you need to calculate the after-tax yield of a corporate bond to compare it the yield on a municipal bond, you will always subtract the investor’s federal income tax rate from 1 in the equation. You will also subtract the investor’s state tax rate from 1 if the municipal bond is issued in the investor’s state of residence.

Seems simple, right? Here’s a question to provide context:

Marilyn is a resident of Kentucky. She is considering a bond issued by XYZ Corporation. The bond comes with a 7% annual interest rate. Marilyn is also interested in purchasing municipal bonds issued in Ohio. If Marilyn has a federal tax rate of 28% and Kentucky’s state tax rate is 4%, what is the after-tax yield on XYZ’s bond?

To answer this question, begin with the interest rate on the XYZ bond, which is 7%. Then subtract from 1 the taxes Marilyn will not pay if she invests in the municipal bond in question. She will not pay federal taxes on the municipal bond interest, so you would subtract 28%, or .28. However, because Marilyn is a resident of Kentucky and the municipal bonds she is considering are issued in Ohio, she will pay state taxes on the bond. That means you would not subtract her state tax rate (0.04) from 1. After subtracting .28 from 1 to get 0.72, you multiply that amount by the 7% coupon payment. Doing so gives you a value of 5.04 (7 x 0.72 = 5.04%). This means that the interest amount she would take home from the XYZ bond would be equivalent to what she would receive from a municipal bond issued in Ohio that has a 5.04% interest payment. If she can get a bond issued in Ohio that has a higher interest payment than 5.04%, she would take home more money in annual interest payments than she would from the XYZ bond.

Tax-Equivalent Yield

The second approach an investor can take to compare how a potential bond investment will be affected by taxation is to calculate the tax-equivalent yield (TEY). This calculation is also known as the corporate-equivalent yield (CEY). The TEY/CEY measures the yield that a corporate bond will have to pay to be equivalent to a given municipal bond after accounting for taxes due. To calculate this yield, you take the annual interest of the given municipal bond and divide it by 1 minus the taxes the investor will not pay if she invests in the municipal bond that she would pay if she invested in a corporate bond.

Here’s the formula for tax-equivalent yield:

Tax-equivalent yield = Municipal Bond Annual Interest Rate / (1 – Taxes Investor Does Not Pay By Investing in Municipal Bond)

When determining what tax rates to subtract from 1 in the denominator, the same principal as described above applies. That is, the investor will not have to pay federal tax on the municipal bond, so her federal rate is always subtracted from 1. The investor will also not have to pay state tax on the bond if it is issued in the state in which she lives. If that is the case, the investor’s state tax rate should also be subtracted from 1. However, if the investor lives in a different state than the state in which the bond is issued, she will have to pay state taxes on the interest payments. In that case, her state tax rate would not be subtracted from 1.

Here’s another question to provide context.

Franz, a resident of Michigan, has purchased a Michigan municipal bond that pays 4% annual interest. If his federal tax bracket is 30% and the Michigan state tax rate is 4%, what interest rate would he need to receive on a corporate bond to have a comparable rate after accounting for taxes owed?

To answer this question, begin with the interest rate on the Michigan municipal bond, which is 4%. Then subtract from 1 the taxes that Franz will not pay on that bond that he would pay if he invested in a corporate bond. He wouldn’t pay federal taxes on the municipal bond interest, so you would subtract 0.30 from 1. Additionally, since the bond is issued in Michigan and he is a Michigan resident, Franz will not pay state taxes on the bond. So you subtract Michigan’s state tax rate of 4%, or 0.04, from 1 as well. After subtracting 0.30 and 0.04 from 1 to get 0.66, you divide that number into the 4% municipal bond annual interest. Doing so gives a value of 6.06 (4 / 0.66 = 6.06). This means Franz would need to find a corporate bond that pays 6.06% in annual interest to match the amount of interest he will take home annually from the Michigan municipal bond after accounting for taxes.

Many people are confused by the concepts of the after-tax and tax-equivalent yields. But you don’t have to be one of them. Just follow this simple approach and any questions you see on this topic will not be overly taxing.

Question: A Municipal Finance Professional (MFP) hosted a $500 plate fundraiser for a governmental issuer. Does this event trigger a ban on business for two years?

A. Yes, it will trigger a ban because an MFP may not host a fundraiser.

B. Yes, it will trigger a ban because the cost per plate is above the de minimis amount.

C. No, it will not trigger a ban because the MFP did not contribute money, only time and space.

D. No, it will not trigger a ban because the MFP was holding the fundraiser, not the municipal dealer.

Correct Answer: A

Explanation: MFPs are not permitted to solicit funds for municipal issuers or their officials without triggering a two-year ban on business for their firm. Thus, holding fundraisers is not allowed. Municipal dealers are also forbidden from holding fundraisers.

To explore free samples of Solomon Exam Prep’s industry-leading online exam simulators for the SIE, Series 7, Series 14, Series 50, Series 52, Series 54, and other FINRA, MSRB, NASAA, and NFA exams, visit the Solomon website here.

Do your customers know the difference between an IA and BD? Do you know the importance of this distinction and how it may affect your registration status? Continue reading

Do your customers know the difference between an investment adviser and broker-dealer? Do you know the importance of this distinction and how it may affect your registration status?

For many retail customers, the difference between an investment adviser (IA) and a broker-dealer (BD) may not seem important. A customer may have received an investment recommendation from a BD, or owned securities through an IA account. However, which kind of firm you work for is important for knowing which services you may provide, how you may provide them, and which qualification exams you must pass.

Investment Advisers

Investment advisers are usually firms, though they can be an individual operating as a sole proprietor, whose primary business is providing investment advice, and who are paid for the advice itself. Investment adviser representatives (IARs) are individuals who work for IAs and advise the IA’s clients on the IA’s behalf. IAs and IARs are not “stockbrokers” and cannot directly buy or sell securities for their customers. While many have IA accounts through which they own stocks, mutual funds, and other securities, in fact these are accounts an IA opens on the customer’s behalf with a BD.

Broker-Dealers

Broker-dealers are usually firms, though they can be an individual operating as a sole proprietor, that execute securities transactions for customers. An individual who is employed by a BD to handle customer accounts is called an “agent of a broker-dealer” on some exams, or a “registered representative” (RR) on others. BDs can offer investment advice incidental to their work with customers but cannot be compensated for the advice itself. If a BD acts as an intermediary between a buyer and a seller, then the BD can charge a commission on the trade. If a BDs buys or sells from its own inventory, then the BD makes money by charging a markup on securities that they sell and taking a markdown on securities that they buy.

So, if you’re an IAR, you…

…can provide advice

…can be paid for that advice

…cannot execute trades

…cannot charge commissions or markups on your customer’s trades

If you’re a BD agent (also known as a registered representative), you…

…can provide advice

…cannot be paid for that advice

…can execute trades

…can charge commissions or markups on your customer’s trades

Testing and Licensing

Finally, many firms, especially larger ones, maintain both IA and BD registrations. When working for these “dual registrants,” you may be asked to qualify as an IAR, BD agent, or both, depending on your role.

In fact, an increase in dual registrations is one of the note-worthy trends Solomon discusses in our recent white paper, “Optimizing On-Boarding in 2021: 7 Key Trends for the Securities Industry,” available for download from this blog post.

To become an agent of a broker-dealer (registered representative), you must pass the Securities Industry Essentials (SIE), and a “top-off” exam such as the Series 6 or Series 7, and for state registration usually the Series 63. To become an IAR, you must pass either the Series 65, or, if you work for a dually registered firm, the SIE, the Series 7, and the Series 66.

This month’s study question from the Solomon Online Exam Simulator question database is now available. Continue reading

This month’s study question from the Solomon Online Exam Simulator question database is now available.

***Comment below or submit your answer to info@solomonexamprep.com to be entered to win a $20 Starbucks gift card.***

This question is relevant to the SIE, Series 6, 7, 22, 24, and 82 exams.

Question:

Which of the following people would be considered a specified adult?

Answer Choices:

A. A 16 year old with autism

B. A 30 year old

C. A 60 year old with a heart condition

D. An 18 year old in a coma

Correct Answer: D

Explanation: A specified adult is a natural person age 65 and older or a natural person age 18 and older who the member firm reasonably believes has a mental or physical impairment that renders the individual unable to protect his or her own interests.